From Wolf Street:

Markets have a way of blowing this type of consensus out of the water.

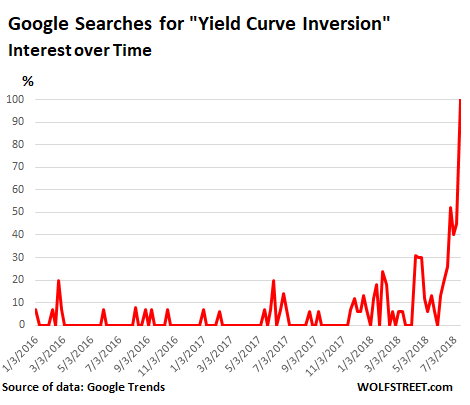

The phrase “yield curve inversion” may not be up there with “Taylor Swift” or “Kim Kardashian,” but it has by now cropped up in the media so often that people are Googling it all of a sudden:

Markets are by now taking this “yield curve inversion” for granted. It’s going to happen, it’s just a matter of time, they say, and whether it’ll be next week or at the next rate hike is not crucial.

This idea that the yield curve must invert is based on the principle that the Fed is raising its target range for the federal funds rate, an overnight rate, and that these higher rates are filtering into short-term Treasury yields, such as the one-month yield, the three-month yield, or the two-year yield. Meanwhile, the 10-year and 30-year yields are doomed to be stuck. And when the two-year yield gets pushed above the 10-year yield, that’s the moment of “inversion.”

An inversion of the yield curve, which happens rarely, has become a popular and accurate recession indicator over the past decades. The last time it inverted was followed by the Financial Crisis.

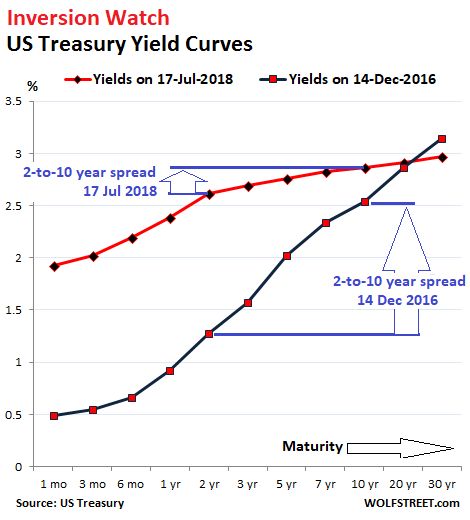

Today, the two-year yield closed at 2.62%, the highest since July 2008. The 10-year yield closed at 2.86%. The difference of 24 basis points is the narrowest spread since before the Financial Crisis.

The chart below shows the yield curves on December 14, 2016, when the Fed got serious about raising rates (black line); and today (red line). Note how the red line has “flattened” compared to the black line. The spread between the two-year and the 10-year markers, at just 24 basis points today, is minuscule compared to the 127-basis point spread on December 14, 2016:

If the 10-year yield remains at 2.86%, and if the two-year yield rises 25 basis points to 2.87% (likely by the next rate hike), the two-year yield would be higher than the 10-year yield, and the curve would be inverted.Recently:

The chart below shows how the spread between the two-year yield and the 10-year yield appears to be headed to zero – a flat yield curve – or below zero, which would be the inversion moment:...MUCH MORE

Dancing on the Edge of a Volcano: "The yield curve needs to be respected"—Jeffrey Gundlach

ICYMI: "U.S. Yield Curve to Invert in Mid-2019, Morgan Stanley Says"

"As the Yield Curve Flattens, Threatens to Invert, the Fed Discards it as Recession Indicator"

"Who’s Afraid of a Flattening Yield Curve?"