As the kids say IYKYK.

NASA's Artemis II just released the first photo of the far side pic.twitter.com/AIa9GNUNkk

— Miss Ally (@MissAlly_01) April 7, 2026

As the kids say IYKYK.

NASA's Artemis II just released the first photo of the far side pic.twitter.com/AIa9GNUNkk

— Miss Ally (@MissAlly_01) April 7, 2026

From Iran International, April 8:

The details are still incomplete, but the positions Tehran and Washington have publicly tied to the ceasefire suggest not a shared settlement so much as a temporary halt layered over unresolved hostilities.

The precise texts are still only partly visible. The White House never publicly confirmed the full contents of the US 15-point proposal, saying only that some reporting had “elements of truth” but was “not entirely factual,” while Iranian state and semi-official media published a far more detailed public account of Tehran’s own terms.

Still, enough has emerged to show how far apart the two sides remain.

Public reporting on the US proposal described a plan centered on rolling back Iran’s nuclear and missile capabilities, curbing support for allied armed groups and reopening the Strait of Hormuz.

Iran’s 10-point plan pointed in the opposite direction. It sought recognition of enrichment, sweeping sanctions relief, compensation, continued influence over Hormuz, US military withdrawal from the region and an end to attacks on Iran and its allies.

That distinction matters because a ceasefire can stop the shooting without answering the political question of what comes next.

On the American side, the administration’s stated war aims remained consistent through March and April: destroy Iran’s missile arsenal and production capability, sever support for what Washington calls terrorist proxies, and ensure Iran never acquires a nuclear weapon.

Tehran’s public plan, by contrast, treated the ceasefire as the start of an arrangement that would preserve core elements of Iranian power rather than dismantle them.

In March, that divide was already visible. Time, citing reporting from Israeli Channel 12 and other outlets, said the US proposal called for dismantling Iran’s nuclear capabilities, ending uranium enrichment on Iranian soil, decommissioning Natanz, Isfahan and Fordow, limiting missile activity, ending support for proxy groups and keeping Hormuz open.

Iran rejected the proposal and, even before its fuller 10-point plan appeared publicly, made clear it was seeking a permanent end to the war rather than a simple pause.

You started the war, but Iran will set the conditions for its end.

— Iran in India (@Iran_in_India) April 8, 2026

Iran's 10-point conditions that the US has accepted as "workable":

The US is fundamentally committed to:

🔹 Non-aggression

🔹 Continuation of Iran's control over the Strait of Hormuz

🔹 Acceptance of enrichment…Enrichment: rollback versus recognition

No issue illustrates the contradiction more clearly than uranium enrichment.

The publicly reported US plan sought to end enrichment inside Iran and dismantle the country’s main nuclear facilities. Tehran’s published plan did the reverse.

Iranian media versions of the 10-point framework explicitly demanded acceptance of enrichment, and some outlets reported that the phrase appeared in the Farsi version even though it was omitted from some English versions shared publicly by Iranian media.

That is not a minor drafting dispute. It is a disagreement over first principles. Washington’s reported position was that Iran’s nuclear program should be rolled back at its core. Tehran’s position was that enrichment should survive in principle, with any later discussion focused on scope rather than existence.

So long as those remain the baseline positions, the ceasefire may limit violence while leaving one of the central causes of the conflict unresolved.

Allied militias: disarmament versus protection

The same gap runs through the issue of Iran’s regional allies.

The Trump administration said one of its central objectives was to sever Iran’s support for proxies. Reporting on the 15-point proposal likewise said Washington wanted Tehran to stop financing and arming those groups.

Iran’s public plan moved the other way. It called for an end to attacks not only on Iran but on its allies, and its 10-point version included a halt to war on all fronts, including Lebanon.

That contradiction was not theoretical. It surfaced almost immediately after the ceasefire announcement.

AP reported that Israel backed the US ceasefire with Iran but said it would continue operations against Hezbollah in Lebanon, directly undercutting mediation claims that Lebanon was covered....

....MUCH MORE

From The Register, April 5:

The GPU king's move to optical scale-up was inevitable

If you thought Nvidia's GB200 rack systems were big, CEO Jensen Huang is just getting started. At GTC last month, the world's most valuable company revealed plans to use photonic interconnects to pack more than a thousand GPUs into a single mammoth system by 2028.

The company isn't waiting to secure supply chains either. Over the past month, the GPU giant has invested billions in companies specializing in optics and interconnects, like Marvell, Coherent, and Lumentum, in preparation for the widespread deployment of these systems.

"For everyone who is in our ecosystem, we need a lot more capacity," Huang said during his GTC keynote speech. "We need a lot more capacity for copper; we need a lot more capacity for optics; we need a lot more capacity for CPO; and that's why we've been working with all of you to lay the foundation for this level of growth."

However, Nvidia's journey to this point began much earlier. In fact, by the time OpenAI revealed ChatGPT to the world in late 2022, Nvidia already knew it had a problem.

At the time, the GPU giant's most potent systems only featured eight GPUs, and the models driving the AI boom required thousands to train. Nvidia needed a bigger box, or at least a faster network that could effectively distribute work across dozens of chips.

We caught our first glimpse of this with Nvidia's Grace Hopper superchips in 2023, but it wasn’t until early 2024 that the full picture came into view. Unveiled at GTC that year, the Grace Blackwell NVL72, a monstrous 120 kilowatt machine, uses a copper backplane containing miles of cables to make 36 nodes and 72 GPUs behave like one enormous AI accelerator.

Copper was the natural choice for this, Gilad Shainer, senior VP of networking at Nvidia, told El Reg.

"Copper is the best connectivity, if you can use it," he said. "It's very cost effective, very cheap, and consumes zero power. It's very reliable. There are no active components."

But copper isn't perfect. At 1.8 TB/s, the cables could only stretch a few feet before the signal degraded as GPUs communicated with one another. If you ever wondered why the NVL72's NVSwitches are all in the center of the rack, it's because the runs were that short. Copper's limited reach also meant Nvidia had to cram as many GPUs into a single rack as possible.

Two years later, Nvidia is rapidly approaching the limits of copper and will need to embrace optics if it wants to assemble an even bigger GPU system.

The pluggable problem

When Huang first showed off the NVL72 rack, codenamed Oberon, the only commercially viable way to connect two accelerators optically would have been to use pluggable optics.These modules are about the size of a pack of gum and contain all the lasers, retimers, and digital signal processing required to turn electrical signals into light and back again.

Pluggables are nothing new in datacenter networks, but using them for scale-up compute fabrics, like Nvidia's NVLink, presents certain problems.

To reach the 1.8 TB/s of bandwidth, each Blackwell GPU would have required eighteen 800 Gbps pluggables: nine for the accelerator, and another nine for the switch. On their own, these pluggables don't use that much power – around 10-15 watts – but multiplied across 72 GPUs, that adds up pretty quickly.

As Huang noted in his 2024 GTC keynote speech, optics would have required an additional 20,000 watts of power.

However, a lot has changed since the Oberon rack was first revealed. Advancements in co-packaged optics (CPO), which integrates optical engines directly alongside the switch ASIC, have helped drive down power consumption.

In 2025, Nvidia became one of the first AI infrastructure providers to embrace CPO by integrating it directly into its Spectrum Ethernet and Quantum InfiniBand switches. (Broadcom-based Micas Networks was making similar moves.)

This dramatically reduced the number of pluggables required to build an AI training cluster. However, it was only more recently that the company began discussing the use of optics and CPO for its NVSwitch fabrics.

NVLink goes optical

After pooh-poohing optical interconnects as too power-hungry two years earlier, Huang revisited the topic at GTC this spring by unveiling the Vera Rubin NVL576 and Rosa Feynman NVL1152, two multi-rack systems that would use photonics to expand their compute domains by a factor of eight....

....MUCH MORE

Most recently - March 31: Photonics: "Nvidia Invests $2 Billion in Marvell, Announces Partnership" (MRVL; NVDA)

And back in the dark ages (see what I did there?):

November 6, 2015 - "NVIDIA: “Expensive and Worth It,” Says MKM Partners" (NVDA)

We don't do much individual stock stuff on the blog but this one is special.

We use it as an example of what Silicon Valley used to be, when high tech meant high technology and not a new app for some (still) mundane task.

Simply put, NVIDIA makes some of the fastest computer chips in the world.

They are used in gaming systems that require graphics that don't make you (literally) puke. Right now automakers use their chips for graphic displays.

The future: Robocars? May 2015: "Nvidia Wants to Be the Brains Of Your Autonomous Car (NVID)":

Among the fastest processors in the business are the one's originally developed for video games and known as Graphics Processing Units or GPU's. Since Nvidia released their Tesla hardware in 2008 hobbyists (and others) have used GPU's to build personal supercomputers.

Here's Nvidias Build your Own page.

Or have your tech guy build one for you.

In addition Nvidia has very fast connectors they call NVLink.

Using a hybrid combination of IBM Central Processing Units (CPU's) and Nvidia's GPU's, all hooked together with NVIDIA's NVLink, Oak Ridge National Laboratory is building what will be the world's fastest supercomputer when it debuts in 2018.

As your kid plays Grand Theft Auto....

Huh.

Iran trying to retcon "Death to America" after 47 years is actually hilarious. https://t.co/0lhlcoXFQI

— Reddit Lies (@reddit_lies) April 7, 2026

The Embassy of the Islamic Republic to South Africa is of course directly contradicting the Ayatollah-once-removed:

Ayatollah Ali Khamenei: Death To America Is Not Just A Slogan, It's Policy

Pretty snappy tagline from the old boy.

"Climateer Investing, it's not just a blog, it's a lifestyle." I should hire this guy.

Possibly related:

From VentureBeat, April 7:

Anthropic on Tuesday announced Project Glasswing, a sweeping cybersecurity initiative that pairs an unreleased frontier AI model — Claude Mythos Preview — with a coalition of twelve major technology and finance companies in an effort to find and patch software vulnerabilities across the world's most critical infrastructure before adversaries can exploit them.

The launch partners include Amazon Web Services, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorganChase, the Linux Foundation, Microsoft, Nvidia, and Palo Alto Networks. Anthropic says it has also extended access to more than 40 additional organizations that build or maintain critical software, and is committing up to $100 million in usage credits for Claude Mythos Preview across the effort, along with $4 million in direct donations to open-source security organizations.

The announcement arrives at a moment of extraordinary momentum — and extraordinary scrutiny — for the San Francisco-based AI startup. Anthropic disclosed on Sunday that its annualized revenue run rate has surpassed $30 billion, up from approximately $9 billion at the end of 2025, and the number of business customers each spending over $1 million annually now exceeds 1,000, doubling in less than two months. The company simultaneously announced a multi-gigawatt compute deal with Google and Broadcom. On the same day, Bloomberg reported that Anthropic had poached a senior Microsoft executive, Eric Boyd, to lead its infrastructure expansion.

But Glasswing is something categorically different from a revenue milestone or a compute deal. It’s Anthropic's most ambitious attempt to translate frontier AI capabilities — capabilities the company itself describes as dangerous — into a defensive advantage before those same capabilities proliferate to hostile actors.

Why Anthropic built a model it considers too dangerous to release publicly....

....MUCH MORE

From Marc Chandler at Bannockburn Global Forex:

Risk appetites have been excited by the two-week cease fire in the Middle East. Stocks and bonds have rallied strongly. The precious metals are higher. May WTI is off more than 15%. June Brent is about 13% lower. The US dollar is weaker against all the G10 and emerging market currencies that are trading. The ceasefire is overwhelming other developments including the central banks in New Zealand and India standing pat.

Global investors have responded to the news, and that may leave North American participants in an awkward position. They will be greeted with large moves and may be reluctant to substantially extend the moves without seeing further developments....

....MUCH MORE

From Agence France-Presse via the Times of Israel's liveblog, April 8:

Two ships have passed through the Strait of Hormuz since Iran agreed to reopen the waterway as part of a ceasefire deal, maritime monitor Marine Traffic says.

“The Greek-owned bulk carrier NJ Earth crossed the Strait at 08:44 UTC, while the Liberia-flagged Daytona Beach transited earlier at 06:59 UTC, shortly after departing Bandar Abbas at 05:28 UTC,” MarineTraffic says on X.

Liveblog home - https://www.timesofisrael.com/liveblog-april-08-2026/

It looks like the Islamic Revolutionary Guard Corps is running Iran but see after the jump for an interesting observation regarding the army (Artesh) vs. the IRGC.

From the Times O'London, April 6:

A diplomatic memo reveals the location of Mojtaba Khamenei. He was wounded in the same US-Israeli airstrike that killed his father

Iran’s new supreme leader, Mojtaba Khamenei, is incapacitated and receiving medical treatment in the holy city of Qom, according to an intelligence assessment which suggests he is not capable of running the country.

