Mr. Lee is only the second analyst we've seen mention lock-up periods. In the case of SpaceX the current shareholders will have to sell stock just to get the free-float high enough to meet S&P's criteria for inclusion into the 500 sometime next year.

Additionally Lee's crossing the valley of the shadow of death to the broad sunlit uplands (boy, there's a pair of mixed allusions/metaphors) is interesting for its eventual bullishness.

From The Motley Fool, June 5:

Tom Lee of Fundstrat is undeniably one of Wall Street's most bullish market strategists.

In fact, it's unusual for Lee not to be bullish. To his credit, Lee

has nailed most of his bull market calls over the past several years.

Interestingly, however, Lee recently appeared on CNBC to discuss what he

called an upcoming three-phased market. Lee expects a bumpy ride in the

near term, including a correction or bear market that could begin shortly. Let's take a look.

The market is about to run into a host of challenges At recent prices, the benchmark S&P 500 (^GSPC 1.53%) index has risen nearly 11% this year. That's impressive, considering all the challenges it's had to overcome, including doubts about artificial intelligence (AI) at the beginning of the year and then the Iran war, which has led to higher oil and gas prices that are likely contributing to elevated inflation.

However, Lee said the market has been bolstered by incredibly strong

first-quarter earnings. According to Lee, most market forecasters had

penciled in $70 of collective earnings per share (EPS)

for the S&P 500. First-quarter EPS actually came in at about $80, a

big beat on expectations for what had already been expected to be a

strong quarter of growth.

If the market stays on this trajectory, that's $40 in additional EPS on an annualized basis, which could lift the S&P 500

by 800 to 1,000 points, according to Lee. However, Lee's base case,

based on what he and the team at Fundstrat had expected to be a

"challenging year," is a three-phased market.

The first phase, currently underway, is largely bullish. With the

S&P 500 now slightly above 7,560 (as of June 3), Lee thinks the

rally could last a little bit longer, potentially taking the market to

around 7,700.

The second phase, which will shortly follow, will be a challenging period for the market.

"Then we are going to digest a lot of things until October," Lee told

CNBC. "And that's a new Fed chair; it's the energy shock ... especially

shortages of petroleum products and lubricants. ... And the third is

the IPOs of SpaceX, OpenAI, and Anthropic that when the unlocks happen,

that's a lot of extra supply.

By "unlocks," Lee refers to the expiration of lock-up provisions that

allow insiders and employees with company shares to sell those shares

in the public market.

"I think that could pressure stocks in a way that feels like a bear market," Lee added.

However, Lee sees this more difficult period settling after the

midterm elections, at which point he expects stocks to rally strongly,

with 2027 yielding "some of the best we've ever seen in our lifetime."....

Mystery customers. Missing permits. Inaccurate customs declarations. Investigations in the U.S. and Mexico. Documents shed light on an alleged fuel smuggling racket.

Ikon Midstream, a Houston-based petroleum trader whose offices were raided last month by U.S. authorities,

is under investigation in Mexico in connection with fuel smuggling,

according to three Mexican security sources with direct knowledge of the

matter and four Mexican government security documents viewed by

Reuters.

The

probe is part of ongoing investigations into maritime shipments of

petroleum products that were brought to Mexico from the U.S. and Canada

in an alleged scheme to evade a hefty tax due on these imports, the

documents and sources said.

Ikon

Midstream is among the “central pieces” in a suspected scheme linked to

one of Mexico’s most powerful crime groups, the Jalisco New Generation

Cartel (CJNG), and Mexico’s attorney general’s office has opened an

investigation into the company “based on testimonies, documents and

surveillance,” according to one of the documents.

Mexico’s attorney general’s office did not respond to requests for comment.

The

Texas trader’s export of diesel aboard the tanker Torm Agnes is being

scrutinized for potential cartel links, as is Ikon Midstream’s purported

relationship with a suspected CJNG-related trucking company that helped

offload the vessel’s cargo in the ports of Ensenada and Guaymas,

according to the security sources and the document.

Smuggled

fuel and stolen crude oil have become the second-largest source of

revenue for Mexico’s cartels behind narcotics, according to the U.S.

government.

Two

of the documents laid out the operations and players in the alleged

racket. Among them, Ikon Midstream was allegedly a supplier of petroleum

products that moved through a complex web of importers, transporters,

distributors and facilitators in Mexico. The other two documents

contained summaries of the probes. The four documents were created in

March and April and their authenticity was confirmed by the security

sources.

Asked

to comment about the investigations, Ikon Midstream Executive Director

Rhett Kenagy said in a May 12 email to Reuters that there was “not a

single shred of documentation to back any of it up” and that the company

was “not going to respond to accusations grounded in hearsay.”

Homeland

Security Investigations, the primary transnational investigative agency

within the U.S. Department of Homeland Security, executed a criminal

search warrant at Ikon Midstream’s Houston offices on April 14, a DHS

spokesperson told Reuters in an April 17 statement. “This is related to

an ongoing investigation into criminal activity,” the statement said.

DHS did not elaborate, and it did not comment on whether it was

coordinating with Mexican authorities.

Excerpt

from an April 17, 2026, statement to Reuters from the U.S. Department

of Homeland Security

about a raid made earlier that week by its

investigative unit at the Houston offices of Ikon Midstream.

Ikon

Midstream has repeatedly denied wrongdoing. In an April 24 statement to

Reuters, the fuel trader said it “has never knowingly provided, and

does not knowingly provide, material support or resources to CJNG.”

Regarding the raid by Homeland Security Investigations, Ikon Midstream

said in its statement that “an investigative action by law enforcement

is not itself a finding of wrongdoing.”

Mexican

authorities have announced the arrests of at least 16 people since

September in connection with fuel smuggling. While officials have said

they’ve uncovered a “criminal structure” behind the alleged illicit

activity, they haven’t publicly named the detainees or said anything

about their possible connections to CJNG.

In an October report,

Reuters chronicled how diesel exported by Ikon Midstream aboard the

tanker Torm Agnes made its way into the hands of Intanza, a Mexican

company that authorities there suspect is a front for CJNG. Intanza has

no listed phone number, website, social media presence or physical

location that Reuters could find.

That

story detailed how Mexican cartels earn billions of dollars annually by

smuggling fuel, mainly from the U.S. to Mexico, in what boils down to a

massive tax dodge: Diesel, gasoline and naphtha are claimed in trade

paperwork to be lubricants to avoid a steep import duty that Mexico

charges on these imported fuels.

