Or something.

That's my headline, not the one at ZH.

From ZeroHedge:

Albert Edwards: The Fed Is Trapped In An Epic Bubble, It Can Never Normalize Rates Again

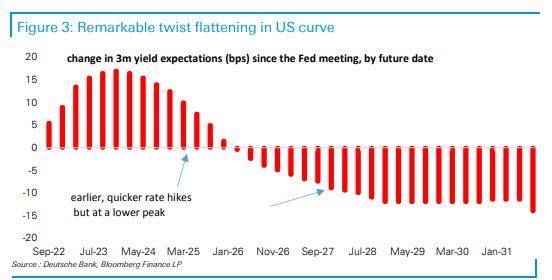

One week ago, we explained why the Fed made a huge policy error last Wednesday when its latest dot plot showed two rate hikes: in simple terms, while market pricing for hikes in 2023 and 2024 went up, yields beyond that dropped as the market said that the best the Fed can do is less than 2-years of rate hikes.

Said otherwise, if the Fed decides to hike - as first Powell hinted and then Bullard doubled down on Friday sending stocks plunging - the market is saying that it won’t be able to go very far before inflation and growth hit a speed limit, pushing yield expectations after the initial hike lower.

This very pessimistic view on r*, first laid out here in 2015, is also in line with market behavior beyond the bond market. First, as Deutsche Bank's FX strategist George Saravelos said, it is aligned with the very high dollar responsiveness we have seen to even small shifts in Fed stance: huge pent-up demand for yield from investors across the planet forces a stronger dollar and a bigger disinflationary impact quicker than assumed. In other words, a low global r* (remember the rest of the world still has massive current account surpluses, or excess savings) pushes US r* even lower.

Second, a low r* is consistent with continued equity resilience, especially in growth stocks heavily reliant on a low medium-term discount rate. That the equity moves in the past two days were led by huge relative rotation from the Russell to the NASDAQ should not be a surprise. This, as Deutsche Bank ominously warns, is 2010-19 secular stagnation pricing, version 2.

Here, another, even bigger question emerged: will the US even be able to sustain positive GDP growth absent trillions in new stimulus each and every year? And even more ominous: what happens to inflation if the Fed is forced to cut rates well before the inflationary burst is extinguished? These are among uncomfortable questions markets will have to answer in the coming months.

* * *

Fast forward to today when SocGen's in-house permagrouch, Albert Edwards, offered an answer to all of these critical questions posed by the Fed: according to Edwards, the market does not have to worry much about such trivial questions as "is inflation transitory or not" for the simple reason that The Fed’s ambition to normalize rates can never be achieved.

Picking up on the observations made by Deutsche Bank's head of FX, Edwards writes that while the global reflation trade was already in retreat, its head of lobbed off by the Fed in its surprisingly hawkish statement of intent last week, a "retreat which quickly turned into a rout across many asset classes."

And while it was not quite in the same league as Bernanke's 2013 "Taper Tantrum" it clearly demonstrated the market’s sensitivity to the Fed’s intentions, fickle as they may be. The biggest surprise: after an initial selloff, the long end of the bond market rallied - in contrast to the sharp sell-off in 2013, or as Edwards echoes what we said: Maybe the market now realizes that a Fed tightening cycle is impossible?

Referencing a WSJ article by the Fed's former mouthpiece, Edwards writes that according to Jon Hilsenrath there are two explanations.

- First, the Fed has done a better job communicating its intentions this time round (personally I think not).

- Secondly and more worryingly, Hilsenrath writes that the markets could be too complacent.

Edwards next notes that according to Jeremy Stein who was a Fed Governor during the 2013 tantrum, the markets shouldn’t take a benign view of the extent of potential tightening as “The Fed cannot support markets if there’s an inflation surprise.” He said that Fed Chair Powell, his former colleague, has been adept at shifting his stance when needed. Despite the market’s tranquillity today, he said, Powell may need that nimbleness in the months ahead. Indeed, Mr. Powell said in a June 16 news conference “We will do what we can to avoid a market reaction. But ultimately, when we achieve our macroeconomic goal, we will taper as appropriate”.

The permacynical Edwards then explodes, and says that when he reads those sorts of statements, he "literally laughs out loud" and asks "is this the same Jerome Powell who at the end of 2018, after talking tough for months about the unwinding of the Fed balance sheet being on “auto-pilot” did a 180 degree about turn when markets began to swoon at the end of that year? He is indeed nimble – in retreat!"

Perhaps Edwards is no longer alone in his uber skepticism: after all none other than Bank of America recently said that everyone knows the Fed will stop tapering as soon as the S&P drops 10%... which isn't a good sign when it comes to Powell's credibility.

So why does Edwards think the bond market reacted inversely to its Taper Tantrum shock? "In my opinion the bond market rallied because they know that Fed easy money comes at a heavy price."

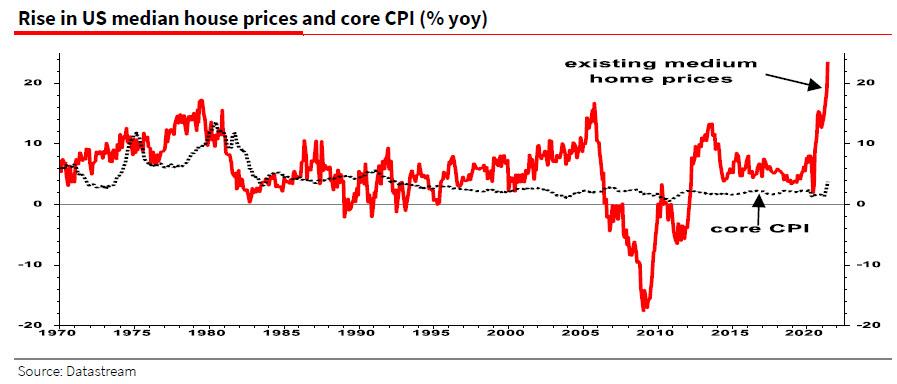

It's not just that: with the Fed having gone all in on reflating everything, not just the economy and stock market but the housing market too, a crash in any of the three would result in an immediate depression. That's why Edwards thinks that the bond market "just doesn’t believe the Fed can follow through on its tougher talk. Why? Because having created another huge, real-terms house price bubble, they are trapped"...

... which confirms what we have said since 2009: that "central banks have become slaves to the bubbles that they blow – the markets quickly forcing a reversal of any tightening. This time around will be no different."....

....MORE