A diplomatic memo understood to be based on American and Israeli intelligence and shared with Gulf allies suggests that Khamenei, the son of the killed long-time leader Ali Khamenei, is unconscious and being treated for a “severe” medical condition.

The memo, seen by The Times, reveals the supreme leader’s location for the first time. The central city, 87 miles south of Tehran, is considered sacred in Shia Islam.

“Mojtaba Khamenei is being treated in Qom in a severe condition, unable to be involved in any decision making by the regime,” it reads.

Iran war latest: follow liveAccording to the memo, the elder Khamenei’s body is being prepared for burial in Qom, the seat of Shia clerical power, known as the religious capital of the country.

It states that intelligence agencies identified the preparation of “laying the groundworks needed to build a large mausoleum in Qom” for “more than one grave”, suggesting that other family members — and possibly Mojtaba himself — could be buried alongside the late supreme leader.

Information on the younger Khamenei’s location is thought to have been known by US and Israeli spy agencies for some time but has not previously been made public.

The US National Security Agency, which is responsible for processing global intelligence on behalf of the Department of War, has been contacted about the memo, as has Iran’s representation in Washington, which is based at the Pakistani embassy.....

....MUCH MORE

Though the report doesn't come out and say it, that sounds like the new supreme leader is in a coma. Which may make the following more important than it would otherwise be. It appears the Israelis have been deliberately sparing the upper ranks of the army and civilian government while killing the hard-core IRGC and Mullocracy:

Notable absence of Artesh leadership among those killed; only IRGC commanders have been targeted. https://t.co/SWZo6LmolX pic.twitter.com/QkzMWcwY67

— Colby Badhwar (@ColbyBadhwar) April 7, 2026

Meaning that should the hard-core lose their grip on power, there will be some folks left to negotiate a peace.

You always want to leave someone you can negotiate with.

Two from Singapore's Straits Times, April 8:

Trump agrees to suspend attacks on Iran for 2 weeks; Tehran says talks will begin on April 10

Follow our live coverage here.

WASHINGTON - US President Donald Trump on April 7 said he was suspending the bombing of Iran for two weeks but that Tehran must reopen the key Strait of Hormuz, barely an hour before his apocalyptic deadline to destroy the country was set to expire.

After more than five weeks of blistering attacks on Iran by the United States and Israel, Mr Trump said he had accepted a proposal mediated by Pakistan to extend his deadline but he again pushed on the Strait of Hormuz, the waterway vital for the world’s oil.

Mr Trump said he had spoken to Pakistan’s leaders who “requested that I hold off the destructive force being sent tonight to Iran”.

“And subject to the Islamic Republic of Iran agreeing to the complete, immediate and safe opening of the Strait of Hormuz, I agree to suspend the bombing and attack of Iran for a period of two weeks,” Mr Trump wrote on his Truth Social platform.

“The reason for doing so is that we have already met and exceeded all military objectives, and are very far along with a definitive agreement concerning long-term peace with Iran, and peace in the Middle East,” he added.

He said Iran had sent a 10-point plan to the US that he called “workable” for negotiations.

The Islamic republic said in a statement released alongside a list of the 10 points published by state media that the plan would require “continued Iranian control over the Strait of Hormuz, acceptance of enrichment, lifting of all primary and secondary sanctions”.Pakistan’s Prime Minister Shehbaz Sharif said the US, Iran and their allies had agreed to a ceasefire “everywhere”, including in Lebanon, following mediation by his government to stop weeks of fighting....

....MUCH MORE

And the Straits Times liveblog:

Live

- Iran says safe transit through Strait of Hormuz possible for 2 weeks ‘if attacks halted’

- Tehran says talks with US will begin on Friday in Islamabad.

- Asia stocks soar after US, Iran ceasefire announcement

....MUCH MORE

From the Federal Reserve Bank of Atlanta, April 7:

1.3%

Latest GDPNow Estimate for 2026:Q1

Updated: April 07, 2026

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2026 is 1.3 percent on April 7, down from 1.6 percent on April 2. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, the US Bureau of Labor Statistics, and the Institute for Supply Management, the nowcasts of first-quarter personal consumption expenditures growth and first-quarter real gross private domestic investment growth decreased from 1.4 percent and 6.6 percent, respectively, to 1.3 percent and 5.5 percent.

As noted exiting from the last update:

...And even more troubling, as we've observed over the years, the Atlanta Fed's model tends to run hot until it converges with the first (flash) actual GDP report.

Hmmm...

From/via ZeroHedge, April 7:

International Energy Agency (IEA) Executive Director Fatih Birol was interviewed by the French newspaper Le Figaro earlier on Tuesday and warned that the Gulf energy shock "is more severe than those of 1973, 1979, and 2022 combined" because it is affecting oil, gas, food, fertilizers, petrochemicals, helium, and global trade all at once.

Birol said in the interview that more than 75 energy sites across the Gulf region have been attacked, with about a third severely damaged, suggesting tens of billions of dollars in repairs and a prolonged disruption of some energy flows, further tightening global supplies and compounding the disruption at the Strait of Hormuz chokepoint.

The newspaper asked Birol, "How quickly can Gulf production recover?"

He responded:

"We are monitoring energy infrastructure in real time—fields, refineries, terminals. Seventy-five facilities have been attacked and damaged, more than a third severely. Repairs will take a long time. Countries like Saudi Arabia may recover faster due to strong engineering capabilities and financial resources, but elsewhere, such as Iraq, the situation is far worse. About 15 million people depend on oil and gas revenues there, and the country has lost two-thirds of its oil income, approaching economic paralysis. It will take a long time for the Middle East—previously a reliable energy hub—to recover."

Cherry-picking the most important parts of the interview:

Le Figaro asked: Who will suffer the most?

Birol responded: The global economy will suffer. Of course, European countries will struggle, as will Japan, Australia, and others. But developing countries will be the most affected due to high oil, gas, and food prices, and accelerating inflation. Their economic growth will be heavily impacted. I fear many developing countries will see their external debt rise significantly. That is why I am pessimistic—this crisis stems not from energy itself, but from geopolitics.

Le Figaro asked: Which countries are most exposed to shortages?

Birol responded: Import-dependent countries are most exposed: in Asia—South Korea, Japan, but especially Indonesia, the Philippines, Vietnam, Pakistan, and Bangladesh. African countries will also be heavily affected, as developing nations have limited financial flexibility....

....MORE

From Sherwood News, April 7:

Stocks returned to negative territory in premarket trading and oil futures jumped after Iranian state-sponsored media said that explosions were heard on Kharg Island.

The Mehr News agency, which reported this at 6:25 a.m ET, did not comment on the source of these explosions....

