From Bloomberg, May 11:

It’s becoming clearer by the day that Brightline, the struggling Florida private railroad, is shaping up to rank among the biggest municipal-bond restructurings ever, alongside the likes of Puerto Rico and Detroit.

But that’s where any clarity around the future of billionaire Wes Edens’ $6 billion passion project ends.

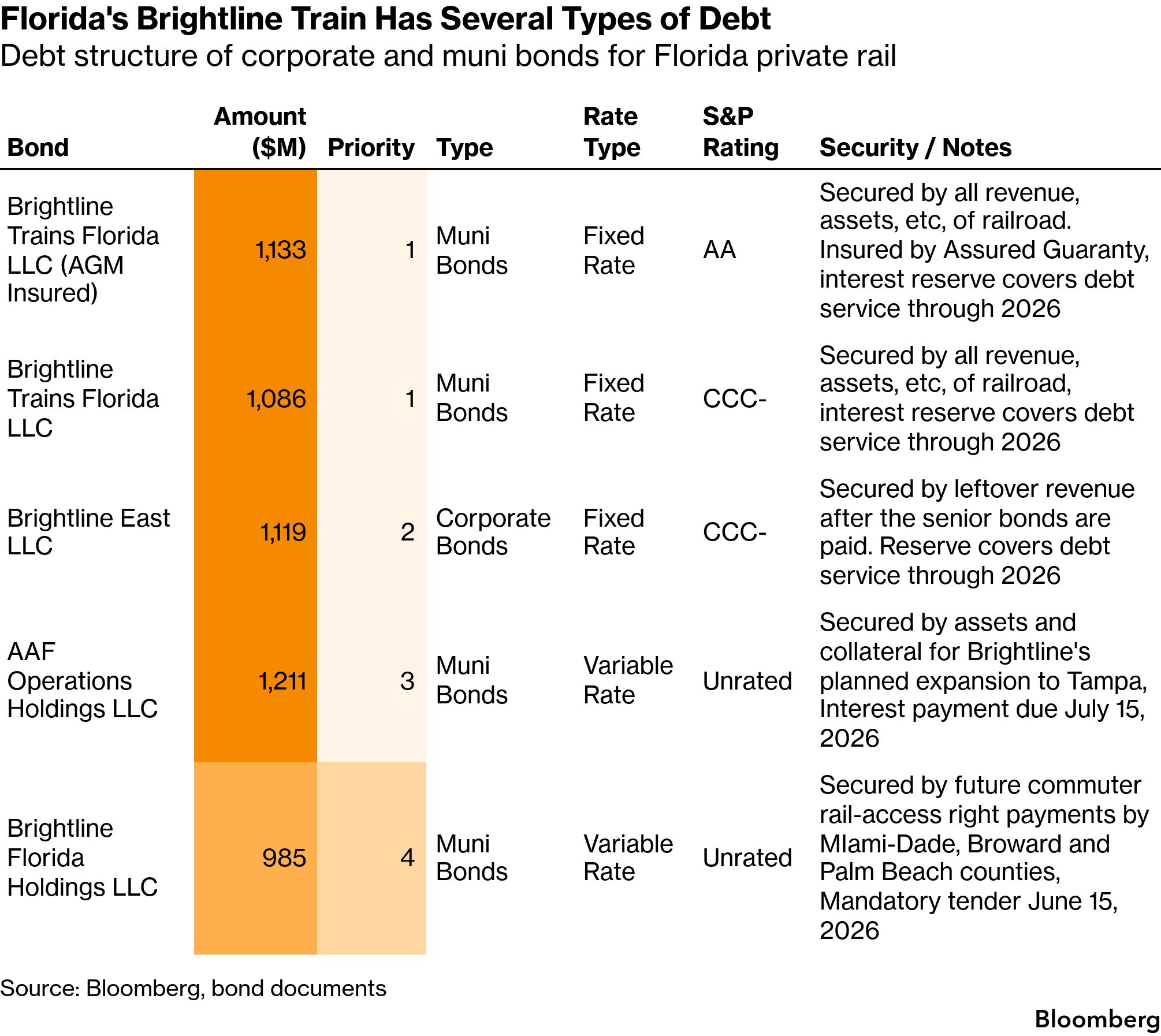

The Fortress Investment Group-backed railroad’s complex debt structure — a mix of municipal and corporate notes issued by four subsidiaries — is among the biggest challenges, as are the pack of firms jockeying for position in any workout scenario.

Invesco Ltd. and Nuveen LLC, giants in the world of tax-exempt securities, lead a group holding Brightline’s $2.2 billion of highest-priority debt that also includes First Eagle Investments. Bond insurer Assured Guaranty Ltd. looms large, too — it guarantees about $1.1 billion of senior securities, a majority, and must consent to any changes.

Meanwhile, distressed specialists Redwood Capital, Aristeia Capital and Nut Tree Capital Management lurk one rung below in the hierarchy. So does an entity of Israel-based Phoenix Financial Ltd., Bloomberg reported last week.

Both factions are angling for a way to wrest control of the railroad in exchange for a large investment, potentially in the form of senior loans to finance a bankruptcy, according to people familiar with the matter.

And then there are the wild cards: deep-pocketed infrastructure funds or strategic buyers that could also be in the mix to take over. One firm that had considered investing in Brightline, but has since moved on, was Italian infrastructure firm Mundys SpA, which owns airports and toll roads, some of the people said.

These competing interests are all coming to a head. Brightline’s auditors Brightline Florida Warns of Likely Insolvency in Financial Audit recently that it doesn’t have the cash to service its debt and meet financial obligations over the next 12 months, raising “substantial doubt” about the 235-mile line’s ability to function without some sort of relief.

For now, the trains between Miami and Orlando are running — still with far fewer riders than projected — and the rail operator has tapped consultants in a renewed bid to find third-party investors and avoid a possible bankruptcy. But its creditors broadly agree that the situation is untenable, and that a debt restructuring, whether in or out of court, is coming within months.

“The debt that the company took out to pay for the project was too high for a realistic assessment of how much ridership they were going to attract,” said Yonah Freemark, a researcher at the Urban Institute. “This is why, generally, infrastructure projects come with public subsidies.”

Interviews with restructuring experts and people with direct knowledge of the Brightline situation describe the railroad plowing slowly into a cash crunch as high costs continuously outstripped revenue.

But its various creditors are now in a race to the finish, huddling with the company in confidential talks as Fortress prepares to relinquish an albatross that lost it $2.2 billion in equity over the course of more than a decade. In the same time span, Fortress itself underwent three ownership changes and a management turnover, and pivoted from its early private equity model to private credit and real estate investments.

A potential bankruptcy, in particular, could cast a shadow over Brightline’s more ambitious project located some 2,500 miles away — a $21.5 billion high-speed rail line between Southern California and Las Vegas called Brightline West....

....MUCH MORE

If interested see also, May 3:

Florida High Speed Rail: "The Great Train Bankruptcy"

Following on April 30's "In Case You Missed It: The Cost Of California's High-Speed Rail Project Is Now Approaching A QUARTER-TRILLION Dollars"

I apparently have a fascination for train disasters, just not of the Gare Montparnasse variety: