First up, Kimble Charting Solutions:

The Japanese Yen (left chart above) created a multi-year flag pennant pattern, reflected by a series of higher lows and lower highs. Once traders broke the bottom of the pennant, sellers rushed in, creating one of the largest currency declines we have witnessed in years.Over the past few years the Australian Dollar has been forming a similar pennant pattern (right chart above) and of late traders look to have broken support of the pennant pattern at (1).Is another key global currency about to bite the dust, due to the breaking of support of the large pennant pattern? Will sellers step in and drive the AU$ lower like they did the Yen?

And from MacroBusiness:

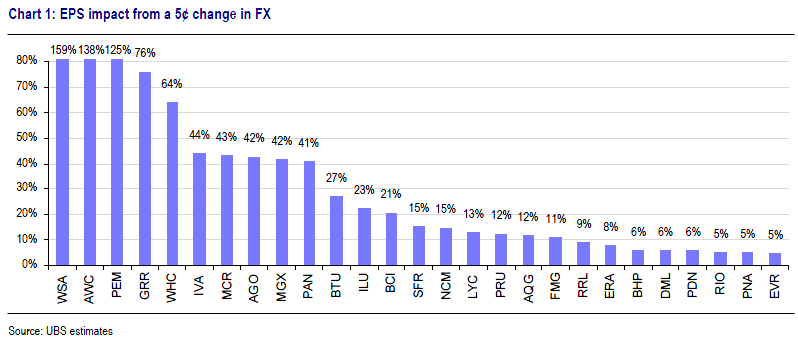

Anyone would think that Australia was an economy of houses and holes. It’s a constant snap back narrative of buy banks, buy miners, as if that’s the only option. It isn’t and a couple of new investment notes today show why. The first is from UBS looking at the positive benefits to miner’s EPS if the dollar keeps falling. The chart assumes a 5% fall:

The greatest change in earnings is displayed by WSA, AWC and PEM, with a 100% change in EPS for a US5¢ change in the A$. Albeit these companies have little to no earnings, which amplifies the sensitivity. Interestingly, BHP is slightly more sensitive to the A$ than Rio Tinto.

Weaker A$ could drive EPS upgrades and improved equity performanceThat’s spot on. But even diversified names are risky. Almost half of BHP’s revenue comes iron ore and the margins are huge so the impact on profit is even greater....MORE

A weaker A$ would drive upgrades to consensus earnings for the miners, as consensus A$ for CY 13/14 is US$1.04/US$1.00. Therefore we should expect that Resource equities to outperform in an EPS upgrade environment. However, we also need to consider the reason for A$ weakness; that being the possible winding back of QE and weaker commodity prices. Both may weigh on equity performance. We retain our preference for the high quality diversified names.