With the effect mentioned in February's "Prepare for a Springtime CPI Collapse" having come to pass and about to begin receding in the rear view mirror it is probably time to begin paying attention to things like May 2's "FAO Food Price Index Rises Again In April, Now At Two Year High" and the the headline essay from Wolf Street, May 5:

Driven largely by non-housing services. Just in time for the Fed meeting.

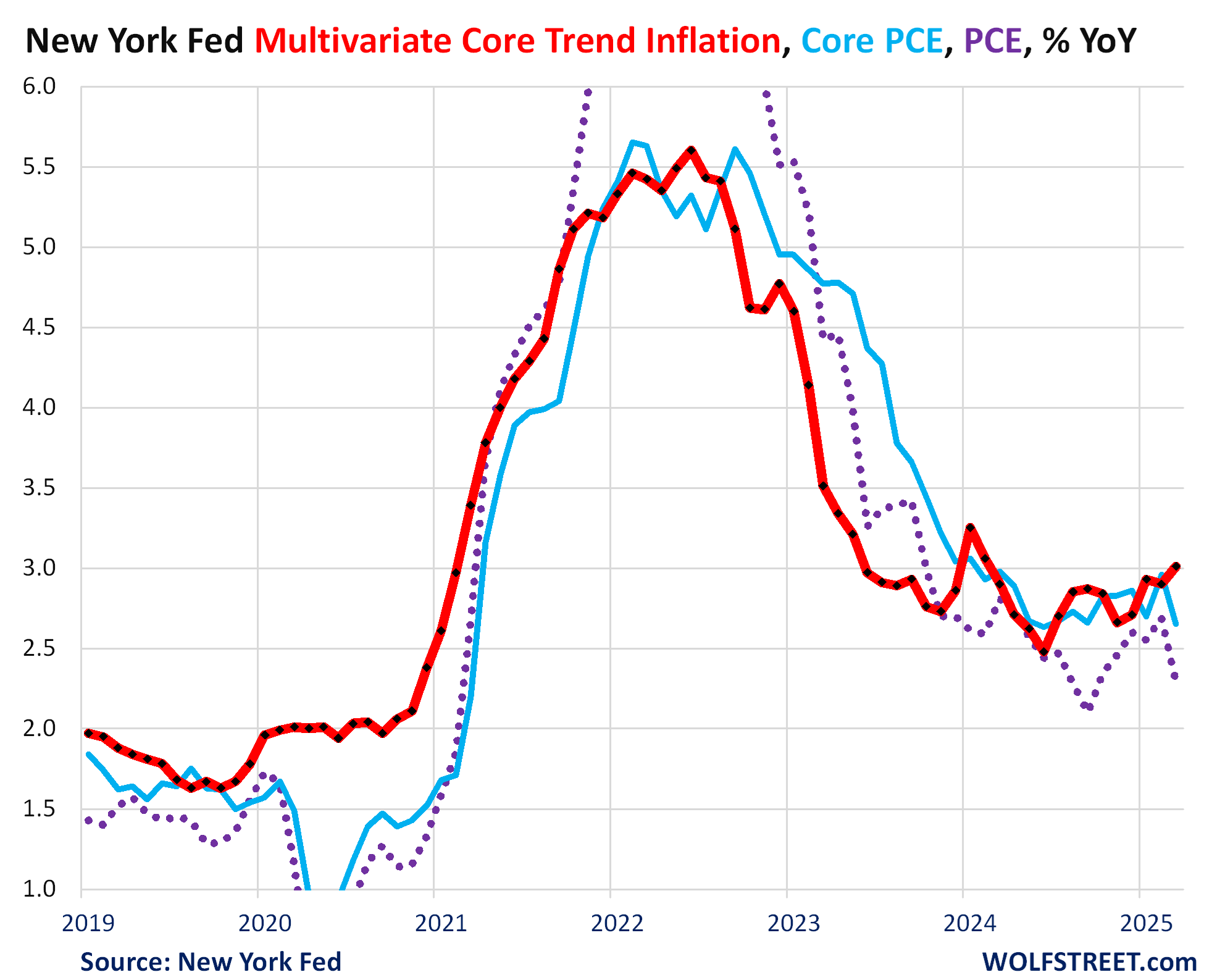

Back in April 2022, when the Fed’s favored inflation measure, the PCE price index, was surging towards its June 2022 high of 7.2% year-over-year, and core PCE to a high of 5.6%, the New York Fed came out with an inflation measure to track inflation’s “persistence.”

This “Multivariate Core Trend” (MCT) inflation measure is based on the same components of the PCE price index, but aggregates them differently. This MCT inflation rate, on a year-over-year basis, decelerated sooner than the core PCE and overall PCE inflation measures in 2022 and 2023, in effect successfully predicting their deceleration months in advance. And now it is predicting the resurgence of PCE inflation.

The MCT inflation rate for March accelerated to 3.0% year-over-year, the worst reading since February 2024 (red in the chart), according to the New York Fed today. The re-acceleration was driven largely by non-housing services and to a small extent by “core goods” components, even as the Fed-favored core PCE inflation (blue line) and overall PCE inflation (purple dots) decelerated year-over-year (my discussion of PCE inflation for March).

So now MCT, which attempts to show “persistence” of inflation, is predicting a substantial re-acceleration of inflation – the “persistence” part – driven largely by non-housing services and to a small extent by core goods. So housing cost inflation, as measured by rents, is no longer the driver of this inflation; it’s non-housing services and to a small extent, core goods.

Should we take this MCT seriously, after it was designed to run ahead of the surge of inflation in late 2020 and early 2021, and then successfully predicted the deceleration of core PCE and PCE inflation in 2022 and 2023?

In this inflation whack-a-mole, where inflation pressures shift to different products and services all the time, anything that can shed light on inflation’s next move – such as the concept of “persistence” in inflation – helps.

These kinds of data points are precisely why the Fed pivoted to wait-and-see....

....MUCH MORE