Geez I hope not.

From Neue Zürcher Zeitung's TheMarket.ch, December 13:

Market strategist and historian Russell Napier outlines a future in which governments mandate where investors should deploy their capital. The global monetary system that has existed since 1994 is being radically restructured.

When Russell Napier speaks, investors around the world listen closely. The long-standing market strategist – formerly with the Hong Kong brokerage CLSA – and author of the Solid Ground Report was one of the earliest warning voices of an impending wave of inflation in the summer of 2020. When The Market NZZ spoke with him two years ago, he predicted a boom in global capital investment.

Napier remains convinced that the global financial system is in the process of fundamental change. «We are talking about nothing less than a collapse of the global monetary system as we have known it for the last three decades», he says.

In an in-depth conversation with The Market NZZ, which has been lightly edited for clarity, Napier explains what this means and how investors should prepare for it.

When we last spoke, you said that governments had found the magic money tree: That by guaranteeing bank loans, they could create money at will, paving the way to financial repression and inflating away their debt. Is that still your view?

In the long term, yes. Financial repression and inflating away bloated debt levels will be with us for years, even decades. But I think we’re experiencing a hiatus first. Governments did exactly what I said in 2021. They created money on a massive scale. Their actions, quite predictably, led to inflation. But then they panicked. So they handed the ball back to the central bankers and said do something about this. In my opinion, central banks have done too much, they hit the brakes too hard. Hence my fear that we might be facing a deflation shock in the short term.

You’re saying central banks have tightened too much?

Yes. We’ve seen a collapse in the growth of broad money in a magnitude that we hadn’t seen since the 1930s. Now, you might say this doesn’t matter since so much broad money was created between 2020 to 2022, and clearly it hasn’t mattered for the past two years. But now it’s starting to bite. That’s my evidence that they have overtightened.

Both in the US and in Europe, M2 growth has picked up again. Central banks have started cutting rates. Why do you still fear a deflation shock?

You’re right, M2 growth has picked up a bit, but it is growing too slowly. It would need to accelerate. The level of M2 growth in relation to the current level of interest rates is just not compatible with what would be needed to sustain economic growth.

Inflation, especially in the US, shows signs of stickiness. Don’t you think another inflationary wave might be in the making?

I can’t reconcile that with the growth rate of broad money. Sure, if we were to suffer a supply shock, then inflation would go up, regardless of what broad money does. But absent that, if broad money is not going up, it suggests that economic activity is going to weaken. I always look at things through a monetary prism. In my view, the next shock is more likely to be deflationary.

Where could that shock come from?

You and I could hypothesise about that all day. It could be a spike in French bond yields. It could be China floating its exchange rate, which would cause the yuan to devalue. It could be the yen carry trade unraveling again. And there’s a fourth possibility, which is the unknown unknown. Somebody somewhere gets into trouble, and we’ll see something break in the financial system.

So basically you are saying that we first might experience a deflation shock before we go back to a world of higher inflation?

Yes, my longer term view of financial repression remains unchanged. That’s the only way I see that will lead us out of the record high levels of debt. Mind you, I use the term deflation shock, but I’m not sure we’ll see outright deflation. Deflation shocks are bad for the economy, they are ugly for equities, and they are very dangerous for high levels of debt. You don’t make money as an investor by trying to predict deflation shocks, you make money by anticipating the government reaction to deflation shocks. And I am convinced that governments will react swiftly by forcing banks to lend, by suppressing interest rates and by using national savings to invest in things they want.

What are the signs that tell you this is happening?

On April 26th, President Emmanuel Macron of France held a speech at the Sorbonne, titled «Europe – It Can Die». Read it. It’s a sea change. In a telling bit of his speech, Macron says that every year, Europeans send 300 billion euros to the US to fund the American government and American corporations. In other words, he's outlining a concept of national savings, and they should be used for the national good. Mario Draghi in his report to the EU Commission also outlines all the things that should be done with new money. The British, meanwhile, are talking about mandation, which posits that pension funds in Britain must invest a certain percentage of their funds domestically. That’s what lies ahead. Governments will tell investors how and where to invest their capital.