Smuggled

fuel and stolen crude oil have become the second-largest source of

revenue for Mexico’s cartels behind narcotics, according to the U.S.

government, which has ramped up efforts to crack down on the illicit

trade. The Trump administration designated CJNG as a foreign terrorist

organization in February 2025.

Import-export

paperwork for these transactions is often incomplete or faked by

smugglers, who use front companies to facilitate these deals and enlist

established oil industry players to help, some actively colluding,

others acting unwittingly, trade experts, tax authorities and law

enforcement officials told Reuters.

Ikon

Midstream sued Reuters for defamation on November 14 in a district

court in Texas, contending the news agency made “categorically false”

statements about its business in the October article. Reuters stands by

its reporting and is contesting the suit.

Ikon

Midstream said it never did business with Intanza. Following

publication of Reuters’ October report, Ikon Midstream provided Reuters

with internal company documents that showed the Torm Agnes cargo plus

three other 2025 shipments of diesel and naphtha aboard the tanker Torm

Louise were sold to a Mexican customer named Azteca Cone.

Azteca

Cone, like Intanza, is part of the same alleged scheme and is likewise

under investigation for fuel smuggling and suspected links to CJNG,

according to the three Mexican security sources and two of the

government security documents.

Azteca

Cone cuts a mysterious figure in the fuel industry. Just like Intanza,

Azteca Cone has no listed phone number, website or physical location

that Reuters could find....

The low-intensity war in the Middle East continues. Crude oil looks set to close the week higher for the first time in three weeks. Meanwhile, some poor earnings have hit the tech sector this week and it is evident in both Asia and the US. A dramatic revision to Ireland’s Q1 growth spurred a downward revision in Q1 eurozone growth to show a 0.2% contraction rather than a 0.1% expansion. Nevertheless, the market remains confident that the ECB will hike rates next week.

The immediate attention turns to the US May employment report. It often elicits a dramatic reaction in the foreign exchange market. The median forecast in Bloomberg’s survey is for an 88k increase. The 150k average in March and April are subject to revisions. Still, given the new Fed chair, the impact on expectations for the June 16-17 FOMC will likely be minimal and this may dampen the reaction today’s report. That said, the intraday momentum indicators appear to favor a dollar recovery ahead of the weekend....

For

most of AI’s history, humans drove every step in its development cycle.

But at Anthropic, we are delegating a growing share of AI development

to AI systems themselves, which is speeding up our work.

Taken

far enough, and given enough compute, that trend points to an AI system

capable of fully autonomously designing and developing its own

successor. This is called recursive self-improvement. We are

not there yet, and recursive self-improvement is not inevitable. But it

could come sooner than most institutions are prepared for.

Using public benchmarks and previously unreported data from within Anthropic, The Anthropic Institute

is showing that AI is already accelerating the development of AI

systems. To take just one example: today, Anthropic engineers on average

ship 8x as much code per quarter as they did from 2021-2025.

The

technical trends discussed in this piece suggest that AI systems are

going to become much more capable in coming years. These trends have

huge implications. AI that can build itself would be a major development

in the history of technology—one that could bring enormous good for the world in science, healthcare, and beyond. But full recursive self-improvement also might increase the risks

of humans losing control over AI systems. If systems are capable of

fully building their own successors, the ways we secure them, monitor

them, and shape their behavior all grow much more important.

Evidence from the outside world

The rate at which AI models improve is accelerating. The length of tasks that they can reliably complete on their own has been doubling roughly every four months, up from an earlier trend of doubling

every seven months. In March 2024, Claude Opus 3 could complete

software tasks that take humans about four minutes to complete. A year

later, Claude Sonnet 3.7 managed tasks that took about an hour and a

half. A year after that, Claude Opus 4.6 managed 12-hour tasks.1

If this trend holds, tasks that take a skilled person days could come

into range this year. In 2027, AI systems could be capable of tasks that

take a person weeks.

The

same pattern appears on coding and research benchmarks. Benchmarks

measure the performance of models in a given domain, and they’re

“saturated” when models achieve close to 100% performance.2SWE-bench

is a standard test of real-world software engineering: it hands a model

an actual open-source codebase and a real bug report, and asks it to

write a code change that fixes the issue and passes the project’s own

tests. Models have gone from scoring in the low single digits to

saturating the benchmark in two years.

CORE-Bench

tests whether a model can reproduce existing research, a prerequisite

for them to conduct original research. It gives an AI model the code and

data behind a published paper, and asks it to rerun everything and

confirm it can replicate the paper’s results. AI systems went from

succeeding at reproducing the results roughly 20% of the time in 2024 to

saturating the benchmark fifteen months later. METR, which runs the

benchmark measuring how well models can complete long-duration tasks, found

that Claude Mythos Preview could work for “at least” 16 hours and was

“at the upper end of what [METR] can measure without new tasks.”

Public

benchmarks say a lot about the capabilities of these systems. But they

can’t reveal the impact AI systems are having on speeding up AI

development itself. For that, we need direct evidence from within AI

companies like Anthropic.

Evidence from within Anthropic

Building a frontier model takes two broad categories of work. There is engineering: writing the code, standing up the infrastructure, and overseeing the model training. And there is research: deciding what experiments to run, interpreting what comes back, and figuring out which ideas to try next.

Across

both engineering and research, the picture is consistent. In

engineering, Claude can be handed an underspecified problem and figure

out how to solve it; humans supply the goal, but they no longer need to

supply the method. In research, Claude can already match or outperform

skilled humans at executing a well-specified experiment. However, large

performance gaps persist when it comes to Claude exercising judgement in

choosing goals in both engineering and research. That’s the gap between

AI today and a future system that could autonomously design its own

successor.

It’s

common for employees at Anthropic to receive more open-ended and

important tasks as they gain more experience. Early on, they execute a

task someone else specified, like, “The export button isn’t working, please fix it.” With experience, they’re handed a goal and design the approach themselves, such as, “Investigate why the network slows down under heavy load.” At the most senior levels, they are deciding which problems are worth working on at all: “What should the team build next quarter?” We can use internal Anthropic data to see how far Claude has come in being able to handle these different kinds of tasks.

Claude writes a significant proportion of Anthropic’s code. As of May 2026, more than 80% of the code we merge into Anthropic’s codebase was authored by Claude.3

Before Claude Code launched in research preview in February 2025, this

number was in the low single digits. That shift also shows up in the

amount of output per engineer. Lines of code merged per engineer per day

stayed constant through Anthropic’s first four years (2021-2024), then

began to climb upward in 2025 when Claude began to run code rather than

just suggesting it for an engineer to copy and paste. The slope

steepened again in 2026 when models began to work autonomously over

longer time horizons. These two inflection points are shown in the chart

below. In the second quarter of 2026, the typical engineer was merging

8× as much code per day as they were in 2024.4

This is because much of the code is written by Claude, with the

engineer directing and reviewing, rather than typing it themselves....

