Stanley Fischer, Central Banker, MIT Econ. Mafioso, Has Died

From the New York Times, June 1:

Stanley Fischer, Who Helped Defuse Financial Crises, Dies at 81 He was the No. 2 at the Federal Reserve and the I.M.F. during periods of economic turmoil, and he mentored future economic leaders, like Ben Bernanke.

Stanley Fischer,

an economist and central banker whose scholarship and genial,

consensus-seeking style helped guide global economic policies and defuse

financial crises for decades, died on Saturday at his home in

Lexington, Mass. He was 81.

The cause was complications of Alzheimer’s disease, his son Michael said.

Mr.

Fischer served as the head of Israel’s central bank from 2005 to 2013,

as vice chairman of the Federal Reserve Board from 2014 to 2017 and as

the No. 2 officer at the International Monetary Fund from 1994 to 2001,

when that agency was struggling to contain financial panics in Mexico,

Russia, Asia and Latin America.

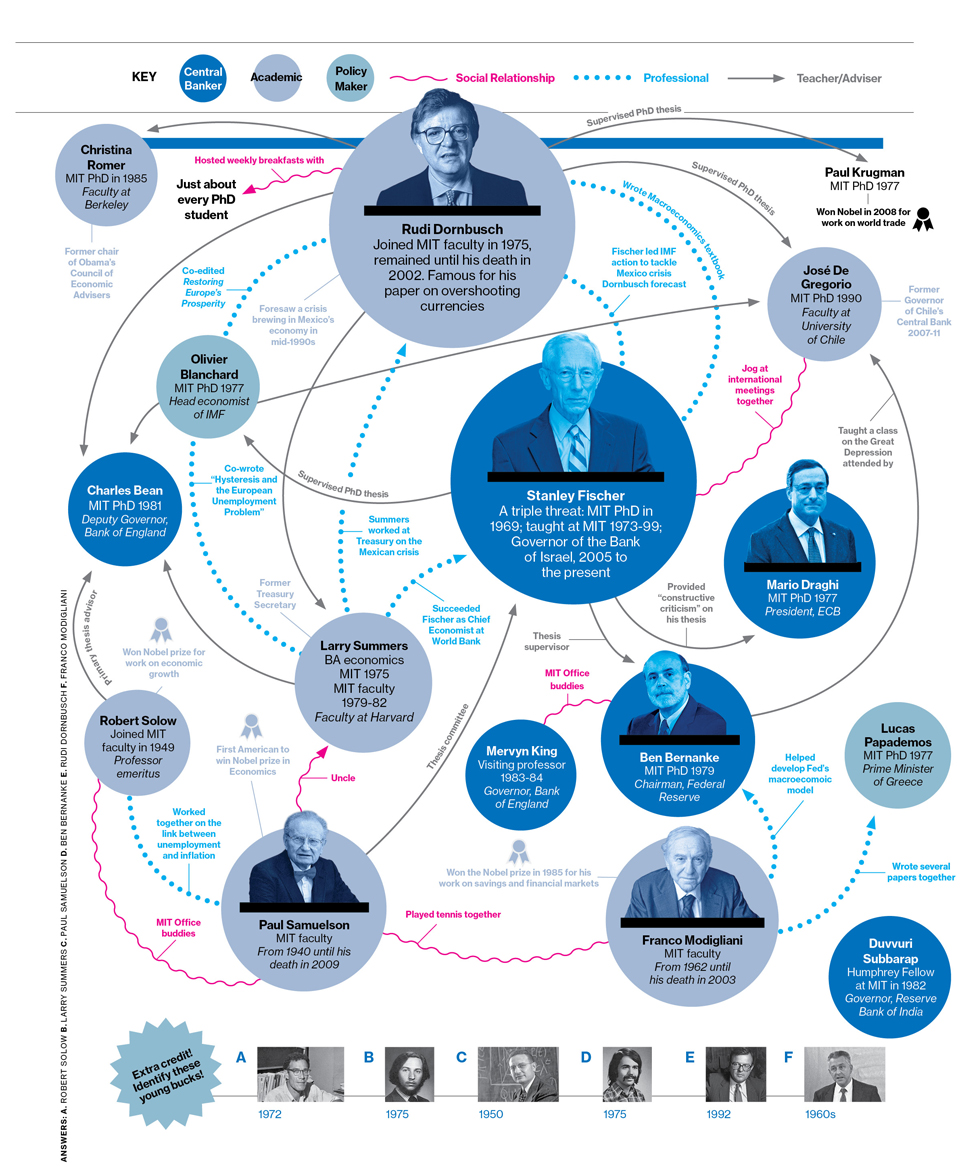

As a

professor at M.I.T., he was a thesis adviser or mentor to an

extraordinary range of future leaders, including Ben S. Bernanke, later

chairman of the Fed; Mario Draghi, president of the European Central

Bank; and Kazuo Ueda, governor of the Bank of Japan.

