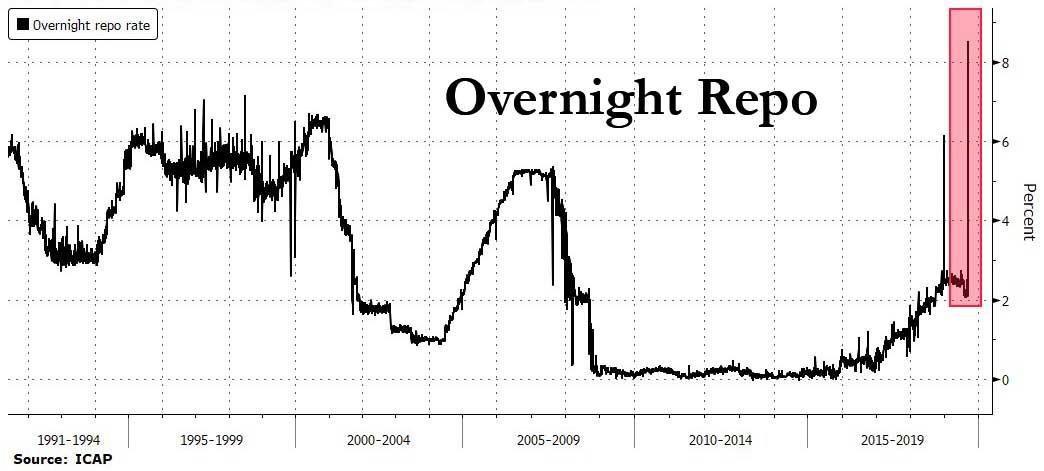

When it comes to the shady events in the shadow banking world of collateral assets and repurchase agreements, nobody does it better than interdealer broker, ICAP, which is not only intimately familiar with just how the Fed's plumbing vision takes place in the real world, but also happens to be the go to firm for pricing on such suddenly critical market stress indicators as repurchase rates.

And sure enough, it was none other than ICAP which first - correctly - said this morning when overnight G/C repo hit 10%...

{kind=link}

... that the Fed would announce its first repo hike in a decade, but also did so with alarming accuracy and detail, as the following note sent out by Icap's Mike Derrico at 6:45am laid out:

Tax Date Funding Squeeze: Overnight System RPs?

This week’s funding squeeze has raised a number of questions about the outlook for the Fed’s balance sheet. We’re going to punt most of the longer-term questions because we want to focus this morning on one very short-term option that the Fed might consider: for the first time in many years, we think it is at least conceivable that the Fed’s Open Market Desk this morning might arrange an overnight system RP with primary dealers of the sort that was commonplace before the expansion of the Fed’s balance sheet in 2009.

The Desk has stood by and watched any number of episodes of temporary repo market pressure in recent years without responding by injecting cash. (The most notable case was the spike in the Treasury GCF average to more than 5.00% on December 31.) While the Desk has some leeway to respond to major market -functioning disruptions (blackouts, etc.), the FOMC has never instructed it to intervene solely for the purpose of limiting repo-rate volatility. The Desk’s directive is framed solely in terms of the FOMC’s effective federal funds rate target.

This week’s episode is different. We think there is a significant risk that the fed funds rate for Tuesday will set above the 2.25% target upper boundary of the Fed’s target rate. Our very tentative guess is that the effective funds rate for Monday, due out at around 9:00 this morning, will remain within the range, but only because the effective rate is calculated as a median. A significant volume of activity, including much that trades directly rather than in the broker market, may have been booked before the extent of the repo market carnage was apparent. The mean weighted average for fed funds on Monday probably moved above the target range, but the median may have been below it.

That probably won’t be true to today. With overnight repo trading at rates above 3% in the reg market yesterday afternoon, lenders in the fed funds market are likely to be pickier this morning. Even if repo market pressure in general eases a bit from yesterday, the effective funds rate could move up from yesterday’s level. We think the odds favor a reading above 2.25% for September 17, regardless of whether the September 16 fixing that will be published around 9:00 AM today is in the target range or not.

That poses a challenge for the Fed. On the one hand, traditional funds rate-targeting guidelines would not only allow a traditional overnight RP with the primary dealers this morning; they would appear to call for one. On the other hand, the first large-scale system RP in a decade would raise a huge number of questions in the market, which might be difficult to disentangle from the broader policy message. We will confidently predict that many traders in many markets would gloss over the nuances of the difference between EFFR and GCF volatility, and jump directly to the conclusion that Fed balance sheet policy had reached another major inflection point. Even though we think that an overnight or short-term system RP with the primary dealers would qualify as “business as usual” in some important ways, we also know that the first system RP in a decade would reverberate through the markets.

We have been lobbying for months for the Fed to pre-announce its intention to arrange traditional RPs with the dealers on key pressure points (mid-month, month-end) as a way of limiting the scope for overnight volatility and to gather information about how Fed repo injections would affect broader market conditions. Despite that, we’ll confess that we are a little daunted by the communications challenges of making a technical change of this nature purely reactively, and on the first day of an FOMC meeting to boot. We think a strong argument could be made for arranging a system repo this morning, but we’re not sure it’s a convincing argument.

Operational Details. If the Fed does arrange an overnight or term RP this morning, we would expect the operation to follow the format of the Desk’s most recent small-value “operational readiness” exercise. As matter of “prudent planning”, the Desk conducts small-scale test operations with the primary dealers on a regular basis. The most recent tests were in May, when the Desk arranged $75 million of 2-day terms RPs on May 8 and $75 million of overnight RPs on May 13.

Both operations were multi-tranche RPs in which the Fed accepted Treasury, agency and MBS collateral, with potentially different stop-out rates for each of the three asset classes. (The MBS stop-out was just 1 basis point above the Treasury stop-out in those operations, but the Desk might impose a wider spread if it were to conduct an operation today.) We would not expect the Fed to pre-announce a size for any operation conducted this morning, as there would be a benefit in reviewing dealer propositions before determining the amount of funding to provide.

The Desk has generally employed a multi-price discriminatory format than a Dutch-auction format for its open market repo operations. We have no reason to expect that to change.

Earlier at ZH:The Desk would presumably want to give dealers some time to think through their bidding strategy if it were to announce an RP this morning. The two May operations both closed at 10:00 AM. If the Fed has not announced an operation by 9:00 AM, the odds of a repo injection this morning would drop off quickly. (If the Fed’s goal is to prevent the median fed funds rate from rising above the target range, it needs to make its intentions clear as early in the session as possible to prevent early trades from going through at elevated levels.)So what happens next? Well, now that the Fed has successfully put out the fire in the monetary basement, if only for the day until the repo rolls tomorrow, the question is what the Fed will do or say tomorrow to ease the market's fear that a funding crunch is deteriorating (immediately catalysts for today's move being temporary notwithstanding). Here, according to ICAP, there are at least three other longer-term options that the FOMC could consider in its implementation note tomorrow afternoon. ...MUCH MORE

$53.2 Billion In QE Lite: Fed Concludes First Repo In A Decade Amid Liquidity Panic

"Nobody Knows What's Going On": Repo Market Freezes As Overnight Rate Hits All Time High Of 10%

Something Just Snapped: Chaos Hits Repo Market As "Dollar Funding Storm" Makes Thunderous Landfall