....MUCH MORE

And at the Associated Press:

Iran calls for human chains to protect power plants as Trump’s deadline nears

From Bloomberg, April 6:

Data center builder Firmus Technologies Pty raised $505 million in an investment round led by Coatue Management LLC, part of a global push to finance artificial intelligence infrastructure.

The deal values the Australian startup at $5.5 billion, Firmus said Monday. Nvidia Corp., the top maker of AI accelerator chips, also participated in the round.

The cash will go toward rapidly deploying AI hardware based on forthcoming Nvidia computer technology in the Asia-Pacific region. Firmus, which has data center projects in Australia and Singapore, has raised $1.35 billion in the last six months, including this latest transaction.

Firmus is leading an effort called Southgate, a plan to build data center capacity in Australia that runs on renewable energy, starting with a site in Tasmania. That facility will house computers based on 36,000 Nvidia accelerator chips after its first two rounds of technology deployments. The powerful processors help develop and run AI models by bombarding them with data.

Nvidia, often in partnership with venture capital investors, has invested billions of dollars in AI companies. It’s aiming to help cultivate an industry that has already fueled explosive sales growth and turned Nvidia into the world’s most valuable business.

As with the Firmus funding, Nvidia is backing companies that also buy its products. Some investors have expressed concern about the circular nature of these deals, something Nvidia has pushed back on.

Read More: A Guide to the Circular Deals Underpinning the AI Boom

Coatue, which has more than $70 billion in assets under management, has made its own push into AI technology. The New York-based investment firm has backed computing infrastructure as well as service providers like OpenAI and Anthropic PBC....

....MORE (sovereign AI)

If interested see also:

December 2023 - Nvidia CEO Jensen Huang Says AI to See ‘Major Second Wave (NVDA)

AI to See ‘Major Second Wave,’ NVIDIA CEO Says in Fireside Chat With iliad Group Exec

NVIDIA’s Jensen Huang says sovereign AI a growing need for countries to reflect unique cultural, linguistic, industrial characteristics

European startups will get a massive boost from a new generation of AI infrastructure, NVIDIA founder and CEO Jensen Huang said Friday in a fireside chat with iliad Group Deputy CEO Aude Durand — and it’s coming just in time.

February 2024 - "Nvidia chief sees rise of ‘sovereign AI’ infrastructure across nations, driving demand for company’s advanced chips"

This is the sort of thing we were referring to in January 20's "Advanced Micro Devices to Build 2 New Supercomputers in Germany (AMD)": "Taking a page out of Nvidia's playbook."

Nvidia wants every language to have its own large language model. And they want every country to have an Nvidia powered supercomputer (or five) to train and run the LLM on....

....Bi-lingual Canada is good but multi-lingual India is Mr. Huang's dream country.

PM Modi's people should ask for two free supercomputers upfront as part of a five 'puter order.

And side dishes. Maybe a billion dollars worth of gaming chips.

March 2024 - Here's Nvidia's "Sovereign AI" Pitch (NVDA)

*****

....This is terrible. I now have Jensen Huang speaking in Dr. Martin Luther King's cadences as he repurposes the penultimate paragraph of "I have a Dream":

Let AI ring from Stone Mountain of Georgia.

Let AI ring from Lookout Mountain of Tennessee.

Let AI ring from every hill and molehill of Mississippi.

From every mountainside, let AI ring.I may have to go lie down.

...Every, town, every village, every hamlet, every wide spot in the road, should have their own (NVDA-powered) supercomputer.

June 16, 2024

France's "Mistral AI warns of lack of data centres and training capacity in Europe"

October 4, 2024

"Parlez-vous AI? Francophone scholars warn against English language dominating AI"

....Our last couple mentions of Singtel were in reference to Nvidia's roll-out of the Blackwell chip for their sovereign AI program:

December 2024 - Canada commits $1.4B to sovereign compute infrastructure as it joins the AI arms race

January 2025 - "Jensen Huang Wants to Make AI the New World Infrastructure" (NVDA)

This sovereign AI you speak of, I have heard of it.

I have heard wondrous tales of immense wealth,

Of amazing deeds performed as if by magic.

Yes I have heard of all of this...*

And many more.

From Reuters, April 7:

- Samsung estimates 57.2 trillion won in Q1 operating profit vs 6.7 trillion won year earlier

- Analysts estimate 40.6 trillion won in Q1 operating profit

- Chipmakers struggle to keep up with demand from AI data centres

SEOUL, April 7 (Reuters) - Samsung Electronics (005930.KS), on Tuesday projected a record-high first-quarter profit, up more than eightfold from a year earlier and well above expectations as booming demand for artificial intelligence infrastructure caused supply bottlenecks and drove chip prices higher.

The world's largest memory chipmaker estimated an operating profit of 57.2 trillion won ($37.92 billion) for the January to March period, compared with an LSEG SmartEstimate of 40.6 trillion won and a more than eight-fold jump from 6.69 trillion won a year earlier.

The preliminary results nearly triple Samsung's previous record quarterly operating profit of 20 trillion won, reached in the fourth quarter last year....

....MUCH MORE

If interested see also:

January 5 - "Memory chipmakers rise as global supply shortage whets investor appetite"

January 7 - Memory: "Samsung bulls bet record earnings will extend US$350b rally" (005930:Korea)

January 12 - Chips: "While you pay through the nose for memory, Samsung expects to triple its profits in Q4"

January 28 - Memory: Samsung’s profit triples, beating estimates...

February 24 - Chips: "Samsung, SK Hynix Drive Korea Benchmark’s Breakthrough Past 6000"

February 27 - Inflation: "Smartphone market set for biggest-ever decline in 2026 on memory price surge, IDC says"

March 2 - Memory: "The inflation spark that could become a deflation shock?"

March 3 - Thanks for the Memories: "South Korea’s Kospi plunges 12% amid broader declines in Asia markets as Iran conflict rages"

The index, which has been driven by the memory chip makers, Samsung Electronics Co. and SK Hynix Inc. et al., up over 145% from March 2025 to the February 25, 2026 peak is now down 10% on the day, March 4th.

March 18 - Memory: Shortage Could Last Five Years, It's The Wafers

From the New York Times, April 3:

Artificial intelligence hasn’t disrupted the labor market, economists say, but they are increasingly convinced that it will — and that policymakers are unprepared.

Among tech evangelists in Silicon Valley, it has become conventional wisdom that artificial intelligence will rapidly reshape the labor market, for better or worse. Economists, however, have often discussed A.I.’s impact with a skepticism bordering on dismissiveness.