His

former students also included two people who chaired the U.S. Council

of Economic Advisers, Christina D. Romer and N. Gregory Mankiw, as well

as Lawrence H. Summers, who served as secretary of the Treasury and

president of Harvard University.

“He had a role in

shaping a whole generation of economists and policymakers,” Mr.

Bernanke said in a February 2024 interview for this obituary. That

included spurring Mr. Bernanke’s initial interest in macroeconomics and

monetary policy.

In 1998, The Times

described Mr. Fischer as “the closest thing the world economy has to a

battlefield medic.” He helped negotiate a rescue package for Russia by

cellphone while standing atop a sand dune on Martha’s Vineyard, where he

was on vacation.

The cures Mr. Fischer prescribed for financial crises were broadly in line with the Washington Consensus, aset of “best practices” compiled in 1989 by John Williamson, a British economist.

Those

guidelines called for openness to free markets, global trade and

foreign investment, among other things. Joseph E. Stiglitz, a Nobel

Prize-winning economist and Columbia University professor, accused the

I.M.F. of acting like a “colonial ruler” and in a 2002 interview with

The Times said that the fund and the World Bank were trying to impose

standard approaches that didn’t take full account of differing

conditions in each country.

In a 2003 lecture on globalization, Mr. Fischer generally defended the

I.M.F.’s approach by arguing that opening up to foreign trade and

investment had lifted multitudes out of poverty in China and India.

Mr. Fischer was a leader in updating the theories of the British

economist John Maynard Keynes, whose calls for government intervention

to steer the economy resonated from the 1930s through the 1960s but came

under harsh attack in the 1970s. At that time of high inflation and low

economic growth, a combination known as stagflation, economists at the

University of Chicago and elsewhere argued that government intervention

was likely to be self-defeating.

Mr. Fischer’s research in the 1970s

focused on that split between Keynesian economists and the Chicago

school’s faith in the market. If unemployment was too high, the

Keynesians argued, central banks could stimulate the economy by making

the money supply grow faster. The Chicago-school economists countered

that such stimulus would prompt workers to expect higher inflation and

demand pay increases; the result would be faster inflation and no

sustainable rise in employment.

In a

1977 paper, “Long-Term Contracts, Rational Expectations, and the Optimal

Money Supply Rule,” Mr. Fischer argued that wages were “sticky” because

of long-term contracts and didn’t adjust immediately when a central

bank changed its policy. Thus, he wrote, a well-timed stimulus program

could boost job creation in the near term without igniting inflation.

“There is some room for maneuver by the monetary authorities” in steering the economy, he concluded.

His

work in this area helped shape a broad agreement among

intervention-minded economists under the label of New Keynesian

economics.

Mr. Fischer also

was chief economist of the World Bank in the late 1980s and vice

chairman of Citigroup in the early 2000s. He failed in a long-shot bid

to become the head of the I.M.F. in 2011, losing out to Christine

Lagarde of France, partly because he exceeded the age limit for the job.

At the time, he argued that he was “full of vigor” at67 and should be given an exemption from the ceiling of 65.

Mr.

Fischer was influential partly because of his diplomatic nature,

Olivier Blanchard, one of his former students and later a colleague at

M.I.T., wrote in 2023.

Even when the field of macroeconomics “was going through wars of

religion, there was no sense of ‘us versus them’ but instead an openness

to alternative views,” Mr. Blanchard wrote.

After

he took a break from academia in the late 1980s to work at the World

Bank, Mr. Fischer was hooked on what he sometimes called his “real

world” role. He relished international travel and the fast-paced demands

of finding solutions for economic crises affecting billions of lives....

Ben Bernanke, Mario Draghi, Kazuo Ueda, Christina Romer, N. Gregory Mankiw, and Lawrence Summers. Also IMF chief economists Olivier

Blanchard, Ken Rogoff and Maurice Obstfeld.