From the Food and Agriculture Organization of the United Nations, June 5:

» The FAO Food Price Index* (FFPI) averaged 130.8

points in May 2026, down 0.2 points (0.2 percent) from its revised April

level, remaining broadly stable. Increases in the price indices for

cereals and sugar were offset by declines in vegetable oils and dairy

products, while the index for meat products remained almost unchanged.

Compared to historical levels, the FFPI in May stood 3.7 points (2.9

percent) higher than a year ago but remained as much as 29.4 points

(18.4 percent) below its peak reached in March 2022.

» The FAO Cereal Price Index

averaged 114.3 points in May, up 2.9 points (2.6 percent) from April

and 5.3 points (4.9 percent) from its level a year earlier. The

continued increase reflected higher prices across all major cereals.

World wheat prices rose for the fourth consecutive month in May,

supported by smaller expected harvests in major exporters, including the

United States of America, where winter wheat crop conditions are among

the least favourable in decades, while higher fuel and fertilizer costs

added further upward pressure globally. Maize prices continued to be

supported by stronger import demand in key markets, tighter availability

in Brazil and the United States of America, and firmer energy prices

boosting ethanol-related demand. International prices of sorghum and

barley increased mainly due to spillover effects from tighter global

maize and wheat markets. The FAO All Rice Price Index increased by 2.7

percent in May 2026, as weather concerns and higher prices of crude oil

and its derivatives underpinned quotations in some leading Asian

exporting countries.

» The FAO Vegetable Oil Price Index

averaged 185.0 points in May, down 9.0 points (4.6 percent) from April,

marking the first monthly decline since the beginning of 2026. The

decrease was mainly driven by lower prices of palm and soy oils, which

more than offset increases in rapeseed oil and sunflower oil prices.

After rising for five consecutive months, international palm oil prices

declined, reflecting expectations of weaker global import demand and

uncertainty in crude oil markets. World soyoil prices showed mixed

trends, with seasonal increases in exportable supplies weighing on

prices in South America, while firm biofuel demand supported values in

the United States of America. Meantime, rapeseed oil prices rose on

seasonally tightening supplies in the European Union, while sunflower

oil quotations continued to increase, underpinned by persistent supply

tightness, particularly in Ukraine.

» The FAO Meat Price Index

averaged 130.5 points in May, almost unchanged (up 0.1 percent) from

its revised April value and 7.7 points (6.3 percent) above its level a

year earlier. Higher quotations for bovine and ovine meat, alongside a

modest increase in poultry meat prices, were almost entirely offset by a

decline in pig meat prices. International bovine meat prices rose

further in May, supported by robust import demand, particularly from

China, where import quota allocations continued to be rapidly utilized,

and from the United States of America amid persistently tight domestic

supplies. At the same time, ongoing herd rebuilding in several major

producing countries continued to constrain exportable availabilities.

World ovine meat prices increased, as higher quotations in New Zealand,

underpinned by limited supplies, were only partially offset by a

temporary easing in Australian export prices, where dry weather

forecasts prompted increased slaughtering, expanding exportable

supplies. Poultry meat prices edged up, as higher prices in Brazil,

supported by firm global import demand, were partly offset by slightly

lower quotations in the United States of America, reflecting ample

supplies. By contrast, pig meat prices declined, mainly due to lower

prices in the European Union amid abundant supplies and subdued import

demand.

» The FAO Dairy Price Index averaged

119.2 points in May, down 0.5 points (0.5 percent) from April and 34.5

points (22.4 percent) below its level a year earlier. International

butter prices continued to decline in both Europe and Oceania, as

improved milkfat availability and heightened competition among major

exporters weighed on quotations. Cheese prices eased only marginally as

ample export availability and intensified competition on international

markets were partly offset by continued support from whey and dairy

protein markets, which helped sustain values in major exporting regions.

By contrast, skim milk powder prices increased further, particularly in

Europe, supported by firm import demand from the Near East, North

Africa, and parts of Asia. Whole milk powder prices showed mixed

developments, with modest increases in Oceania, supported by seasonally

tightening export availability following the production peak and

continued demand from Southeast Asia and the Near East, largely offset

by lower European quotations reflecting subdued demand from China and

generally comfortable global supplies....

From Dunstan Ramsay's Omnibudsman substack, September 4, 2022:

The world needs to use a lot more energy

A recent article in The New Yorker

discusses the importance of refrigeration to the development of Rwanda,

where cold storage is necessary to reduce rates of foodborne illness and

secure more stable income for farmers. The piece demonstrates an

inescapable fact about the future of the world: we need to use more

energy — a lot more.

There's probably about 3 million households in Rwanda, and a vanishingly small number

have a fridge. A refrigerator uses about 2 kilowatt-hours (kWh) of

energy per day, so if we were able to get one into every household, that

would add about 2 billion kWh (2 terawatt-hours, or tWh) to Rwanda's

annual energy usage. That's about as much energy as there is contained in 1 million barrels of oil — and fully one-third of Rwanda's current primary energy consumption.

Primary energy

describes the amount of energy not just in a barrel of oil but in a

lump of coal, a gust of wind, a ray of sunshine, or a uranium fuel rod.

Energy, in general, is a measurement that describes the capacity of any

system—a cigar, a soccer player, a lightbulb—to perform work

on its surroundings. A cigar converts chemical energy into heat via

combustion; a soccer player transfers kinetic energy to a ball by

kicking it; a lightbulb converts electricity into heat and light. The

fundamental unit of energy is the joule:

roughly, this is the amount of energy required to lift a pencil one

foot into the air. Kilowatt-hours are just another measure of energy, in

this case about the amount that a medium-sized person might use in

running a 10k at an 8-minute pace.

Energy, put slightly more simply, is just a measure of how much stuff is done in the world. Access to more energy means the ability to do more stuff.

And the world needs to do a lot more stuff. Ten percent of people live in extreme poverty, and 85% live on less than $30 per day. In places like Somalia, Nigeria, and Chad, more than one in every ten children die

before the age of five. In those countries, pneumonia, which is caused

primarily by malnutrition, is among the top causes of death.