Rising unemployment among young college graduates? The result of high interest rates and macroeconomic uncertainty. Dire predictions of widespread job losses? A failure to understand the lessons of past technological revolutions. Even the layoffs that companies themselves blamed on artificial intelligence were often chalked up to “A.I.-washing” from executives looking for something to blame other than their own mismanagement.

Recently, however, the message from economists has undergone a subtle change. Most still do not see much evidence that A.I. is disrupting the job market. But they are starting to take seriously the possibility that it could someday soon. If it does, they are worried that policymakers are not ready to respond.

“I don’t think A.I. has hit the labor market yet, and I don’t think it’s radically changed corporate productivity yet, either, but I think it’s coming,” said Daniel Rock, a University of Pennsylvania economist who has studied the economic impact of artificial intelligence.

In a working paper published this week, a team of researchers surveyed economists about their outlook over the next five and 25 years. Most expect the economy to grow a bit more quickly as A.I. improves, but not to diverge substantially from historical patterns. If the technology improves rapidly — a possibility they consider unlikely but plausible — they envision a far more drastic scenario with faster growth but also greater inequality and the disappearance of millions of jobs.

“Economists are certainly taking A.I. seriously,” said Ezra Karger, an economist at the Federal Reserve Bank of Chicago who was one of the study’s authors.

Economists’ expectations for the future looked relatively similar to those of A.I. industry insiders, who were also surveyed for the study. Both groups agree the future is uncertain: A.I. could either wipe out whole categories of jobs or cause few job losses. Its effects could be concentrated among entry-level white-collar workers or spread to more experienced workers and those in blue-collar jobs. The changes could upend the economy within years or take decades to play out.

Given the potential scale of the disruption, economists say it is time to start considering the policies that could help workers displaced or otherwise harmed by the changing economy — something that societies often failed to accomplish in past technological transitions.

“There’s enough conversation around this that we certainly should, as a country, be talking about what sorts of policies make sense in a world where the way employment and careers work now changes a lot in the next two to five years,” said Robert Seamans, an economist at New York University.

A Paradigm Shift

When OpenAI released ChatGPT to the public in November 2022, Alex Imas, an economist at the University of Chicago, did not necessarily see it as an economic game changer, he said. The technology was powerful but limited, prone to mistakes and incapable of producing work with the quality and consistency necessary for most professional applications.“I knew it was important, but I was definitely on the more skeptical side when it first came out,” Mr. Imas recalled.

For Mr. Imas, the real shift came in late 2024, when OpenAI released a model capable of “reasoning,” meaning it could work through a question step by step before producing an answer. That ability greatly expanded the type of problems the model could tackle, and made it more reliable at solving them.

“It was just a paradigm shift for me,” Mr. Imas said. “And then I started thinking, ‘This is potentially an industrial revolution-scale event, if not more.’”

For other economists, the shift came just in the past few months, with the release of Claude Code — a tool from the A.I. company Anthropic that writes computer code from users’ prompts — and the widespread rollout of A.I. “agents,” autonomous systems capable of performing tasks directly.

Molly Kinder, a senior fellow at the Brookings Institution who studies A.I., said that as she experimented with the new tools, she had a realization: She no longer needed anyone to do the kind of basic research that she ordinarily hired college students and recent graduates to perform — and that she had performed herself early in her career.

“I really don’t know anything a college student can bring to my team that Claude can’t do,” she said. More senior jobs — ones that require interacting with clients and investors, or making strategic decisions — may be safe for now, she said. But “if you can do your job locked in a closet with a computer, ultimately you’re going to be in trouble.”

Everywhere but the Statistics

Technological advancement alone will not reshape the economy. For that to happen, companies need to adopt the tools and figure out how to use them productively.History shows that the process almost always takes longer than the inventors expect. Legal and regulatory hurdles slow things down. Companies have to retrain workers or hire new ones. Corporate leaders have to develop new processes and overcome resistance from reluctant managers and cautious information technology departments.

“These conversations have been, in my opinion, overly focused on what the technology can do,” said Martha Gimbel, the executive director of the Budget Lab at Yale University. “There’s plenty of technology that could have changed things and didn’t.”

Many hospitals kept patients’ health records on paper for decades after the technology existed to digitize them, Ms. Gimbel noted. Videoconferencing tools have existed for years, but it took a pandemic to force companies to embrace them.

There are signs that A.I. could flow through the economy more quickly than past innovations. Already, nearly one in five companies reports having used A.I. in the last two weeks, according to data from the Census Bureau, and in some industries the rate is twice as high. Workers report using A.I. at even higher rates, suggesting many may be experimenting with the tools on their own initiative.

And while A.I. has not yet had a big impact on aggregate statistics, some economists argue its effects are visible beneath the surface. In a paper published last year, researchers at Stanford University found that employment was declining for entry-level workers in jobs that were highly exposed to A.I.

Technological advancements “sometimes take decades” to appear in the economy in the form of increased productivity, said Erik Brynjolfsson, one of the authors of the Stanford paper. “I don’t think it’s going to be decades this time.”

‘How Painful Is It Going to Be?’....

....MUCH MORE

Earlier today at Yahoo Finance:

Goldman Sachs' blunt warning to laid-off tech workers: It will take time and earnings loss to find a new job

From Bloomberg, April 1:

The struggle to manufacture transformers, switchgear and batteries domestically has forced the US to rely on imports, delaying data center construction.

In the red dirt of Abilene, Texas, more than 6,000 workers travel around on electric buggies, spending day and night constructing a massive data center that will feed the world’s growing artificial intelligence needs. When completed this year, the eight sprawling buildings — which OpenAI will use — will consume 1.2 gigawatts of power, or enough electricity for nearly 1 million American households.

As the global AI race heats up, there is a huge rush to build data centers fast. There’s no lack of money chasing these projects, with tech giants Alphabet Inc., Amazon.com, Meta Platforms Inc. and Microsoft Corp. committed to spending more than $650 billion this year alone. Yet neither ambition nor capital is enough to materialize all the necessary components for these power-hungry computers.

Almost half of the US data centers planned for this year are expected to be delayed or canceled. One big reason is the shortage of electrical equipment, such as transformers, switchgear and batteries. They are needed not just for powering AI, but also for building out the grid that is seeing increased consumption from electric cars and heat pumps. US manufacturing capacity for these devices cannot keep up with demand, and the scarcity has caused data center builders to rely on imports.

