I'm not seeing that QE is doing a damn thing other than lifting equity prices.And from last spring: "Is the US Economy Getting More Energy Efficient or Not?":

The fact that the Fed persists in the face of that reality pretty much tells you that raising asset valuations is the goal with all the other chatter being misdirection.

Cool, keep it up.

On the other hand declining oil prices aren't the worst thing in the world. We used to figure a 10% move in oil equated to a lagged 1% move, up or down, in CPI. In our more energy efficient world it's probably a 20:1 ratio but it still matters.

Short answer: yes.Here's FT Alphaville:

It takes fewer and fewer BTU's of energy to produce a dollar of GDP. That statement is a bit simplistic however in that it doesn't account for the fact that a service economy is almost by definition less energy intensive than an industrial model, that being a San Francisco residential real estate agent consumes fewer BTU's than an aluminum smelter for the same GDP activity....

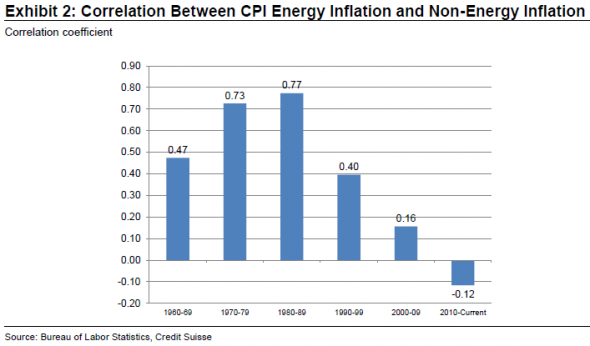

The declining correlation between energy and non-energy inflation

The chart above is from a note by Credit Suisse economists, who write:

Second-round effects of oil and gasoline prices have diminished in recent decades. In fact, the correlation between energy and non-energy items has turned negative recently. Two explanations for this shift tend to get the most emphasis. First, the economy is much less energy intensive than it used to be. Second, inflation expectations are lower and better anchored than, say, the 1970s “wage-price” spiral era.These are sensible longer-term explanations. The note doesn’t get into causality, but the possibility that higher energy prices have been mildly deflationary for other items throughout the current, interminably-crap recovery also seems reasonable....MUCH MORE