What does it take to end malnutrition? One thing that would help is, as the New Yorker

notes, refrigeration: massive amounts of fresh food spoil in the

developing world. Refrigerators are part of the solution: to fix

malnutrition, you need to get food from where it's grown to where it's

needed while it's still edible. And in order to get food between

refrigerators, you also need refrigerated trucks, which are extremely

energy intensive and of which Nigeria, a country of 200 million people,

has fewer than 1000 (it needs 25 times as many).

Those trucks will be more useful (and longer-lived) with better roads to drive them on: only about 16% of Nigerian roads are paved. You need energy equivalent to 240 tons of coal to pave 1 kilometer of asphalt, and with the need to do so for 135,000 km

of roadway, you're looking at an energy cost of roughly 2GwH — about as

much as a full square kilometer of solar panels produces each day.

Suppose now that the world has done what it takes to address pneumonia as a cause of infant mortality. What next?

Well,

then there's everything else. Just for starters, we need to set up and

run the systems that distribute clean water in order to prevent

diarrhea, the next-most-common cause of infant mortality across much of

the world. This takes energy.

It also takes energy to run dialysis machines, school buses, and

incubators for preterm babies. It takes energy to boil a pot of water on

the stove, to pasteurize milk, and to manufacture antibiotics. It takes

energy to build universities, preschools, old folks' homes, affordable

housing, bookstores and art museums, and yet more energy to provide the

air conditioning that allows students to focus and the elderly to

survive on hot days in a warming world. It takes energy just to grow

food: most of the billions of people alive today — and, with any luck,

the billions to come — owe their lives to the Haber-Bosch process,

which quite literally turns energy into artificial fertilizer for the

purposes of growing more food. That process is responsible for about 1%

of global energy consumption.

It takes energy to do all this — and we haven't even gotten to Netflix.

This reminded me that I should note First Solar surpassed its $317.00 May 2008 all-time-high* yesterday, June 3, by trading up to $320.95 and closing at $318.25. The stock also had a $320 handle this morning ($320.64) before reversing to close down $3.30 at $314.95. Fingers, toes and other body parts crossed that we didn't just see a double top.

From Reuters, June 4/5:

Storage gets bigger display at world's largest solar exhibition

Solar majors make battery foray, lean on supply chain networks

Jinko to nearly triple battery-making capacity this year

China's major solar panel manufacturers are ramping

up higher-margin battery exports to boost revenue as growth in

photovoltaic (PV) sales slows, betting on rising global demand for

renewable energy storage to cut reliance on fossil fuels.

The sector has been hit by weaker domestic installations, slowing exports and record-low prices, with executives expecting global demand to decline in 2026.

That has pushed players including JinkoSolar (688223.SS), JA Solar (002459.SZ), LONGi Green Energy (601012.SS), and Trina Solar (688599.SS), to accelerate expansion into battery storage, company executives told Reuters.

JinkoSolar

plans to nearly triple its battery manufacturing capacity from 5

gigawatt-hours (GWh) to 13-14 GWh by the end of this year, as developers

seek to address the intermittency of renewables, a company official

said at SNEC - a solar industry gathering attended by over half a

million people.

"We

are seeing some goodwill from our company's directors' point of view,

in that we are having massive investments," Titus Koech, a regional

technical head for energy storage systems, told Reuters.

Countries

with high renewable penetration - including Japan, Vietnam and India,

as well as Germany, the Netherlands, the U.S. and Australia - were

among the largest importers of batteries from China in 2025, according

to energy think tank Ember.

At

JA Solar's booth, energy storage products took centre stage, marking a

shift from PV-focused displays in previous conferences, said Gloria Gao,

marketing director of its storage unit.

"If

you only own a solar business, it's not helping your business grow

because the margins are really small. That's why we started our energy

storage business, because we foresee the future," Gao told Reuters.

Solar

panels exports, which typically carry better margins than domestic

sales, grew 4.7% in 2025 - the slowest pace since 2018, Ember data

showed. Growth from May to December is expected to lag that seen in

the first four months of the year, Rystad Energy analyst Fei Chen said.

By contrast, battery exports for energy storage are forecast to jump 30% to 150 GWh in 2026, Rystad said.

ONE-STOP-SHOP VERSUS BATTERY MANUFACTURING GIANTS

China's solar manufacturers are entering a market dominated by battery giants such as CATL and BYD, but are betting on their supply-chain expertise and ability to offer integrated solar-plus-storage solutions....

I'm not sure that's a good idea but I haven't had much luck with companies run by attorneys either. With the lawyers they either remain in the "Thou shalt not" groove of the wise counselor or they go a bit nuts because they think they're no longer an officer of the court.

With the analysts you, somewhat surprisingly, run into the same problems you do with economists: "Sure, it works in practice but will it work in theory." And the "On the other hand..." stuff. Don't even get me started on Elliot Wave practitioners with their alternative wave counts introducing a third and a a fourth hand.

Anyhoo, the equity analysts are going to need to do something after AI takes their jobs so maybe give them a shot at the C-suite. But watch those hands.

From Financial News London, May 25:

It might seem an unlikely move, but capital markets experience is increasingly valuable in the C-suite

Standard Chartered had some compelling reasons to promote Manus Costello -

As

a former equity analyst who covered the bank for many years, Costello

is very familiar with the bank’s strengths and weaknesses, and those of

its rivals. He knows its investors well, understands what they are

looking for and speaks their language.

Since

joining Standard Chartered as head of investor relations two years ago,

Costello has built a good rapport with chief executive Bill Winters,

who says he has made a “significant contribution to the group’s

strategic positioning and engagement of stakeholders”.

While

very familiar with the business he also brings an outsider perspective

that many management experts would say is an ideal combination.

Yet

this raises a question: if it is such an obvious move why don’t more

analysts become senior executives in the sectors they have covered?

In

financial services, the numbers are strikingly small. One of the few

prominent examples is Sallie Krawcheck, who made her name as an

independent-minded analyst of Wall Street banks at Sanford Bernstein. In

2002, she was hired by Citigroup to rebuild trust in its research and

wealth management business after accusations of conflicts of interest.

Two years later she was appointed Citi’s chief financial officer.

In

the UK, Luke Ellis, former chief executive of hedge fund manager Man

Group, previously worked for JPMorgan, though in equity derivatives

rather than research.

Another former

analyst who is now a chief executive is Anthony Noto. A one-time

Goldman Sachs internet analyst, Noto was appointed head of financial

technology firm SoFi in 2018. But Noto shifted into banking at Goldman

before going into the industry, which makes him a slightly different

case.

There are plenty of bankers who move into the industry they covered. Current examples include Jonathan Sorrell, the former Goldman banker who now heads wealth management group Rathbones....