Electrification is a key solution to both tackling climate change and powering AI ambitions. But America’s AI prowess on computer chips and cutting-edge software is being hamstrung by the country’s inability to manufacture the electrical parts. “There’s not enough domestic capacity to go around, so people are pretty much forced to go to the export market,” says Benjamin Boucher, senior analyst with Wood Mackenzie.

The import dependence is putting data center companies in a bind. “There’s only going to be one winner,” President Donald Trump said in December, “and that’s probably going to be the US or China.” While he wants the US to win, his America First doctrine calls for installing trade barriers to cut imports.

Data centers consuming as much as 12 gigawatts of power are supposed to come online in 2026 in the US, according to analysts at market intelligence firm Sightline Climate, who will be releasing a new report in the coming weeks. However, only a third of that is currently under construction, Sightline estimates.

Crusoe won the contract to build the Texas data center campus because of its promise of speed. Cully Cavness, Crusoe’s chief strategy officer and co-founder, says the company pledged to get a portion of the data center powered up in less than a year after starting construction. The secret to achieving that was buying enough of the right electrical equipment through early orders, securing some supplies before export barriers were erected.

Electrical infrastructure adds up to less than 10% of the total cost of the data center, but it’s impossible to build the operation without it. “If one piece of your supply chain is delayed, then your whole project can’t deliver,” says Andrew Likens, Crusoe’s energy and infrastructure lead. “It is a pretty wild puzzle at the moment.”

Most companies contacted by Bloomberg News declined to comment on the problems they are facing or where they source their equipment from. The few that responded highlighted the solutions they have enacted. Spokespeople for Amazon and Microsoft said they plan electrical equipment procurement ahead of time when building their data centers, and a spokesperson for Equinix Inc. pointed to a recent investment in a manufacturing facility that makes switchgear. Google, Oracle, Nebius Group NV, and Coreweave Inc. declined requests to comment....

....MUCH MORE

Recently:Following on April 5's "Inside China’s robotics revolution".

We have no interest in IPOs as vehicles to invest/speculate/gamble with, but do pore over offering documents to glean whatever insight might be publicly proffered.

From Irene Zhang at ChinaTalk substack, April 2:

Unitree Goes Public

robotics diffusion, AGI for the real world, and US-China entanglement

In 2017, Hangzhou-based robotics firm Unitree 宇树科技 launched its first quadruped, Laikago. Laika was the name of the Soviet space dog onboard Sputnik 2, and the American English pronunciation of “go” is similar to that of the Chinese word for dogs, 狗 gǒu. Unitree’s battery-powered tribute to Laika wasn’t fuzzy, but walked on four feet and navigated through basic obstacles.

Unitree founder Wang Xingxing 王兴兴 has long held faith in the potential of robotic canines. Since 2020, when Unitree started gaining media attention, he has insisted in multiple interviews that humans are drawn to four-legged creatures and will have a natural fondness for their artificial counterparts.

Fast forward to 2026, and Unitree has just filed for a $610-million IPO on the Shanghai Stock Exchange. The company is a household name in China after its humanoid robots performed dances at the CCTV Spring Festival Gala for two consecutive years and counting. Through their IPO disclosures (investor prospectus and response letter to the Shanghai Stock Exchange’s inquiries), we get some answers to important questions about the development of embodied AI.

How is Unitree profitable?

Where is diffusion happening inside China, aside from dancing on TV?

Are Chinese robotics companies content to lead in hardware and applications, or do they also see themselves as pursuing some kind of generalized “frontier”?

And finally, what does this all mean for US-China dynamics in robotics?

***video***

What’s the money maker?

One of the most notable things about Unitree is the fact that it actually makes money. Unprofitability is a near-universal challenge because AI robotics, despite massive advances in the past few years, is still an early-stage technology. Mass adoption has not yet arrived; pathways out of bottlenecks like data are uncertain; and important safety standards have not caught up. Even shipping products consistently can be a challenge for some companies in the space, let alone manufacturing at scale and booking reliable customers.This context is why observers have found Unitree’s ability to turn a profit remarkable. Not only has the company’s net profit been positive since 2024, but from 2024 to 2025, its net profit grew by 204.29%. A look at its growth, broken down by product category, reveals the most significant source of this revenue explosion: humanoids.

....MUCH MORE

Previously:

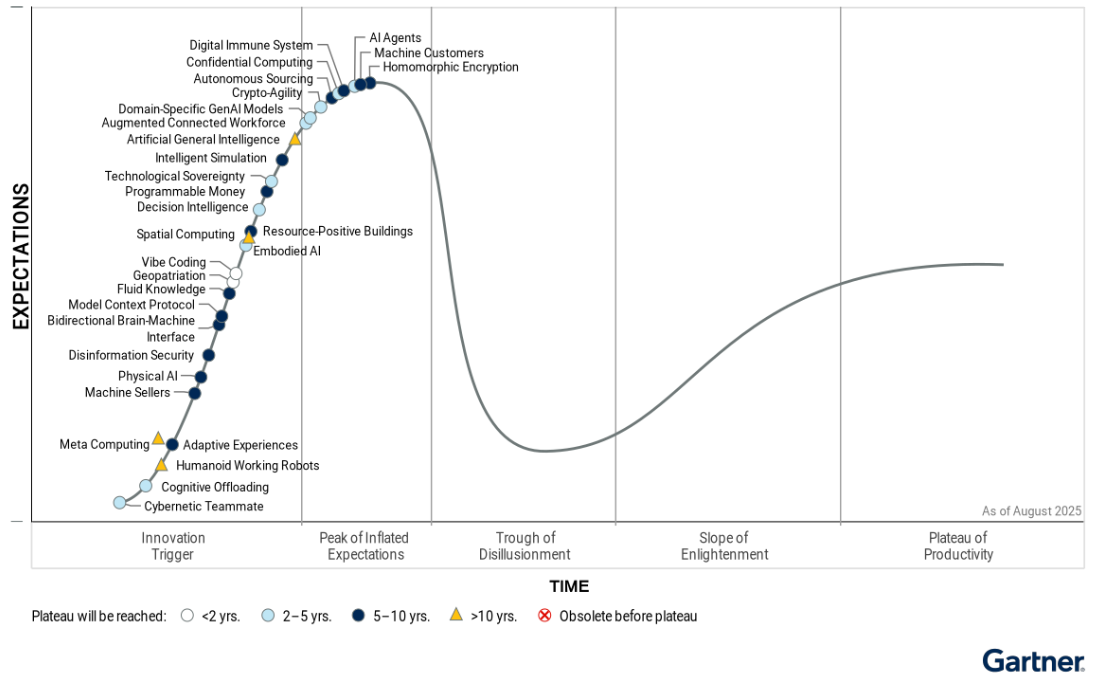

January 29, 2026 - "Gartner Predicts Fewer Than 20 Companies Will Scale Humanoid Robots for Manufacturing and Supply Chain to Production Stage by 2028"

So it looks like 2027 will be a very important year for Unitree, Tesla and the other 90 wannabe players. We shall see.

