The easy part is seeing how the dominoes start to fall, it will be because of a clogged toilet somewhere,* but getting the contra bet down will take some creativity.

From MacroBusiness:

Will US investors pull the pin on housing?

Following on from this morning’s post on how Wall St has re-inflated US housing, here is Westpac’s Elliot Clarke on the role of investors in US housing. I see two possible ways this can go. If Wall St is driving the rebound through rental securitisations then it could run despite rising interest rates because it’s a play on reaping the financial packaging fees. But the asset remains in the hands of the bank et al there has to be a high risk of run on the market when rates turn (or taper arrives). A tipping point scenario if I’ve ever seen one.

The US housing sector has been a key focal point in this recovery, not only due to the material price and activity declines that occurred following the GFC, but also because of the sector’s historical ability to have a positive, broad-based impact on activity – directly through new construction, and indirectly through confidence and consumption.

When considering the health of the housing market, house prices have been the financial market’s primary benchmark, the expectation being that as go prices, so goes activity. However, this has not proven to be entirely correct, with the contribution to growth of housing activity lacklustre relative to the scale of the prior decline and past cycles.

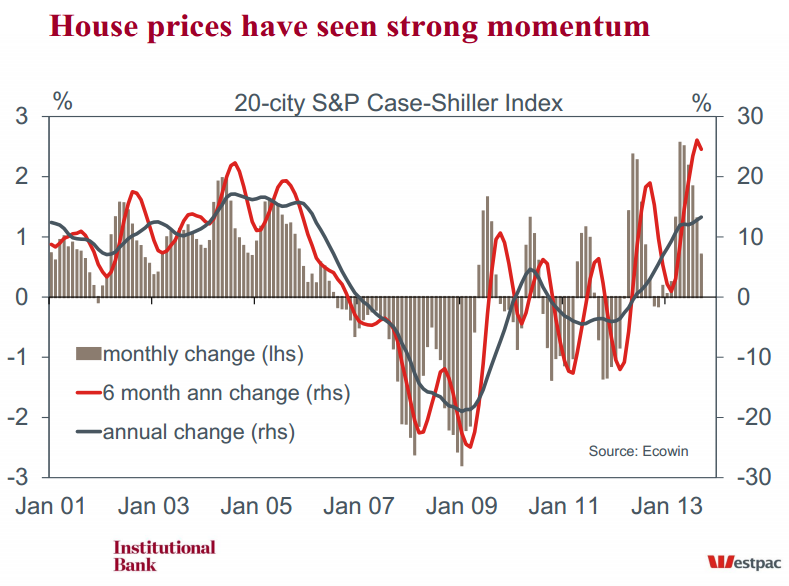

On house prices, the past two years have definitely given reason for optimism and confidence. According to the S&P/ Case-Shiller 20-city measure, house prices have risen by 18.5% between January 2012 and September 2013, with the bulk of those gains seen in the past year (13.3%yr).

While these gains are certainly significant, it is important to remember that, owing to the scale of the GFC price declines, national house prices are still down 21.5% from their April 2006 peak in nominal terms; and, given the PCE deflator has risen by almost 14% over that time, closer to a third in real terms. Arguably this is a key reason as to why the pass-through from price gains to confidence and consumption has been more modest than that seen in past cycles.....MOREFrom AlterNet (!) over a year ago:

...Think about what this means. Just as banks got out of the business of administering the mortgages they made, these securitized rental investors would replace conventional landlords. To make these deals profitable, lots and lots of mortgages would have to be combined. But, the investors won’t administer these rentals. Instead, a rental servicer would be responsible for collecting your rent and distributing it to all of the investors.In the meantime there's a beautiful opportunity for rental servicers.

Now, what will happen when your toilet backs up or there is no heat? Your concerns would be addressed at a call center, perhaps in another country, provided you stay on hold long enough and are eventually switched to the right person.

Most likely, after leaving any number of messages, your rental servicer will schedule an appointment when you have to be at work. Or, will just allow you to get on with it, and sort the problem on your own.

Suppose you decide to hold back rent until the repairs are taken care of. The servicer may report you as delinquent in paying your rent. That may make it harder for you to find a new rental later—or finance the car you need to get to work—because this negative information would be reported to credit agencies....