From Wolf Street, February 13:

But that’s how inflation is, once out of the bottle: It serves up nasty surprises.

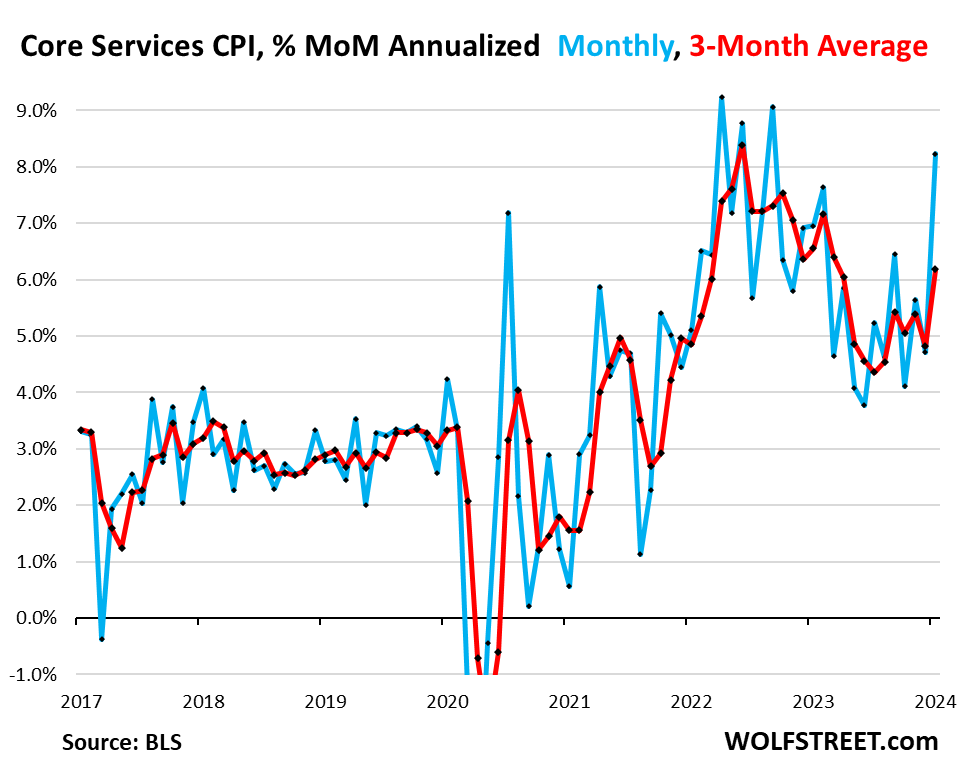

We’ll start with the “core services” CPI (services minus energy services) because this is so crucial, and because Powell keeps talking about it. We have been concerned here for months about the refusal of core services inflation to ease off, and we’ve found the acceleration in the fall last year “very disconcerting.” But that’s how inflation is – it tends to serve up nasty surprises. And now it did.

“Core services” CPI jumped by 0.66% in January from December, or by 8.2% annualized (blue). In this inflation cycle, only three months were worse (April, June, and September 2022). It includes housing, insurance, health care, subscriptions, etc., but not energy services. Core services is where consumers do the majority of their spending – and it’s re-heating from already hot levels.

The three-month moving average, which irons out the month-to-month squiggles, jumped by 0.50%, or by 6.2% annualized (red), the worst since March 2023. All this according to the CPI data released today by the Bureau of Labor Statistics.

Inflation in January boiled down to this:

- Energy prices continued their plunge (-10.4% annualized in Jan. from Dec.).

- Prices of durable goods continued their decline (-5.4% annualized in Jan. from Dec.), on a plunge in used-vehicle prices.

- But food prices rose (+4.5% annualized in Jan. from Dec.).

- And “core services” were red hot (+8.2% annualized).

“Core CPI,” a measure of underlying inflation that excludes food and energy products, accelerated to an increase of 0.39% in January from December, or 4.8% annualized (blue line), the highest since April last year. It was held down some by the decline in durable goods CPI, but pushed up more forcefully by core services CPI.

The three-month moving average of core CPI accelerated to 4.0% annualized in January from December, the worst reading since June (red line)....

....MUCH MORE

Earlier this week:And the Cleveland Fed Inflation Nowcast, which has been running cool—.13% for the just reported January monthly figure vs. .20% consensus and .30% actual—is nowcasting .37% headline for the February release in the second week of March. That's creeping back toward 5% annualized.