Here's Gartner's Hype Cycle for emerging technologies. Humanoids are bottom left and tagged by Gartner with an expected ten years to the Plateau of Productivity:

Of course that also implies we are quite a ways from the Trough of Disillusionment as well.

And of course, your mileage may vary:

September 13, 2022 - Gartner Outlines Six Trends Driving Near-Term Adoption of Metaverse Technologies

There are many, many more. If interested use the search blog box, upper left.From Quanta, March 16:

The central limit theorem started as a bar trick for 18th-century gamblers. Now scientists rely on it every day.

No matter where you look, a bell curve is close by.

Place a measuring cup in your backyard every time it rains and note the height of the water when it stops: Your data will conform to a bell curve. Record 100 people’s guesses at the number of jelly beans in a jar, and they’ll follow a bell curve. Measure enough women’s heights, men’s weights, SAT scores, marathon times — you’ll always get the same smooth, rounded hump that tapers at the edges.

Why does the bell curve pop up in so many datasets?

The answer boils down to the central limit theorem, a mathematical truth so powerful that it often strikes newcomers as impossible, like a magic trick of nature. “The central limit theorem is pretty amazing because it is so unintuitive and surprising,” said Daniela Witten (opens a new tab), a biostatistician at the University of Washington. Through it, the most random, unimaginable chaos can lead to striking predictability.

It’s now a pillar on which much of modern empirical science rests. Almost every time a scientist uses measurements to infer something about the world, the central limit theorem is buried somewhere in the methods. Without it, it would be hard for science to say anything, with any confidence, about anything.

“I don’t think the field of statistics would exist without the central limit theorem,” said Larry Wasserman (opens a new tab), a statistician at Carnegie Mellon University. “It’s everything.”

Purity From Vice

Perhaps it shouldn’t come as a surprise that the push to find regularity in randomness came from the study of gambling.

In the coffeehouses of early-18th-century London, Abraham de Moivre’s mathematical talents were obvious. Many of his contemporaries, including Isaac Newton and Edmond Halley, recognized his brilliance. De Moivre was a fellow of the Royal Society, but he was also a refugee, a Frenchman who had fled his home country as a young man in the face of anti-Protestant persecution. As a foreigner, he couldn’t secure the kind of steady academic post that would befit his talent. So to help pay his bills, he became a consultant to gamblers who sought a mathematical edge.

Flipping a coin, rolling a die, and drawing a card from a deck are random actions, with every outcome equally likely. What de Moivre realized is that when you combine many random actions, the result follows a reliable pattern.

Flip a coin 100 times and count how often it comes up heads. It’ll be somewhere around 50, but not very precisely. Play this game 10 times, and you may get 10 different counts.

Now imagine playing the game 1 million times. The bulk of the outcomes will be close to 50. You’ll almost never get under 10 heads or over 90. If you make a graph of how many times you see each number between zero and 100, you’ll see that classic bell shape, with 50 at the center. The more times you play the game, the smoother and clearer the bell will become.

De Moivre figured out the exact shape of this bell, which came to be called the normal distribution. It told him, without his having to actually play the game, how likely different outcomes were. For instance, the probability of getting between 45 and 55 heads is about 68%.

De Moivre marveled with religious devotion at the “steadfast order of the universe” that eventually overcame any and all deviations from the bell. “In process of time,” he wrote, “these irregularities will bear no proportion to the recurrency of that order which naturally results from original design.”

He used these insights to sustain a meager life in London, writing a book called The Doctrine of Chances that became a gambler’s bible, and holding informal office hours at the famed Old Slaughter’s Coffee House. But even de Moivre didn’t realize the full scope of his discovery. Only when Pierre-Simon Laplace ran with the idea in 1810, decades after de Moivre’s death, was its full reach uncovered.

Let’s take an example slightly more complex than coin flips: dice rolls. Every roll of a die has six equally likely outcomes. If you repeatedly roll the die and tally the results, you’ll get a chart that looks flat — you’re bound to see about as many rolls of 1 as you do 2 or 4 or 6....

....MUCH MORE

Bunch of lightweights.

Back in the day the old-timers didn't need much more in the toolbox than a rock and a stick.

Some months they didn't even use the rock for weeks at a stretch.

From Bloomberg, March 19:

As Maxence Visseau spent the first few days of the Iran war trying to make sense of what the conflict would mean for markets, he put artificial intelligence at the heart of his investment process.

Large-language models enabled Visseau, the founder of investment firm Arkevium, to cut the time he spent on research by about 80%. He used Anthropic’s Claude to stress-test multiple scenarios in parallel, compare historical precedents and map out potential ripple effects across asset classes.

“I was up for almost 48 hours straight, monitoring the interceptions in the United Arab Emirates while simultaneously running scenarios and preparing for the market open,” said Visseau, who’s based in Dubai and specializes in macro trading strategies. “That’s precisely the kind of moment where AI becomes indispensable.”

While Visseau said the technology isn’t a reliable substitute for human judgment, he views the time-saving benefits of AI as increasingly essential for navigating markets whipsawed by a war that has upended energy supplies and left at least 4,000 dead. Interviews with investors and strategists across the globe suggest the conflict has led AI tools to become more entrenched in workflows, even as several flagged pitfalls including sloppy prompts and inaccurate results.

“We are witnessing history — the first major conflict where AI is being used to fight and where traders rely on AI to map out the war in ways that have never been done before,” said Nick Twidale, chief market analyst at AT Global Markets in Sydney and who’s a 25-year veteran of trading markets.

One of the advantages of using AI tools such as OpenAI’s ChatGPT, Google’s Gemini and China’s DeepSeek is a dramatic improvement in time management.

Jian Shi Cortesi says where she previously may have spent half an hour reading different sources to catch up on the news, now the Zurich-based fund manager at GAM Investment Management can get a summary of the latest developments in the war in seconds. Gathering information about a particular company takes a day or less, down from multiple days previously.

“In the past, it’s like digging a hole with a shovel. Now you’re digging dirt with these massive excavators,” Cortesi said. “The speed has probably increased by five times.”