And that would conform to your definition of financial repression?

Yes. I say we are headed towards a system of national capitalism. Interestingly, the term ‹national capitalism› has been used before, by a man who used to live in Zurich for a while: his name was Lenin. In a system of national capitalism, governments direct national savings towards national purposes. And our purposes today are investments, as outlined by Macron or Draghi and also by industrial policy initiatives in the US: Investments in energy infrastructure, in defense, in new productive capacity in order to de-risk from China. If we get into a bad Cold War with China, this will have a high national priority.

Do you expect a continuation of the boom in capital expenditures that you outlined two years ago?....

....MUCH MORE

Our most recent visit with Mr. Napier was November 22's Russell Napier: "America, China, and the Death of the International Monetary Non-System" from American Affairs Journal.

We've referenced his capex/construction/infrastructure interview a couple times, here's

Russell Napier Called It: "The Eyepopping Factory Construction Boom in the US"

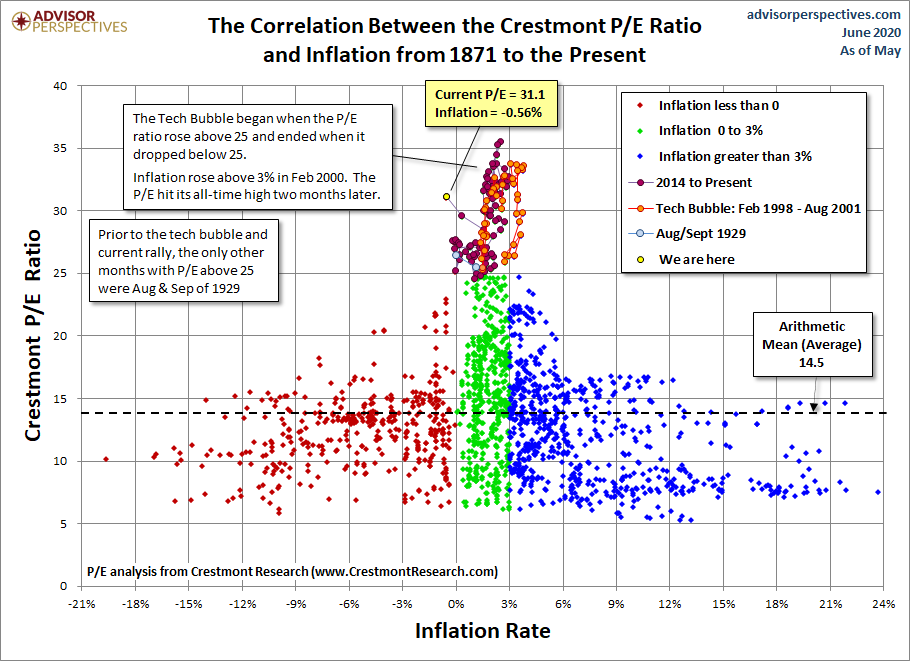

And a reminder from Crestmont Research that inflation is historically (USA, last 100 years) kindest to equity valuations (P/E) at 0% to 4% with 1% to 2% being the the sweet-spot. The sweet spot used to be higher if well enough understood to take advantage of what was transpiring. Back in the day Papiermarks and purchase real assets: plant, property and equipment, that held its value during the WWI inflation and the Weimar hyperinflation. For a while he became the richest person in the world.

That trade seems to have disappeared with the current economy's skew toward asset-light businesses.

Here's Crestmont:

The Relationships Between Inflation Rates, P/E Multiples, and Expected Future Returns

....Here's another way to look at the relationship between inflation and P/E's. Note that both the highest inflation and deflation rates correspond with the lowest multiples accorded the earnings:.

And a different way to look at the information: