From FT Alphaville:

Cu in hell

But not just yet.

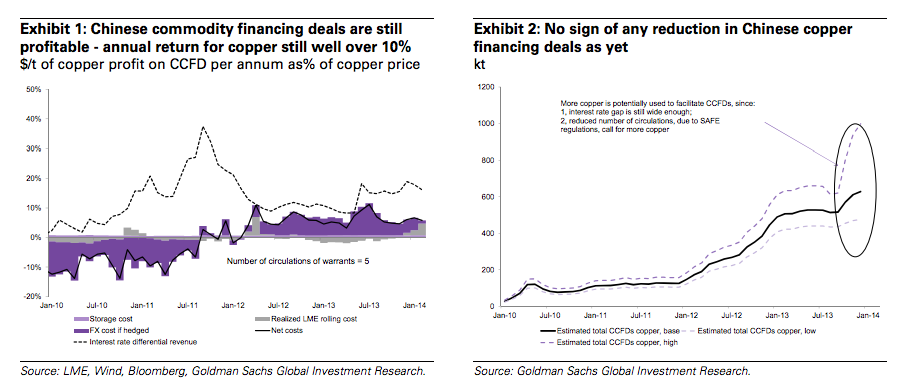

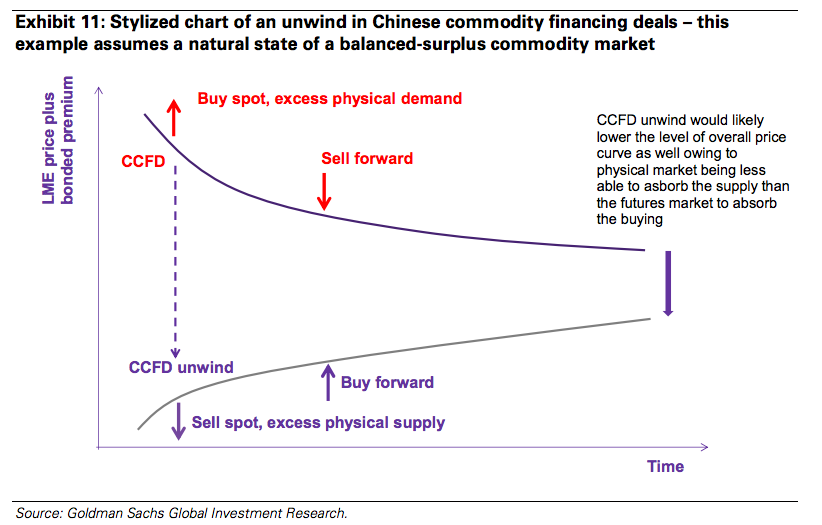

The chart is from Goldman Sachs’ latest metals note. The basic point is that recent moves in copper, rather than signalling any immediate unwind, are being caused by slower Chinese demand and strong global copper supply growth while copper financing ticks along… for now, obviously:

In contrast to some media reports, we find that the bulk of Chinese commodity financing deals are ongoing, facilitating ‘hot money’ inflows into China and providing a mechanism to import low cost foreign financing. In general, the profitability of most currency and commodity hedged Chinese commodity financing deals remains substantial, owing to a still positive CNY and USD based interest rate differential (>4%), limited depreciation in the CNY over the past month (<2 a="" and="" are="" cny="" commodity="" copper="" cost="" currency="" curve="" exposure="" forward="" hedging="" i.e.="" in="" lack="" limited="" of="" returns="" still="" the="" tightness="" underlying="">10% (Exhibit 1), and up to 1mt of physical copper could still be tied up in deals (Exhibit 2).

That’s in contrast to iron ore btw, but since it didn’t have a liquid futures market going for it and we’ve already covered that, we’ll just skip along… From Goldman again...MORE