It looks like the drought intensities decreased a bit while the areas affected remained about the same.*

From the University of Nebraska-Lincoln, June 4:

This Week's Drought Summary The mid-level height anomaly pattern during the week exhibited an omega-block type pattern, with mean troughing over Alaska and both the West and East, with the western trough cutting off over California, and strong ridging between the troughs across the central contiguous US. This pattern promoted below-normal temperatures across the Southwest for much of the period, with colder air pushing eastward towards the end of the week followed by warming temperatures. Across the East, cooler air overspread New England and the mid-Atlantic, keeping evapotranspiration rates a bit lower than normal. In contrast, much above-normal temperatures were observed throughout the week across the northern Plains and upper-Midwest, though colder weather and storminess overspread the northern Rockies and adjacent High Plains at the end of the week.

An active pattern was noted across

the Plains, South, and Southeast as a mean frontal boundary provided a

focus for stormy weather. These rains, in conjunction with a wetter

pattern overall during May, prompted widespread additional drought

relief for the South and Southeast regions, as well as portions of the

High Plains. In contrast, hot, dry weather across the northern Plains

and upper-Midwest caused expansion of drought and abnormal dryness, with

widespread degradation occurring in western portions of the Midwest

region. Towards the end of the week, a storm system brought heavy

precipitation to western and central Montana, bringing some drought

relief following a period of hot, windy weather. Across the Northeast,

additional rainfall benefitted portions of New England, while drier

weather overspread the mid-Atlantic and southern New England following a

wet week previously.....

*****

....Looking Ahead

At the start

of the next 7 days, drier conditions are favored across much of the

East, with daily temperatures quickly warming to above-normal. A storm

system now over the Plains will progress slowly eastward, bringing a

potential for much needed rainfall across the upper Midwest and Great

Lakes region. Current QPF forecasts from the Weather Prediction Center

show amounts potentially exceeding 1.5 inches across much of Iowa and

far southwestern Wisconsin, but lighter amounts elsewhere will likely be

insufficient to overcome the high demands coming from much above-normal

temperatures and summer agriculture, especially across Illinois,

Indiana, and northern Minnesota. A gradual return to a summer convective

regime is favored across the Southeast during the week, but

accumulations are forecast to be less than what fell over the past few

weeks, especially across northern Florida and east of the Appalachians.

Seabreeze-driven convection is favored to remain active across South

Florida. Mostly dry conditions are favored across the West, with a storm

system bringing some precipitation to the Pacific Northwest. Meager

precipitation is forecast for the Northeast region, raising concerns for

a return of short term drought impacts....

“I could end the deficit in five minutes,” he said. “You just pass a law

that says that any time there’s a deficit of more than three percent of

GDP, all sitting members of Congress are ineligible for re-election.

Yeah, yeah, now you’ve got the incentives in the right place, right?”

—Warren E. Buffett, retired insurance salesman, Omaha Nebraska

To Boldly Go: The Case for Space Datacenters Space DC Total Cost of Ownership Explained. Unpacking constraints from Terrestrial DCs and Chip Production. Space-Earth Parity in the late 2030s, Space DCs could start to be viable even sooner.

Everyone has been talking about datacenters in space. Interviews

given by Elon Musk in the past few months have spent lots of time on

orbital compute:

“Five years from now, my prediction is

we will launch and be operating every year more AI in space than the

cumulative total on Earth... I would expect to be at least, sort of five

years from now, a few hundred gigawatts per year of AI in space and

rising.” - Elon Musk on Dwarkesh Podcast, February 2026

Furthering

space-based compute was also one of the stated motivations behind the

merger of xAI into SpaceX (as a ‘reorganization of entities under common

control’), and is a key part of SpaceX’s plans to go public, as stated

in their S-1 filing on 20 May 2026.

“Our

goal over time is to launch 100 gigawatts of compute to space each

year. If operated continuously, the generation resources used to support

100 gigawatts of compute could generate approximately one-fifth of the

annual power production in the United States, which was 4.4 thousand

terawatt hours in 2025… We expect space‑based compute to massively

increase AI compute scale, while also improving token economics.” - SpaceX, S-1 Filing, May 2026

As

expected, many part-time prognosticators in the Substack-verse have

emerged from the woodwork to weigh in on the concept. Some articles

bring up insightful points, but there are more than a few that are built

upon ideas that fly in the face of science.

A few casual arguments made in favor of space datacenters include the following:

Space can provide free solar energy 24 hours a day

Cooling is “free”. Some erroneously point to space being cold as a key positive

Communications latency in space is low as you’re just sending light through a vacuum

There is no need for permitting in space… so far…

Many

of these points sound like they hold merit on the surface, but a deeper

analysis of each apparent advantage reveals a far more complex story.

While

we think that it is possible that space datacenters could scale one

day, deploying orbital compute using today’s technology currently costs

several times more than deploying terrestrial compute. Achieving

Space-Earth cost parity will require significant engineering work,

material science breakthroughs and cost scaling progresses and will

still take years to achieve. There are also important reliability and

servicing obstacles to overcome - for instance - how GPU servers will

recover from faults that require human intervention, effectively

shielding accelerators from radiation, among many others.

When we deploy compute in space, it won’t be because of the four superficial reasons we have cherry-picked above. Rather, Space-based

datacenters make sense in the world where AI demand well exceeds all of

the four layers of terrestrial datacenter supply that we will introduce

below. For Space datacenters to step up to this call -

it is a necessary condition that major space datacenter cost items like

radiators, solar arrays and launch costs decline considerably, and that a

number of key operational obstacles are overcome.

Users of our AI Space Datacenter TCO Modelcan

see a first-principles, system-level framework for evaluating orbital

compute economics, engineering constraints, and supply-demand dynamics

across both terrestrial and space-based infrastructure.

The four layers of incremental power supply for terrestrial datacenters include:

Grid-connected supply,

Converted bitcoin miners and powered land,

Behind the meter generation, and finally,

Industrial capacity and manpower to build further power infrastructure.

A

necessary condition for AI related IT equipment demand to reach levels

exceeding terrestrial datacenter supply is for there to be enough chip

fabrication capacity to fulfill this demand in the first place, before

we even discuss datacenters! We wrote about this in great detail in our

recent article on the Great AI Silicon Shortage,

where we concluded that the industry has moved from a power-constrained

to an accelerator-constrained regime. Available datacenter capacity and

power now exceed AI compute demand, but TSMC’s N3 wafer capacity and

HBM supply cannot keep pace with the pace of accelerator deployments.

