First up, the call fourteen months ago at NZZ's The Market.ch, October 14, 2022:

Market strategist and historian Russell Napier warns of a 15- to 20-year phase of structurally elevated inflation and financial repression. He shares his views on how investors should prepare for this new world.

Russell Napier has never been one of the eternal inflation warners. On the contrary: The market strategist and historian, who experienced the Asian Financial Crisis 25 years ago at first hand at the brokerage house CLSA in Hong Kong, wrote for years about the deflationary power of the globalised world economy.

Two years ago, the tide turned and Napier warned of a vicious return of inflation – and he hit the mark. In an in-depth conversation with The Market NZZ, which was lightly edited for clarity, he explains why most developed economies are undergoing a fundamental shift and why the system most investors have become accustomed to over the past 40 years is no longer valid.

According to Napier, financial repression will be the leitmotif for the next 15 to 20 years. But this environment will also bring opportunities for investors. «We will see a boom in capital investment and a reindustrialisation of Western economies,» says Napier. Many people will like it at first, before years of badly misallocated capital will lead to stagflation.

In summer of 2020, you predicted that inflation was coming back and that we were looking at a prolonged period of financial repression. We currently experience 8+% inflation in Europe and the US.

What’s your assessment today?

My forecast is unchanged: This is structural in nature, not cyclical. We are experiencing a fundamental shift in the inner workings of most Western economies. In the past four decades, we have become used to the idea that our economies are guided by free markets. But we are in the process of moving to a system where a large part of the allocation of resources is not left to markets anymore. Mind you, I’m not talking about a command economy or about Marxism, but about an economy where the government plays a significant role in the allocation of capital. The French would call this system «dirigiste». This is nothing new, as it was the system that prevailed from 1939 to 1979. We have just forgotten how it works, because most economists are trained in free market economics, not in history.

Why is this shift happening?

The main reason is that our debt levels have simply grown too high. Total private and public sector debt in the US is at 290% of GDP. It’s at a whopping 371% in France and above 250% in many other Western economies, including Japan. The Great Recession of 2008 has already made clear to us that this level of debt was way too high.

How so?

Back in 2008, the world economy came to the brink of a deflationary debt liquidation, where the entire system was at risk crashing down. We’ve known that for years. We can’t stand normal, necessary recessions anymore without fearing a collapse of the system. So the level of debt – private and public – to GDP has to come down, and the easiest way to do that is by increasing the growth rate of nominal GDP. That was the way it was done in the decades after World War II.

What has triggered this process now?

My structural argument is that the power to control the creation of money has moved from central banks to governments. By issuing state guarantees on bank credit during the Covid crisis, governments have effectively taken over the levers to control the creation of money. Of course, the pushback to my prediction was that this was only a temporary emergency measure to combat the effects of the pandemic. But now we have another emergency, with the war in Ukraine and the energy crisis that comes with it.

You mean there is always going to be another emergency?

Exactly, which means governments won’t retreat from these policies. Just to give you some statistics on bank loans to corporates within the European Union since February 2020: Out of all the new loans in Germany, 40% are guaranteed by the government. In France, it’s 70% of all new loans, and in Italy it’s over 100%, because they migrate old maturing credit to new, government-guaranteed schemes. Just recently, Germany has come up with a huge new guarantee scheme to cover the effects of the energy crisis. This is the new normal. For the government, credit guarantees are like the magic money tree: the closest thing to free money. They don’t have to issue more government debt, they don’t need to raise taxes, they just issue credit guarantees to the commercial banks....

....MUCH MORE

And Wolf Richter at Wolf Street, December 2, 2023

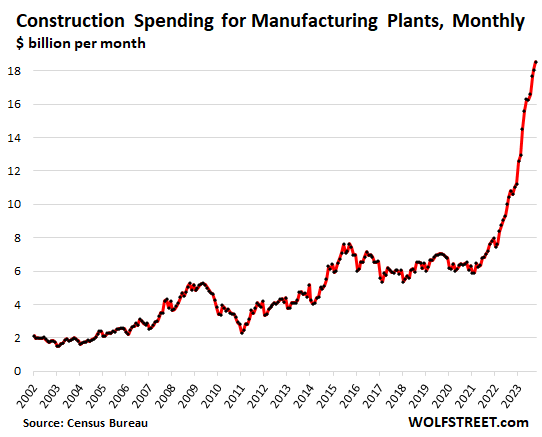

The Eyepopping Factory Construction Boom in the USThe supply-chain catastrophe in 2020-2021, the edgy US-China relationship, and the scary dependence on China triggered a big corporate rethink.

In October, $18.5 billion were plowed into construction of manufacturing plants in the US ($246 billion annualized), up by 73% from a year ago, by 136% from two years ago, and by 166% from October 2019. The relentless pace of the month-to-month increases is what’s amazing – from $12.5 billion spent in January to $18.5 billion in October.

The construction boom started in early to mid-2021, and since then, spending has tripled. About a year later, in July 2022, Congress passed a package of subsidies for select manufacturing industries to build factories, such as semiconductor makers (they’ll get $52 billion) and EV battery makers.

But the wheels of government turn slowly, approvals take their time, disbursements of funds for large projects takes time, so the flow of these government funds would just be the first trickle in 2023. The bulk is still coming.

....MUCH MORE