From ZeroHedge:

On Tuesday, we pointed out something which we hoped was only unintentionally ironic: at the same time as the first day of Jay Powell's highly anticipated Congressional Testimony (which, to loosely paraphrase Gabriel Garcia Marquez was titled "inflation love in a time of Treasury cholera") was set to begin, JPMorgan was holding a conference call "on potential asset bubbles" - all of which have been sparked by the abovementioned individual - which included the who is who of sellside JPM research, including the bank's heads of global equity and credit research, the top quants, and so on.

During the call, which had thousands of JPM clients dialing in and which was riddled with technical difficulties, JPMorgan traders and researchers discussed their outlook for global markets in the context of what virtually everyone now sees is one massive bubble...

... including the implications of growing retail participation in US equity markets, the increased acceptance and adoption of bitcoin and possible market consequences.

For those who missed it, here are the bank's own highlights of its top ten takeaways (a replay can be found here) while the accompanying presentation is at the bottom:

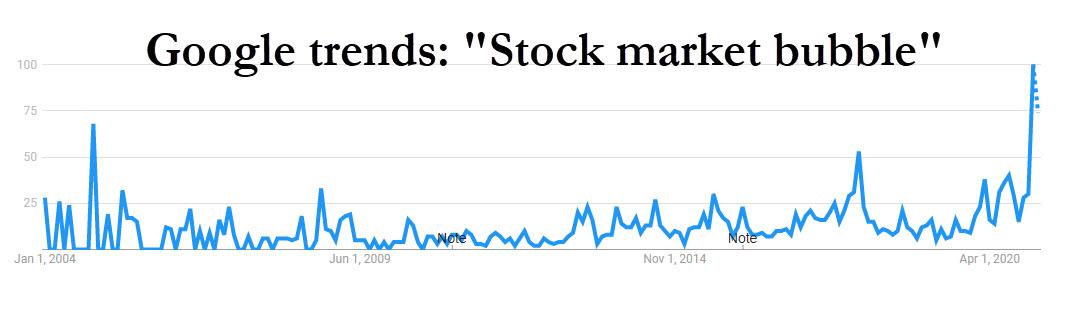

1. We do not see a broad equity market bubble but rather certain pockets of the market that are experiencing hyper growth such as electric vehicles and renewables. While there is a lot of talk about bubbles, it is hard to see one in the broad equity market, where a dominant group (FANGs) practically hasn’t moved for 6 months despite massive amount of stimulus and an expected economic recovery, Financials that have barely recovered 2020 losses, and Energy that is still down 25% from last year despite a commodity bull market. We do see some relatively contained market segments that appear to be in a bubble related to Electric Vehicles (EV), renewable energy and innovations stocks. These sectors only make up a small part of the market (e.g., electric vehicles make up only 2% of the S&P 500), but we do see segments that remain cheap such as energy where positioning remains heavily underweight. We believe that this is only the first inning of the market rally, and that the rotation into cyclicals could play out for the next year. The broad rotation into cyclicals has contributed to an increase in intraday volatility as realized volatility of the S&P 500 has gone down to 5. If we want to be thorough in our search for bubbles, there is another asset that is currently in a bubble—the VIX. The VIX is now disconnected to underlying short-term S&P 500 realized volatility, indicating a bubble of fear and demand from investors looking to hedge or profit from a hypothetical market selloff. Given the VIX is at a near-record premium to actual equity volatility (~400-500% above the ‘fair value’), we think selling the “VIX bubble” represents a good market opportunity.

2. We remain constructive and sanguine on the outlook for the S&P 500, and the strong rotation and outperformance to Value from Growth which should continue and taking into account client positioning. Although the topic of reflation has been top of mind for most clients in the past few weeks, we have seen investors starting to position for higher interest rates by reducing exposure from high multiple and momentum names. However we remain positive and constructive on the market outlook. We distinguish between a positive vs. negative rise in yields and remain constructive as the Covid-19 recovery is on track, ongoing fiscal and monetary support will be forthcoming with a new stimulus bill and a possible infrastructure bill in the pipeline, and equity positioning remains low. There is strong interest for reopening names such as cruise lines, transports, casinos and hotels from both hedge funds and real money accounts and also growing interest in financials and energy.

3. There has been a strong rebound in global gross exposures across equities, up ~11% month to date, or 9% year to date. Short gamma positions have increased, but we see that as a secular phenomenon as retail activity has increased. Despite some warning of a ‘VAR shock’ what we are seeing now is ‘VAR inflows’ with volatility targeters/risk parity funds adding (rather than reducing) ~$1.5bn in equity exposure daily and gamma hedging reducing S&P 500 volatility, and long VIX positioning (e.g. via ETPs, limiting VIX upside)....

....MUCH MORE