This means that today, and for the next few years, chip manufacturing

will be the global constraint before we even worry about supply for

these four layers.

The chip constraint forms a separate

fifth layer of supply - Semiconductor Production, and it is a

“universal” constraint on all chip deployment, whether deployed on Earth

or in Space. Users of our AI Space Datacenter TCO Model

can see how this constraint applies well into the future, and under what

scenarios regarding chip manufacturing capacity addition that

Semiconductor Production may not be the constraint.

Elon Musk is clearly well aware of this constraint, and it is the impetus behind his Terafab Initiative. The AI Space Datacenter TCO Model also includes knobs and sliders for users to tune to test out various Terafab scenarios.

Framing the Space Datacenter Debate Our various industry models such as the Accelerator Model, the Foundry Industry Model and WFE Models illustrate the aforementioned chip tightness. Meanwhile our AI Datacenter Model forecasts accelerating incremental datacenter additions in 2027 and 2028. Thus, datacenter capacity addition will run ahead of chip constraints in the next few years until fab capacity additions accelerate to catch up. Our suite of industry models will only forecast such wafer fab and datacenter capacity additions once such plans are confirmed.

However, the world in which AI demand is so

overwhelming as to exceed the already formidable datacenter capacity

additions is a world with no time for half measures. As such, our AI

Space Datacenter TCO Model base case departs from our industry models to

reflect this world, assuming accelerating incremental datacenter

capacity additions and a meaningful step up in the pace of chip fab

capacity addition. It is a world where all the stops are pulled out and

many obstacles from gas turbine availability to EUV tool production

constraints are overcome because clear long-term AI end use ROI

justifies enough capital investment to overcome them.

The below

chart illustrates what this world could look like - with incremental

datacenter capacity additions eventually in the hundreds of GW annually,

though adding chip capacity will still be more difficult than adding

datacenter capacity....

Israel and Lebanon raises hopes of a breakthrough in US-Iran talks where a low intensity conflict has been waged under the flag of a ceasefire. The Israel-Lebanon deal reportedly does not include Hezbollah, underscoring the fragility and limits of the ceasefire claims. July WTI is near the middle of the $94-$96 range. The market seems cautious.

The US dollar is mostly softer, with the Canadian dollar the weakest among the G10 currencies. The swaps market has a BOJ hike nearly fully discounted for later this month and the greenback continues to hover near but below JPY160. Japan’s finance minister continued to press with recent rhetoric that it stands ready to act. Poor earnings from Broadcom late yesterday weighed on the chip sector in Asia and has dragged the Nasdaq futures down over 1%. The market-sensitive US May jobs data are due tomorrow but the bar to a change in Fed policy this month, as Warsh chairs his first meeting is very high....

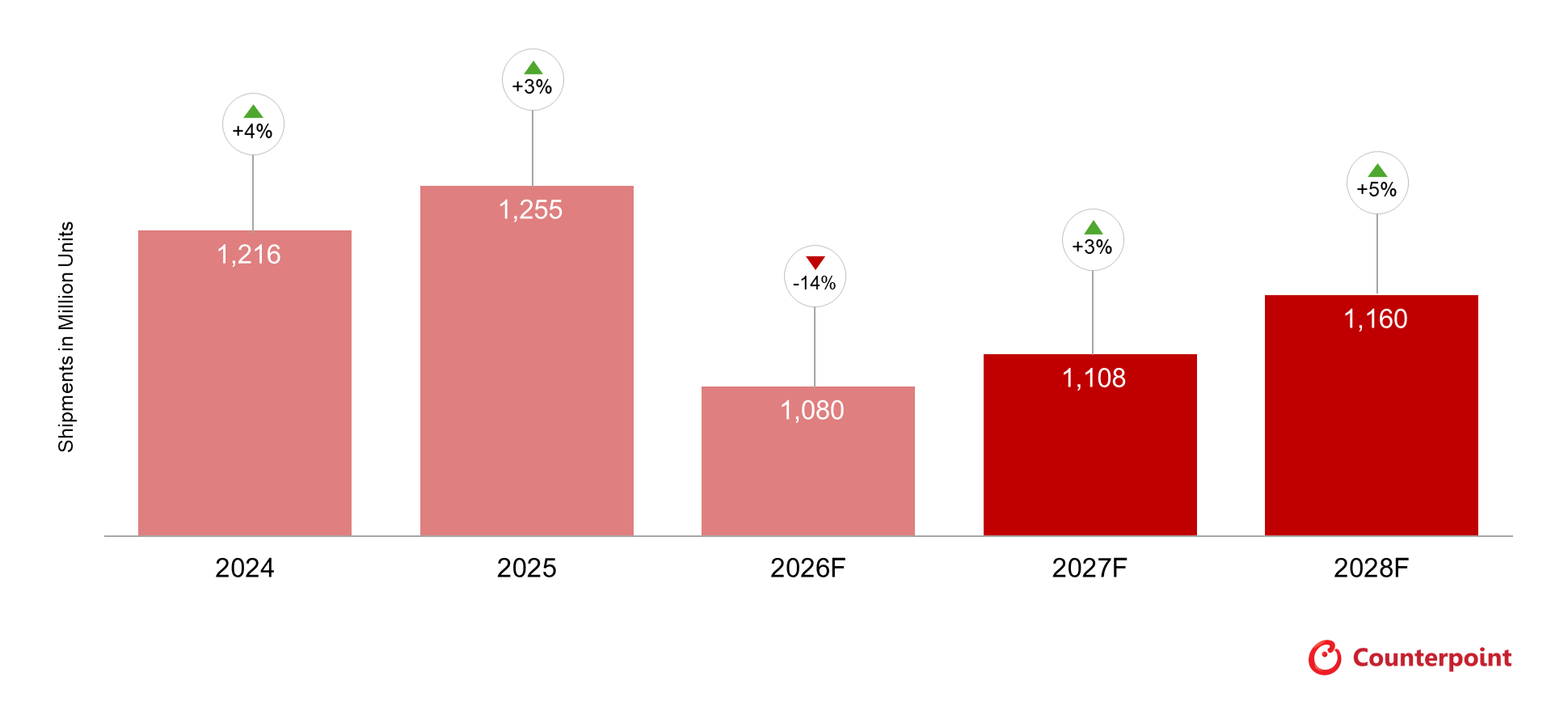

Global smartphone shipments are now forecast to fall 13.9% YoY in 2026, dropping to 1.08 billion units, the lowest annual volume since 2013, and a steeper contraction than our February forecast of 12.4%.

