Right now, land and development, urban econ. from Building the Skyline.org's Skynomics blog, Dec. 17:

Clark and Kingston

In 1930, W. C. Clark and J. L. Kingston (CK), an economist and architect, respectively, published a book called, The Skyscraper: A Study in the Economic Height of a Modern Office Buildings. In this work, they act as a hypothetical developer of a Manhattan office skyscraper. Their aim was to determine a height for the structure which maximized the return, given the rents, and the costs of land and construction.

In fined-grained detail, they laid out the various elements of erecting such a building, including floor plans, and the all the different types of costs a builder must pay, from bricks, to elevators, to steel. For their analysis, they chose a large lot across the street from Grand Central Station, in the heart of Manhattan’s midtown business district.

The point of this exercise was to demonstrate that the supertall towers rising in Manhattan during the late 1920s were not “freak” buildings, but rather, were based on reasonable economic foundations.[1] They showed that when one did all of the accounting—comparing the income to the costs—the height that maximized the return was 63 stories. (Ironically, this is not that much different than today. One Vanderbilt, an office building currently under construction across the street from Clark and Kingston’s hypothetical lot, will rise 58 stories.)

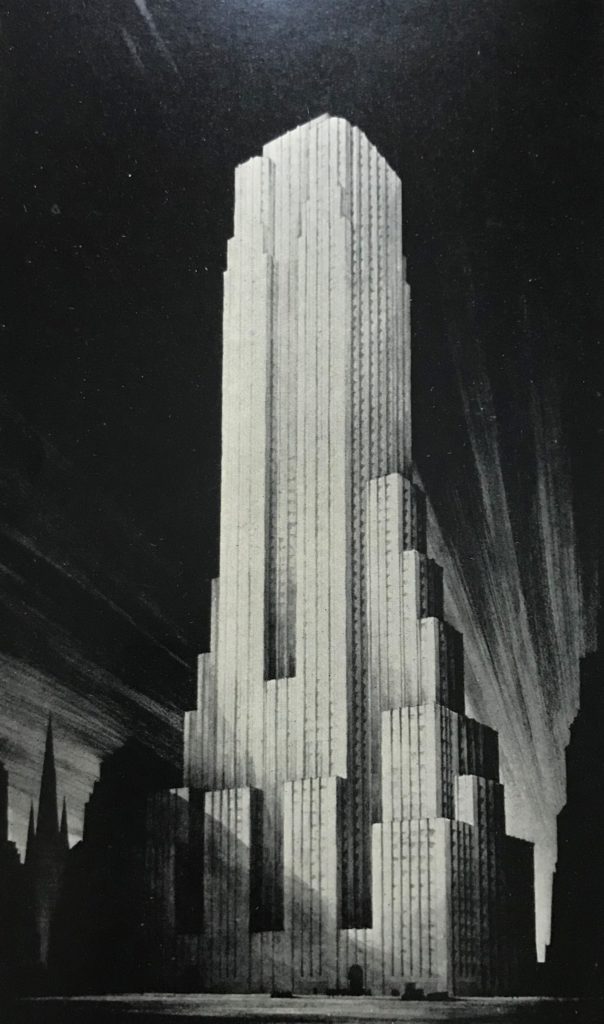

Manhattan Skyscraper Rendering by Architect J. L. Kingston. At 63 stories it was considered the ideal height at the time. Source:

The Skyscraper: A Study in the Economic Height of a Modern Office Buildings (1930).

The Skyscraper: A Study in the Economic Height of a Modern Office Buildings (1930).

Economic Height In their book, they present a definition of what they called the Economic Height of the building, based on the writings of the engineer, J. Rowland Bibbins; and one that is still reasonable:...MUCH MORE

The true economic height of a structure is that height which will secure the maximum ultimate return on total investment (including land) within the reasonable useful life of the structure under appropriate conditions of architectural design, efficiency of layout, light and air, ‘neighborly conduct’, street approaches and utility services. (pps. 8-9)Economic Height provides a useful guide (though not the only one) for understanding why skyscrapers get built, since this height is determined by the best balance between the revenues and costs. In general, going taller will generate more income, but will also add to the expense. In modern economics terminology, the economic, or profit maximizing, height is one where at the highest floor, the additional or marginal revenue from that floor just equals the marginal or additional cost to providing it. If built one floor higher, the cost of adding the floor will be greater than the revenue and will not be worth it. If less than that height, money is “left on the table,” since adding a floor would produce more income than it would cost to produce it.

It’s worth stressing is that a developer builds this optimal height to earn a profit. People and companies are willing to pay the high prices because of the needs they fulfill and the benefits they provide. Thus, Economic Height is a response to the demand; not the other way around.

Land Values and Building Height

As CK also demonstrate, there is a direct relationship between the cost of acquiring the land and the return on investment from a taller building. We can think of developers as a type of urban farmer; the more it costs to acquire a lot, the more they must intensely develop the land in order to receive enough income to compensate for the high cost of the location. Thus, around the world, we observe taller buildings in places that have higher land values.

Given this notion of Economic Height as a benchmark, we can then say that any building that is taller than this can be considered economically “too tall” in that it is higher than it “ought to be” for pure economic gain; and hence produces lower profits than a shorter building. The difference between the actual and Economic Height is what I call Symbolic Height....

January 3:

The Economics of Skyscraper Height (Part II)