From Wolf Street, November 29:

But there is a solution to this affordability crisis.

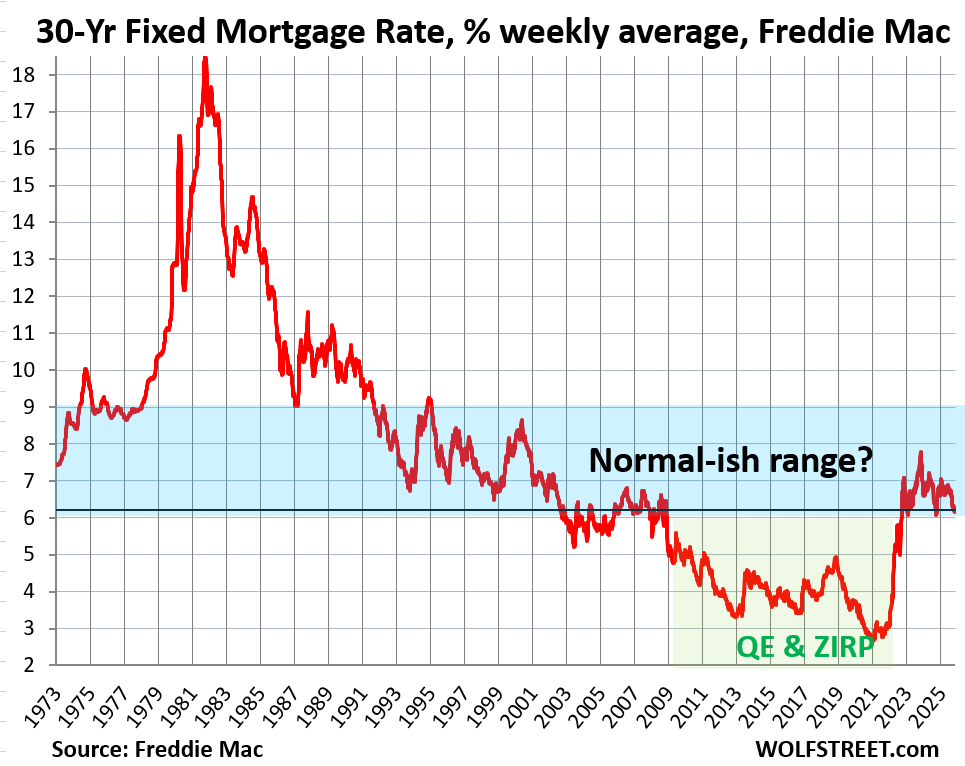

For about the past three months, the average 30-year fixed mortgage rate has been around 6.25%, give or take a few basis points. In the latest reporting week through November 26, it was at 6.23%, according to Freddie Mac data.

While this may seem high to people who have not seen anything beyond the QE era of 2009 through 2022, it’s at the low end of the historical range. There was a 40-year bond bull market from the early 1980s through 2020, during which longer-term yields kept zigzagging lower, and mortgage rates with them. But the final phase of this 40-year bond bull market was driven by QE, starting in 2009, when the Fed bought large amounts of securities, including mortgage-backed securities (MBS). This ended when the worst inflation in 40 years erupted.

The below 5% average 30-year fixed mortgage rates were an aberration caused by QE – an explicit policy by the Federal Reserve to repress mortgage rates to trigger the biggest bout of home price inflation this country has ever seen. The below 5% mortgage rates started in 2009, and in 2012, home prices began soaring. And then, amid the mega-QE during the pandemic, home prices exploded by 50%, 60%, even 70% in many markets in just two years.

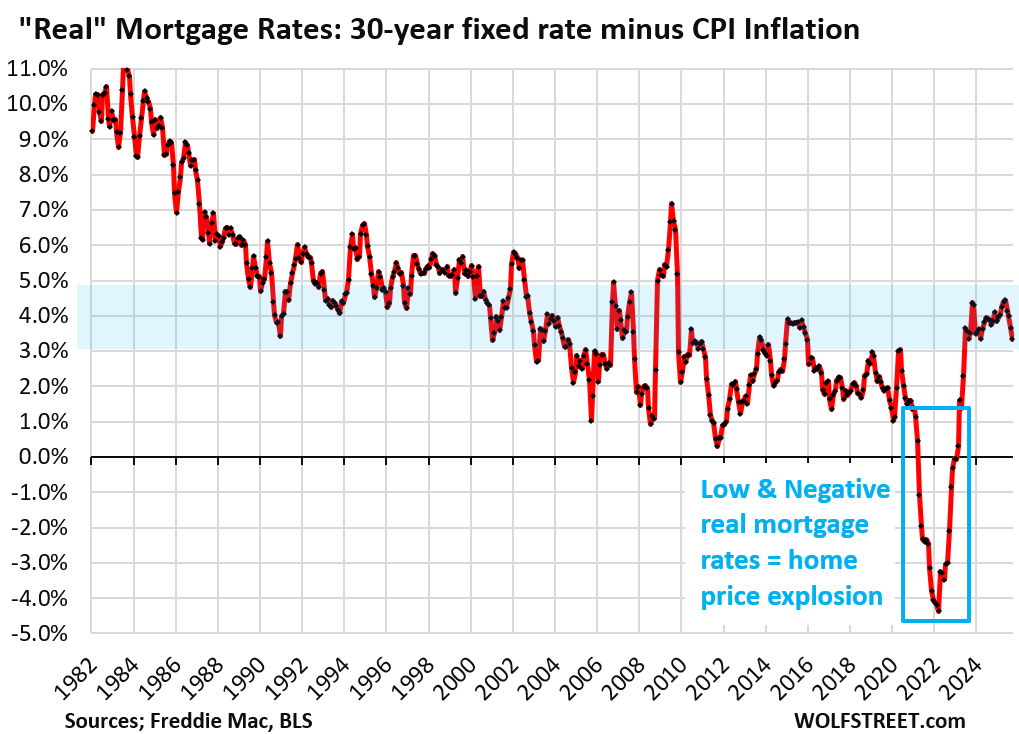

Negative “real” mortgage rates were ultimately the result of the mega-QE from March 2020 through early 2022 – which included the Fed’s purchases of trillions of dollars in MBS – which pushed mortgage rates below 3% even as inflation was spiking.

By the beginning of 2022, inflation was heading toward 9%, and the most reckless Fed ever (as I called it at the time, you can google it) still had its short-term policy interest rates near 0% and was still doing QE to repress mortgage rates.

Mortgage rates were far below the rate of inflation at the time, so negative “real” mortgage rates (mortgage rates minus CPI inflation rates), and that turned out to be better than free money.

FOMO-addled buyers, armed with better-than free money, trampled all over each other, overbid, outbid each other, offered ridiculous amounts “over asking,” bid sight-unseen, waived inspections, etc., and home prices exploded by 50%, 60%, 70% in many markets in just those two years.

Negative real mortgage rates were not normal. They were the result of the most reckless Fed ever. They were an aberration.

Recently, mortgage rates have been in a normal range in relationship to inflation

Now CPI inflation is over 3%, the worst since May 2024, after having accelerated for months. Higher inflation also seems to be the new normal, as the Fed has been cutting its policy rates, and has been discussing further cuts, despite this inflation, and if it continues to cut, it would be an indication that the Fed is going to tolerate higher inflation over the longer term, that it’s comfortable with maybe 3% to 4% inflation. And higher inflation would entail higher bond yields, and therefore higher mortgage rates.

And there is no appetite for QE because it would cause inflation to explode in this already inflationary environment. Americans hate, hate, hate inflation and high prices, and they have a history of voting governments out of office under which that inflation occurred.

What is not in a normal range are home prices. Home prices move very differently in each market – but they soared in most major markets from 2012 to 2019, and then they exploded in most major markets in the two years from mid-2020 to mid-2022.

In a bunch of markets, home prices began sagging in the second half of 2022. In other markets, home prices continued to rise, but at a slower pace.

For example, in Austin, TX, prices of mid-tier single-family homes exploded by 64% in the two years from mid-2020 to mid-2022. That is not normal. It’s ridiculous. And from mid-2012 to mid-2022, over those 10 years, home prices exploded by 207%, from $225,000 to $690,000 for mid-tier single-family homes – having more than tripled in 10 years! That’s not normal; it’s ridiculous. Those are the effects of the Fed’s mortgage rate repression.

Since the peak, home prices in Austin have dropped by 24% as the market is in the slow process of repairing the affordability crisis. Undoing the craziness from 2020-2022 is the solution, along with rising wages over the years, not lower mortgage rates.....

....MUCH MORE

In September 2013's "Ben Franklin on Labor Economics (or how to create an underclass)" I intro'd with:

"In countries fully settled…those who cannot get land must labor for others that have it; when laborers are plenty, their wages will be low; by low wages a family is supported with difficulty; this difficulty deters many from marriage, who therefore long continue servants and single...."

—Haves and Have Nots: The Real Real Estate State and Artificial Scarcity, Technology and Planning

As we, and before us (way before us) Ben Franklin* have pointed out, the surest way to create a permanent underclass is to keep a population from getting on even the first rung of the wealth accumulation ladder.

In most cases this means real estate, access to which is limited by zoning laws and construction regulations constricting supply. Politicians working for their political masters/funders.

Another way to keep the populace from accumulating wealth is to keep the cost of daily expenses, food, rent, transportation, equal to or a bit above income so there is no accumulation of capital and preferably a slide into debt.

A third way to make the rich richer and the poor poorer is to pump enough money into the system to inflate asset prices, benefiting those who already own the assets and combined with the other factors, keep folks in a hand-to-mouth existence.

There's more but that's just what comes to mind without thinking too hard....

You say you want a revolution?