Regarding Signature bank and SVB, just how toxic are their loan books?

Two from Wolf Street. First up, the headliner April 10:

Retail CRE debt has been crappy since 2017, and banks managed without collapsing. Now Office goes to heck. Multifamily, the biggie, is following.

First, the US Banking landscape.

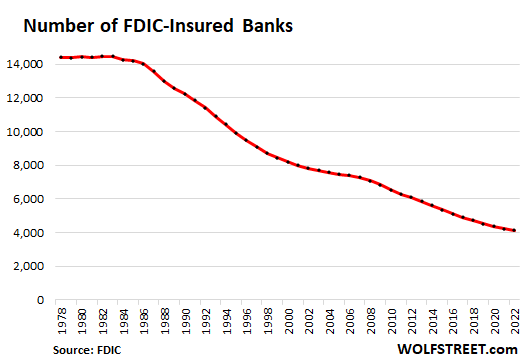

There are 9,697 domestically-chartered banks, savings associations, and federally insured credit unions in the US. Of them, 4,135 were FDIC-insured commercial banks as of December 2022, with 71,190 branches, according to the FDIC’s year-end tally. Now minus three banks, in order of collapse date: Silvergate Bank, Silicon Valley Bank, and Signature bank. So, today maybe 4,132 banks.

All these banks, savings associations, and credit unions had $29 trillion in assets. Of them, the FDIC-insured banks alone had $23 trillion in assets. Of them, four held 40% of those assets:

- JP Morgan ($3.2 trillion in assets)

- BofA ($2.4 trillion in assets)

- Citibank ($1.8 trillion in assets)

- Wells Fargo ($1.7 trillion in assets).

Then there’s nothing for a long distance before we get to the fifth largest bank, US Bank, a regional bank, with $585 billion in assets. Silicon Valley Bank was the 16th largest bank at the end of 2022 with $209 billion in assets.

The 32nd largest bank had less than $100 billion in assets. The 132nd largest bank had about $10 billion in assets. The 2,050th-largest bank – the bank in the middle, or the median bank – had just $315 million in assets.

That’s important to understand when we talk about bank failures: If a few of these smaller banks collapse, few people outside of their community would even notice, though it could be a big blow to their community, especially in rural areas where this may be the only bank within miles.

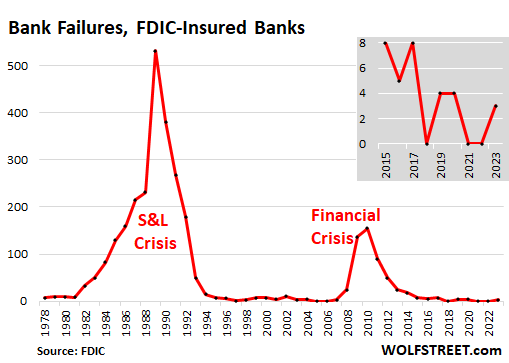

Bank failures are kind of routine, but can spike.

As long as banks have existed, banks have failed, just like other companies have failed, even the most splendid ones. In the US, banks can’t file for bankruptcy (though their holding companies can). Failed banks are taken over by regulators and are “resolved.” This is a much quicker process than dismembering it in bankruptcy court, and it allows for most of the deposits to be returned to the economy in short order.

So far in 2023, among the FDIC-insured banks, there have been three bank failures, if you include Silvergate, which was forced to shut down. There were no bank failures in 2021 and 2022, but four in 2020 and four in 2019.

The gray insert shows the bank failures from 2015 through 2023 so far. The massive spike in the 1980s was the Savings & Loan crisis, which led to the prosecution and quality time in the hoosegow for a bunch of bank executives. Yes, those were the good old times. By contrast, during the Financial Crisis, no one even attempted to send anyone to the hoosegow.

CRE Debt by category.

Multifamily (apartment buildings, student housing, etc.) is by far the largest category. CRE debt outstanding by CRE category as percent of total CRE debt:

- Multifamily: 44.2%

- Office: 16.7%

- Retail: 9.4%

- Industrial (warehouses, etc.): 8.0%

- Lodging: 6.7%

- Healthcare (life sciences): 2.1%

- Other: 12.9%

Some CRE debt still in good shape, others are in trouble.

....MUCH MORE

And April 11:

Trouble in Multifamily CRE: Two Big Messes, and Investors Are on the Hook, not Banks

A REIT specializing in CRE loans foreclosed on 3,200 apartments in Houston. CMBS investors hit by default of 62 multifamily buildings in San Francisco.