Another is being able to mine history near instantaneously for insights and context on what may happen next, especially given the volatility in markets. Brent crude surged as much as 11% to top $119 a barrel on Thursday on concern over the risk of escalating tit-for-tat attacks on key energy facilities in the Middle East, before giving up most of its gains. It last traded at $108.

Deep Search

Anna Wu, a cross asset strategist at Van Eck Associates Corp. in Sydney, used ChatGPT and Claude to go back 100 years to track every war-driven oil breakout, and find out what asset classes outperformed in each occurrence. To improve the utility of the answers, she asked AI to cross reference with other data points such as the median inflation and global economic growth.

“It definitely has brought in more efficiency,” Wu said. “A lot of the historical analysis right now has become a lot less time-consuming because before it would be me searching to the end of Google.”

For Gustavo Pessoa, artificial intelligence tools provide instant access to information that previously might have been hard to get, at a time when calculating the impact of the virtual closure of the Strait of Hormuz is becoming more essential to investing.

“We use it for everything — from understanding the types of ships to analyzing the elasticity of oil demand to prices and even estimating how many barrels will be needed to stabilize flows,” said Pessoa, who’s a founding partner at Sao Paulo–based hedge fund Legacy Capital Gestora de Recursos Ltda.

AI is not perfect, nor is it a replacement for human experience and decision-making. The technology has made mistakes in everything from gaming development to news content representation. A Bank of England policymaker warned that AI adoption in trading may amplify market shocks and herd-like behavior....

....MUCH MORE

From Marc to Market:

The US deadline on Tehran for re-opening the Strait of Hormuz has subtly shifted until tomorrow. The holiday-thinned market initially bought dollars and oil and took risk off in response to the continued attacks and the escalation of US rhetoric. However, negotiations, apparently led by Pakistan, Egypt, and Türkiye for a 45-day cease fire, have captured the imagination of market participants, even though the negotiators themselves do not appear optimistic.

In quiet turnover, the dollar has given up its early gains, and as the North American session is about. to begin, the greenback is lower against all the G10 currencies and emerging market currencies. US index futures are trading firmer and May WTI is off around 1% but is still near $110. It still seems binary. If the hopes are dashed, risk will come off as the conflict could dramatically escalate....

....MUCH MORE

From Mr. Gates' GatesNotes blog, March 23:

I’m in Texas this week to talk about the remarkable breakthroughs fueling our zero-emission future.

Greetings from the Lone Star State! I’m in Texas this week for the Breakthrough Energy Ventures Investors Summit. This is one of the best places in the world to see the future of energy, and I can’t wait to see how much progress has been made since my last visit.

There’s a lot on the agenda this week, but I’m especially excited to talk about electricity breakthroughs. By 2050, the world will need nearly three times as much power as we use today—and if we’re going to decarbonize the economy, we’ll have to electrify a lot of things that currently use fossil fuels. That means we need to deliver a huge amount of energy in a clean, reliable, and affordable way.

If you’re an electricity nerd like me, this is an exciting moment. Earlier this month, TerraPower—the next-generation nuclear power company I created in 2008—received federal approval to start building the nuclear reactor at its Kemmerer, Wyoming plant. Wind and solar are reportedly generating more electricity than fossil fuels in the EU for the first time. We’re seeing a clear shift as the world’s electricity system is becoming more diverse, more innovative, and more dynamic than ever before.

Here are three of the coolest technologies people will be talking about this week:

Geothermal. Geothermal power has been around for more than a century, but new approaches are unlocking greater potential for the technology. Most geothermal power plants today are located near the boundary between two tectonic plates, where you don’t have to drill as deep to find usable heat that can be pumped to the surface to turn a turbine and generate electricity.

Fervo wants to make geothermal an option in more places by both digging deeper (up to a mind-blowing 15,000 ft below the surface) and extending their wells horizontally at their deepest point. The results so far are super promising: Their pilot project has been consistently generating electricity since 2023, and their Cape Station plant in Utah will come online this year.

Fusion. Fusion is the reaction that powers the sun and stars, and it has the potential to be a virtually unlimited source of clean, safe electricity. Once the technology is fully commercialized within the next decade, it can be built anywhere, scaled up, and used to make huge amounts of electricity with no carbon emissions and minimal waste.

The question right now is how we get there. It seems likely that the first commercial fusion plants will use magnetic fields to harness the reaction to generate electricity. There are two different approaches to this: the tokamak, a donut-shaped machine that is easier to build but harder to keep stable, and the stellarator, a twist-shaped machine that is harder to build but easier to keep stable. (An unstable reaction can damage the machine but poses no risk to safety.) Commonwealth Fusion Systems is on track to turn on their SPARC tokamak next year, and Type One Energy is making great progress with their Infinity One stellarator. Marathon Fusion, Xcimer, and Zap Energy aren’t quite as far along with their approaches, but I’m optimistic about what they’re doing.

Geologic hydrogen. Hydrogen shows great promise as an energy source, and the discovery of geologic hydrogen is one of the biggest energy surprises of the past decade. Although it’s the earliest stage technology on this list, I’m excited about its potential. Geologic hydrogen is a zero-emission power source that is continuously generated underground by the Earth itself. Bourakébougou, a village in Mali, is powered by the small hydrogen field it sits on top of, and researchers have found deposits in the U.S., France, and other places.

This is an unusual technology to talk about because it’s hard to predict a timeline....

....MUCH MORE including video.

We have dozens, nay, scores of posts on Mr. Gates and energy and Breakthrough Energy Ventures. On Breakthrough and its billionaire backers;

https://climateerinvest.blogspot.com/search?q=breakthrough+energy+ventures

And on Bill and nuclear:

Bill Gates Goes To Wyoming Coal Country, Breaks Ground On A Nuke Plant, Plays Poker With The Locals

On geologic hydrogen:

Want To Be A Hydrogen Tycoon? Maybe Prospect For Ophiolite And Chromite Ore

"There's hydrogen in them thar hills"

Grizzled prospector intently looking for hydrogen.

just kidding, that's Tom Waits in the Coen brothers film “The Ballad of Buster Scruggs.”

On the tribulations of dealing with stuff vs. dealing with software. May 2019:

Bezos, Andreessen and Gates Looking For Cobalt In Canada

Not them personally, can you imagine? Tramping around northern Saskatchewan?

Jeff: Bill, does this rock look blue to you?No, it's a company they're invested in....

Bill: I can't see it, let me get my glasses.

Marc: Guys, have I told you all the things I've wanted to tweet since I quit Twitter?

Jeff and Bill: Oh Gawd