A memory supply crisis, driven by capacity reallocation toward AI-focused HBM and server DRAM, is the primary driver of the downturn, with LPDDR4/5 prices expected to treble in Q2 2026 relative to Q4 2025, per Counterpoint’s Memory Service.

Lower-end OEMs and Emerging Markets face the sharpest pressure, with LPDDR4 memory supply tracking to a decline of over 40% in 2026; the sub-$150 segment faces an effective permanent removal in some markets.

Apple and Samsung are the most insulated OEMs, while Huawei is the only Chinese brand expected to grow shipments in 2026.

The Iran conflict and the closure of the Strait of Hormuz add a geopolitical dimension to the downturn, though macroeconomic headwinds are expected to be materially less severe than the post-Ukraine inflationary shock.

Seoul, Beijing, Berlin, Buenos Aires, Fort Collins, Hong Kong, London, New Delhi, Taipei, Tokyo – June 1, 2026

The global smartphone market has entered its deepest period of contraction on record, according to Counterpoint Research's latest Smartphone Market Outlook Tracker, with full-year 2026 shipments now forecast to decline 13.9% YoY to 1.08 billion units, a downward revision from the 12.4% decline projected in February. The trigger is a worsening memory supply crisis that has accelerated sharply in recent weeks, compounded by the outbreak of the Iran conflict.

Global Smartphone Forecast, May 2026 Edition

Source: Counterpoint Research Smartphone Market Monitor and Market Outlook, May 2026 Update

Memory crisis deepens the 2026–2027 downturn

The Q1 2026 smartphone market retreated 3.1% YoY, marking the first decline after nine consecutive quarters of growth. The performance was nonetheless better than expected, as OEMs moved to front-load shipments and clear pre-shock inventory ahead of expected price increases. However, the deterioration since has been sharp. Counterpoint Research's Memory Service indicates that mobile LPDDR4/5 prices in Q2 2026 are on track to treble relative to Q4 2025 levels, with the squeeze expected to persist through H2 2027 given the capital intensity and lead times inherent to semiconductor manufacturing.

The damage is falling disproportionately on lower-end devices. LPDDR4 supply is expected to decline more than 40% in 2026 as fabs reallocate capacity toward AI-driven HBM and server DRAM, making it increasingly uneconomical to supply entry-level products. Globally, smartphone wholesale prices rose 14% in Q1, and the pace will sustain as pre-shock inventory is exhausted. Certain sub-$150 price tiers face effective permanent ejection from the market.

Principal Analyst Yang Wang commented, “The memory crisis is the most disruptive supply-side event the smartphone industry has ever faced. Unlike demand-driven slowdowns, such as seen during COVID and 2022-23, the current contraction will not respond to pricing, channel and product planning adjustments. OEMs in the low- and mid-tier are caught between unabsorbable cost increases and consumers with hard affordability ceilings. The narrative around the smartphone market is no longer how to grow shipments or market share, but whether to remain in the market at all.”

Premium resilience, OEM divergence, and the road to recovery

So the question becomes: Will the increase in average selling price brought about by the shift to more expensive phones be large enough to offset the decline in unit volume?

Dent is a type of field corn. A long way for a not-very-good play on words

First up, from Xinhua via People's Daily, June 4:

Chinese scientists develop high protein maize in animal feed quest

Chinese scientists have identified two key genes for high protein

content in maize and have managed to develop high protein varieties,

offering a promising solution to China's animal feed protein shortage.

Maize is China's largest grain in terms of production volume,

however, its protein content is generally low, only about 8 percent,

leading to a heavy dependence on imported soybean meal as a protein

source for livestock, according to Wu Yongrui, deputy director of the

Center for Excellence in Molecular Plant Sciences (CEMPS) of the Chinese

Academy of Sciences (CAS).

In 2025, China's soybean imports exceeded 100 million tonnes. Raising

maize protein content by just one percentage point would be equivalent

to the protein contained in approximately 8 million tonnes of imported

soybeans, Wu said.

Therefore, developing high protein maize to replace imported soybean

meal in feed is a promising tactic in seeking to address the country's

feed protein shortfall. Yet, for a long time, breeding efforts had

lacked access to superior high protein genes, Wu noted.

Research has found that wild maize contains protein levels as high as

30 percent, but after over 9,000 years of domestication and modern

breeding, most of these genes have been "lost" in contemporary varieties

due to the absence of targeted selection for protein content, Wu

explained.

In 2022, a research team led by Wu identified the first high protein

gene, THP9-T, from wild maize, achieving a preliminary boost in protein

content for major domestic maize cultivars. However, further

breakthroughs in maize protein content remained a significant challenge.

Through persistent efforts, the team successfully identified a second

high protein gene, THP3-T. Multi-year, multi-location field trials

demonstrated that this gene can increase kernel protein content from 10

percent to over 13 percent in inbred lines without compromising yield,

while also enhancing whole-plant protein content and enabling the maize

to grow well and remain protein-rich with less fertilizer, Wu said.

Further research revealed that combining THP3-T and THP9-T produces

an unprecedented synergistic effect, raising kernel protein content in

inbred lines from 10 percent to 15 percent -- far exceeding the impact

of either gene alone.

"The research not only discovered the 'key puzzle piece' for high

protein maize breeding but also offers new possibilities for quality

improvement and precise genetic enhancement of modern maize," Wu said.

The team has employed marker-assisted breeding technology to

precisely improve over 80 parental lines of major maize cultivars in

China, raising their protein content to more than 14 percent.

The team also successfully increased the kernel protein content of

Zhengdan958, China's most widely cultivated maize hybrid, from 8.5

percent to over 12 percent.

Wu said that China produces approximately 300 million tonnes of maize

annually. If the protein content of maize used for feed nationwide were

raised by four percentage points to more than 12 percent, the total

added protein would be equivalent to over 30 million tonnes of imported

soybeans, which is roughly 30 percent of current soybean imports....

The

discovery of oil in Persia (modern-day Iran) in 1908 marked a

significant turning point in the region's economic and political

landscape. The process began when Moẓaffar od-Dīn Shāh, the Qājār

Dynasty's ruler, sold exploration rights to William Knox D'Arcy, a

wealthy Englishman. Despite initial challenges, including harsh weather

and a lack of skilled labor, D'Arcy's venture bore fruit when oil was

struck at Masjed Soleymān, leading to the establishment of the

Anglo-Persian Oil Company in 1909. This discovery attracted British

government interest, especially as the internal combustion engine gained

importance, further integrating Persian oil into global markets.

