From Wolf Street, May 20:

The BOJ’s QT, inflation that’s higher than in the US, an atrocious fiscal mess, a devalued yen, it all comes together.

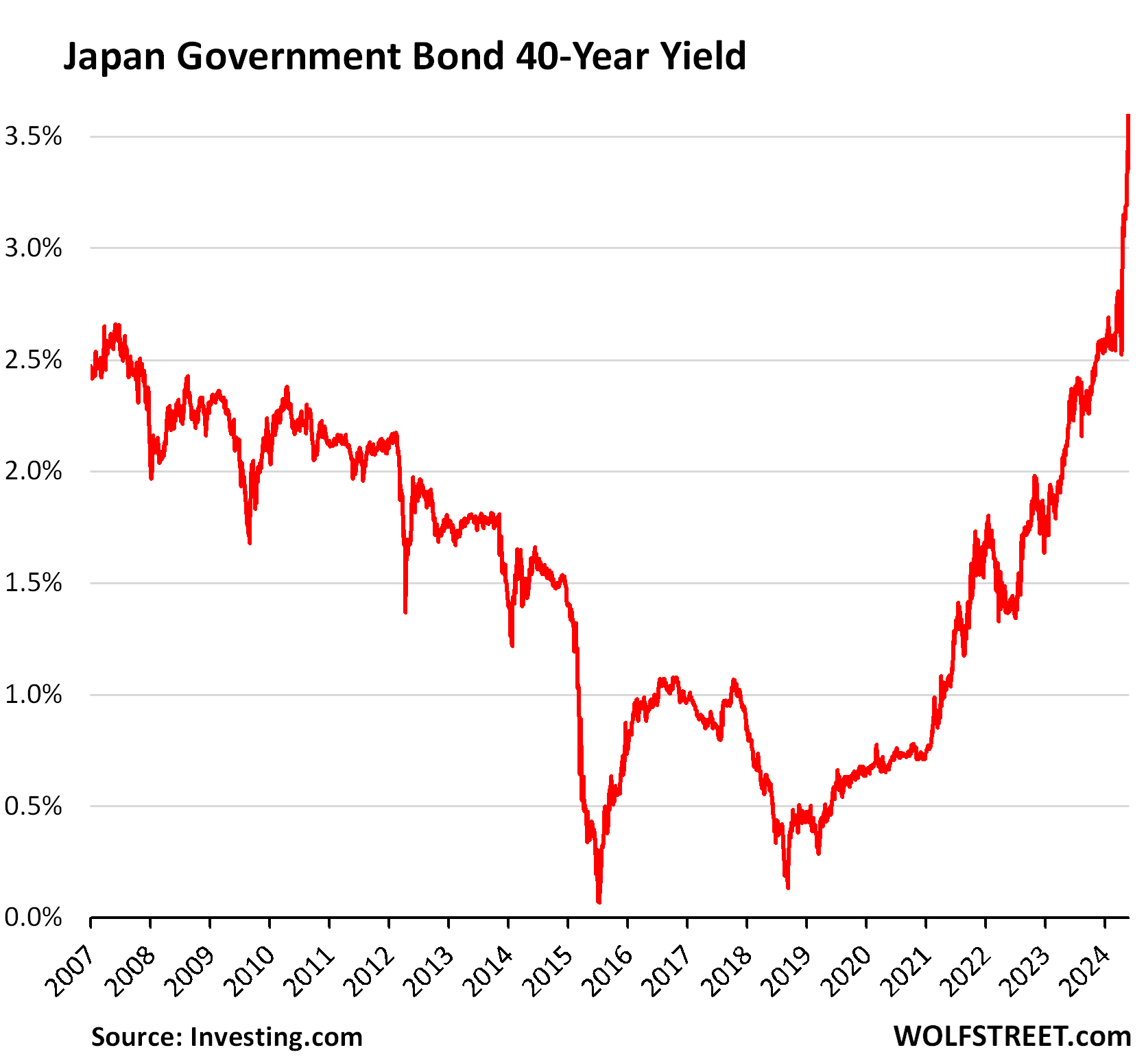

Japan, which now has substantially more inflation than the US – 3.6% overall CPI and 3.2% core CPI – is watching in astonishment as its very-long-term bond yields spike in a dramatic manner, while the Bank of Japan has accelerated QT this year, which it started in mid-2024.

The superhero is the 40-year JGB yield, which jumped another 11 basis points at the moment, for a spike of 100 basis points since the beginning of April, to 3.56% at the moment. A rising yield means a falling price.

Despite the breathtaking spike, the 40-year yield is still a hair below the rate of Japan’s overall inflation rate, and thereby a hair negative in real terms, and new bond buyers are still getting ripped off in terms of yield.

And bond holders that bought new 40-year bonds a few years ago when the 40-year yield was below 1% or even below 0.5% are getting crushed on price, because a yield spike like this in a very-long-term bond means that the market price of the bond collapses. If they don’t want to take the loss selling it, they can hold the bond to maturity, collecting a miserable 0.5% or whatever in coupon interest a year, for decades, and then finally get paid face value when the bond matures, and the purchasing power of that face value will be much diminished by decades of inflation. Inflation without compensation....

....MUCH MORE