It is probably time to retire what has been a very trusty lodestone, February 9's "Prepare for a Springtime CPI Collapse".

From Wolf Street, May 30:

Outside of two heroes that pushed down the overall indices, there isn’t anything benign about this PCE inflation data.

The PCE price index, released today by the Bureau of Economic Analysis, was benign. The overall PCE price index and the core PCE price index barely ticked up on a month-to-month basis, and on a year-over-year basis decelerated further toward the Fed’s 2% target. And that’s nice. But why? And the answer is not nice.

Two very unusual things happened – one has never to that extent happened before in the data going back to 1960, and the other hasn’t happened to that extent since the market crash in 2020 – which pushed down the core services PCE price index, the core PCE price index, and the overall PCE price index.

What’s not nice is that we know that those two components will snap back violently.

The PCE (Personal Consumption Expenditure) price index tracks not only goods and services that are included in the CPI (Consumer Price Index), but also other categories that consumers don’t pay for directly, such as many financial services, and it tracks many of the components not by observing transaction prices, but by “imputing” price levels from other data, including from financial markets.

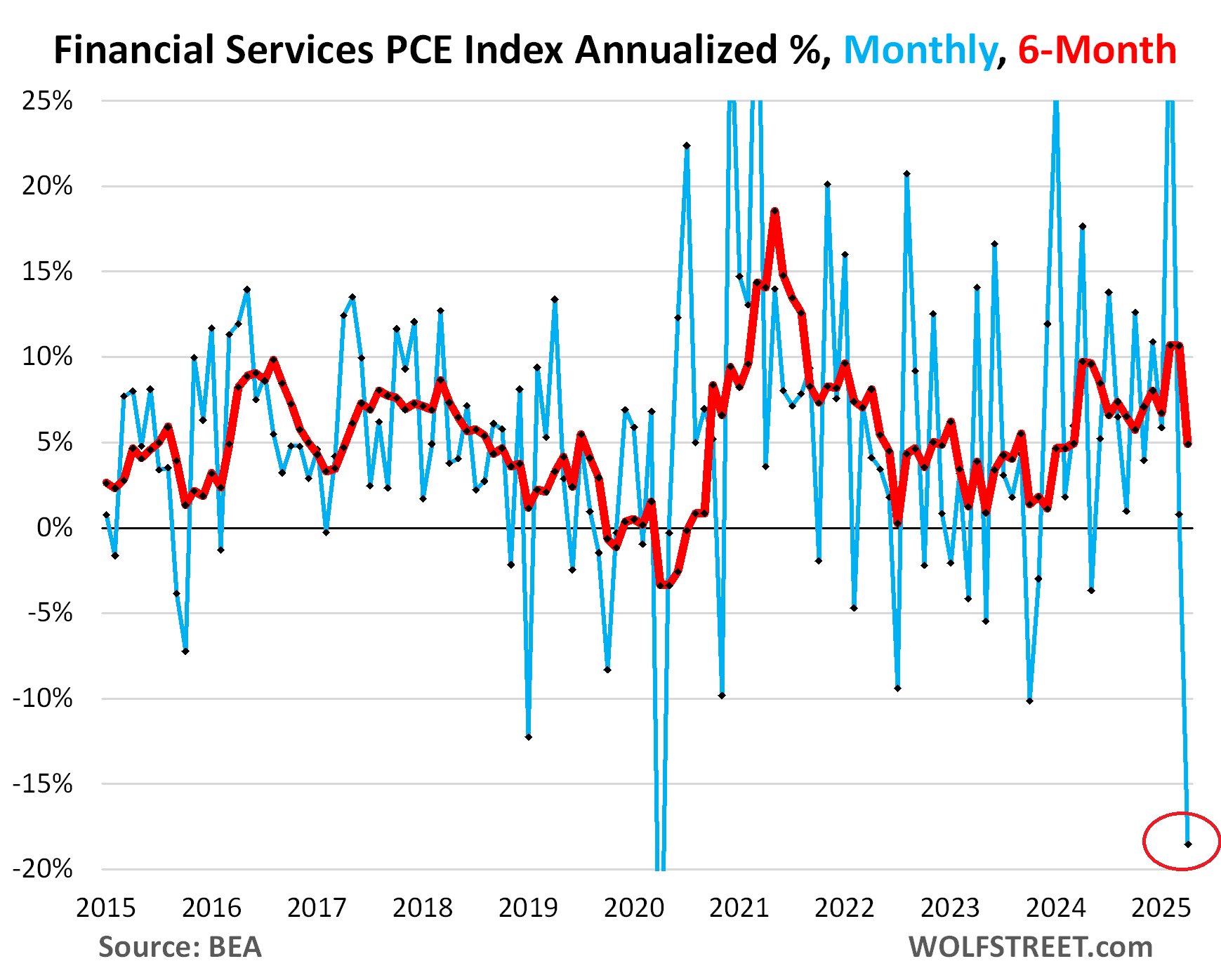

This PCE price index for “financial services” with its “imputed” prices that consumers don’t pay for directly was one of the two stars of the show today.

The “financial services” PCE price index, which features heavily in core services, plunged month-to-month by 1.69% (-18.6% annualized) in April, by far the biggest drop since April 2020, when it plunged even more based on the values it imputed from the crash of the financial markets at the time.

April 2025 experienced a big stock market sell-off, a five-day drop totaling 12.4% of the Wilshire 5000 index, though markets recovered afterwards. And the PCE price index with its imputed values went haywire – but we know that it won’t last, that it will snap back violently:

These are financial services many of which consumers don’t pay for directly, and much of it is imputed from other data. “For example, the imputed value of banking services to deposit holders is calculated based on factors like interest rates and the volume of deposits,” explains the BEA.

It includes fees and commissions at banks, brokers, funds, portfolio management, etc. It includes “financial services furnished without payments” for which imputed values are used; it includes services provided by pension plans; commercial banks and credit unions; regulated investment companies; portfolio management and investment advice firms; trust, fiduciary, and custody activities, etc.

Some of the sources from which values are imputed are FDIC data, PPI data, data from stock exchanges and markets — to impute the values for the components for portfolio management and investment advice services, for example — various government data, etc.

And this financial services PCE price index is hugely volatile, some of it related to sharp movements in the financial markets, as in April 2020 and in April 2025. And it will snap back.

The Fed knows all this, and Powell has occasionally mentioned the Financial Services component when it acts up in one or the other direction, and he might mention it again.

Another hero: Recreation Services PCE price index plunged month-to-month by 0.73% (-8.4% annualized), the biggest plunge in the entire history of the data going back to 1960. So this was another huge outlier....

....MUCH MORE