The

geopolitical implications of this find were profound, as both Russia

and Britain sought to protect their interests in Persia during World War

I. Subsequent developments included efforts by local leaders, such as

Reza Khan, to negotiate better terms for oil profits, reflecting a

growing nationalistic sentiment. This historical moment laid the

foundation for Iran’s complex relationship with foreign powers,

particularly regarding oil control, which continued to evolve through

the 20th century, culminating in significant political upheaval,

including the 1979 revolution. The discovery of oil thus not only

transformed Persia's economy but also its political dynamics and

international relations.

Full Article

DATE May 26, 1908

The discovery of oil in Persia by an Englishman who had purchased

oil concession rights gave Great Britain control of Persian oil, making

Persia of tremendous strategic importance during two world wars. The

discovery also initiated the opening of the Middle East to oil

exploration and development, making the region of vital importance to

the world economy. Initial Western control of oil production produced an

anti-imperialist reaction that remained for many decades.

LOCALE Masjed Soleymān, Persia (now Iran)

Key Figures

William Knox D’Arcy (1849-1917), British entrepreneur

Moẓaffar od-Dīn Shāh (1853-1907), Qājār shah, r. 1896-1907

Reza Khan (1878-1944), nationalist and secular reformist shah of Iran, 1925-1941

Mohammad Reza Shah Pahlavi (1919-1980), shah of Iran, 1941-1979

Mohammad Mosaddeq (1880-1967), nationalistic prime minister of Iran, 1951-1953

Sir Percy Sykes (1867-1945), British general in charge of protecting Persian oil fields during World War I

George B. Reynolds (fl. early twentieth century), leader of D’Arcy’s oil drilling team

Summary of Event

During the last half of the nineteenth century, Persia (modern-day

Iran) was of interest to Europeans mainly for its fine carpets and for

whatever monopolies could be gained from monetary gifts to the corrupt

shahs (emperors) of the Qājār Dynasty. By 1900, Russian interests

controlled the five northern Persian provinces, while the British sphere

was in the south and controlled monopolies for commodities such as

tobacco. It was business as usual when Moẓaffar od-Dīn Shāh sold a

concession to a wealthy Englishman, William Knox D’Arcy, who had made

his fortune mining gold in Queensland, Australia. For ten thousand

pounds, D’Arcy purchased the rights to explore, develop, and sell natural gas,

petroleum, and asphalt in all of Persia, except for the five northern

provinces controlled by Russia, for the next sixty years. After two

years, D’Arcy was required to form a company and give the shah twenty

thousand additional pounds and twenty thousand pounds in shares of the

company’s stock. The shah was also to receive 16 percent of any profits

from annual oil revenues.

The natural seepage of oil from the ground in Persia, which had been

used for centuries to caulk boats and bind bricks, attracted European

interest in the 1870’s as technology for oil drilling developed. Baron

Julius de Reuter (founder of Reuters News Agency)

made two unsuccessful efforts to locate oil, and in the early 1890’s a

French geologist surveyed western Persia and published a scientific

paper on the region’s oil-producing potential. These efforts sparked

D’Arcy’s interests and resulted in his 1901 purchase of the shah’s

concession. That year, D’Arcy hired George B. Reynolds, one of the few

Englishmen with experience in oil exploration, and sent him to find oil

fields in western Persia.

From 1901 to 1905, Reynolds drilled for oil without success. Harsh

weather conditions, difficult terrain, and the shortage of skilled labor

slowed progress. Running low on capital, D’Arcy signed an agreement

with the Burmah Oil Company, a British corporation, to gain the funding

necessary to continue exploration. Reynolds began drilling in southern

Iraq, but through 1906 and 1907 he continued to lose money. The venture

was close to collapse when, at 4:00 P.M. on May 26, 1908, oil began to

gush over the top of oil rig number one at Masjed Soleymān, rising to a

height of fifty feet above the rig. Two more wells were sunk, with

equally productive results. The first major oil strike in the Middle

East had been made. Today, a small outdoor museum preserves what is

known as Well Number One, which still retains its original rig, boiler,

and pump.

In 1909, the Anglo-Persian Oil Company was founded. D’Arcy led the

company, and by the time of his death in 1917 he had made a massive

fortune, despite the fact that he never set foot in Persia and operated

only through his agents. The company began construction in October,

1909, and by 1911 the number of employees had risen to twenty-five

hundred. The export of oil began in 1912, and by 1914, thirty oil wells

had been drilled at Masjed Soleymān....

Senior government officials have warned Russian President Vladimir Putin

that spending on the war in Ukraine is on an unaffordable path, the

most serious sign of internal division in Moscow since the full-scale

invasion began.

Officials

in Russia’s Finance Ministry and central bank have advised the Kremlin

that the current level of projected defense expenditure risks the

government’s budget deficit widening dangerously, according to people

familiar with the matter and documents reviewed by Bloomberg News.

The

officials, who have grown increasingly concerned about the state of

Russia’s economy and state budget in recent months, have proposed new

cuts to defense spending, the people said. It will be difficult to mend

the country’s stretched public finances without finding further

efficiencies, they have advised.

However,

a divide among policymakers has seen senior officials in the Defense

Ministry and some in the Kremlin, who are determined to pursue Putin’s

war aims, insist on protecting military expenditure. Reducing it would

badly damage the economy because so many businesses are reliant on

military-related contracts, they have argued.

Putin

has asked Finance Ministry officials to find spending reductions in

other budget areas before targeting defense, some of the people said.

They were all granted anonymity discussing the concerns, the extent of

which has not been made public.

Kremlin spokesman Dmitry Peskov didn’t immediately respond to a request for comment.

The

Defense Ministry is not only resisting cuts but is demanding additional

funding, according to two people close to the Russian government.

Military expenditure will have to increase to address a shortfall as

high as three trillion rubles ($36 billion) this year, they said.

The

president has been aware of the budgetary pressures both last year and

this year, so the challenges aren’t a surprise, the people said. The

scale of any spending cuts will depend solely on Putin, as no major

budget decisions are made without his approval and he acts as the

ultimate arbiter, they said, describing that as an iron rule.

When

the 2026 budget was drafted, officials understood that a funding gap of

roughly 1.2 trillion to 1.5 trillion rubles could emerge in the second

half of the year, money that might be needed for the defense sector.

At

the time, there were hopes the war in Ukraine would end following the

summit in Alaska last August between Putin and US President Donald Trump,

which would have made a reduction in defense spending in the second

half of 2026 a logical assumption, according to the people close to the

Russian government....