From the Federal Reserve Bank of New York's Liberty Street Economics blog, August 7:

Recent natural disasters have renewed concerns about insurance

markets for natural disaster relief. In January 2025, wildfires wreaked

havoc in residential areas outside of Los Angeles. Direct damage

estimates for the Los Angeles wildfires range from $76 billion to

$131 billion, with only up to $45 billion of insured losses (Li and Yu, 2025).

In this post, we examine the state of another disaster insurance

market: the flood insurance market. We review features of flood

insurance mandates, flood insurance take-up, and connect this to work in a related Staff Report

that explores how mortgage lenders manage their exposure to flood risk.

Mortgages are a transmission channel for monetary policy and also an

important financial product for both banks and nonbank lenders that

actively participate in the mortgage market.

Flood Damages and Insurance Coverage

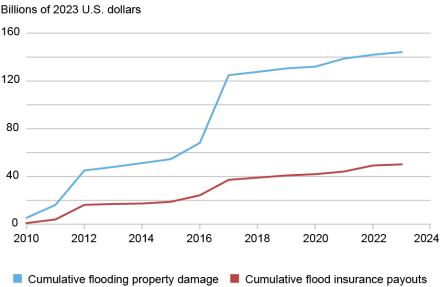

The U.S. has sustained substantial and largely uninsured damages from

flooding over the past fifteen years. The chart below displays the

cumulative damages from flooding in the U.S. and the cumulative

insurance payouts on these damages, starting in 2010. Between 2010 and

2023, the direct property damage from flooding totaled nearly

$144 billion (in 2023 USD). In the same period, insurance payments on

property damage from the National Flood Insurance Program totaled

approximately $50 billion (in 2023 USD)—just 35 percent of the direct

damages. These damage estimates understate the full economic cost of

flooding by excluding indirect damages (for example, lost income and

production associated with floods).

Cumulative Flood Damages and Insurance Payments, 2010‑23

Sources: Authors’ calculations, NOAA Storm Events Database, FEMA. Notes:

Both damages and insurance payments considered are restricted to those

in the fifty states and District of Columbia, excluding damages and

claims in U.S. territories.

Insurance Mandates

What does the flood insurance market look like and who has to

purchase flood insurance? Flood insurance in the U.S. is almost

exclusively provided through the National Flood Insurance Program

(NFIP), which is managed by the Federal Emergency Management Agency

(FEMA). In its role administering the NFIP, FEMA designates special

areas with elevated flood risk, known as 100-year flood zones. A

100-year flood zone is a FEMA-designated area with an annual probability

of experiencing a major flood of at least 1 percent (that is, at least

one major flood is expected every 100 years). With little exception,

flood insurance is required to obtain a mortgage for a property in

100-year flood zones—areas that cover roughly 5 percent of residential

properties.

Although these flood-prone areas are mostly concentrated in coastal and

riverine areas, smaller pockets exist across the country. The chart

below shows the county-level proportion of properties covered by a

100-year flood zone for the contiguous states. Nearly 20 percent of all

properties located in one of FEMA’s 100-year flood zones are located

within one mile of the coast, but the majority are located further

inland—approximately 60 percent of properties inside a 100-year flood

zone are located more than ten miles from the coast....

Brian Harmon

had just finished spending over $300,000 to fix his home in

Kingwood, Texas, when Hurricane Harvey sent floodwaters “completely over

the roof.”

The six-bedroom house, which has an indoor swimming

pool, sits along the San Jacinto River. It has flooded 22 times since

1979, making it one of the most flood-damaged properties in the country.

Between

1979 and 2015, government records show the federal flood insurance

program paid out more than $1.8 million to rebuild the house—a property

that Mr. Harmon figured was worth $600,000 to $800,000 before Harvey hit

late last month.

“It’s my investment,” the 49-year-old said this summer, before the hurricane. “I can’t just throw it away.”....