In fact, QE started reversing at the end of 2014.

The Fed’s balance sheet would be “substantially smaller” after the Fed gets done with its QE unwind, Fed Chairman Jerome Powell said on Thursday. How far the Fed might go in shedding assets is a red-hot topic right now that causes a lot of fretting and howling on Wall Street and in the White House. Here is what Powell said at the Economic Club of Washington, D.C – and then we get into the dynamics and charts of what he described and what “substantially smaller” might mean:

“Yes, we wanted to have the balance sheet return to a more normal level, which is a level no larger than it needs to be for us to conduct monetary policy,” he said. When asked what level that would be, he said:

“Don’t know the exact level. That would depend really on the public’s appetite for our liabilities, specifically currency. To us, that’s a liability. And the public has a large appetite for currency….”

“So it will be substantially smaller than it is now,” he said. “But nowhere near what it was before, and the reason is, currency was well less than $1 trillion before quantitative easing started and now is moving up toward $2 trillion.”

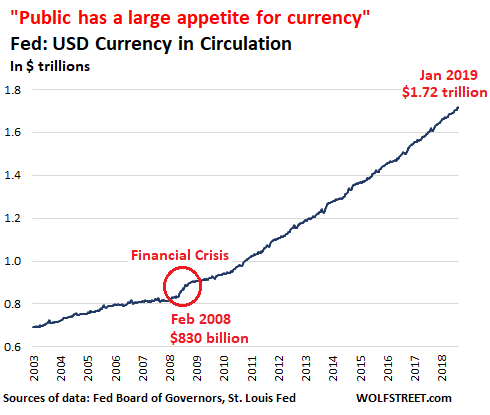

“Currency in circulation”

The line item on the Fed’s balance sheet called “currency in circulation” is composed of Federal Reserve Notes – as it says on the wrinkled and thinning wad of twenties in my pocket — and coins. In other words, hard cash. And as Powell pointed out, this is a liability on the Fed’s balance sheet, not an asset.

The Treasury Department produces the bills and coins. But the Fed manages the amounts in circulation via the banking system. Currency in circulation grows when there is a lot of demand for paper-dollar cash. There must always be enough paper-dollars in the banking system to satisfy the demand by customers for the physical dollars. And as Powell pointed out, “the public has a large appetite for currency.”

This demand for dollars is on a global basis. People globally are hoarding this stuff, and some countries use it as their primary currency, or as an alternate currency alongside their own trashed currency. When the Financial Crisis set in, folks started hoarding more of it, and demand increased at a steeper rate.

This chart shows currency in circulation. The amount more than doubled from $830 billion in February 2008 to $1.72 trillion now:

Note the steeper curve during the Financial Crisis — and afterwards. I also went to the bank and withdrew some extra paper-dollars and stashed them away, just in case. And this, as it was done by hundreds of millions of people around the globe, increased demand for those paper-dollars....MUCH MORE

Currency in Circulation and the Fed’s assets

But banks don’t get paper-dollars for free. They have to trade for them with the Fed dollar-for-dollar. So when currency is put into circulation via the banking system, the Fed records the currency as a liability, and what the Fed gets in return from the banking system dollar-for-dollar becomes an asset on the Fed’s balance sheet. This asset is mostly Treasury securities.

Until QE blew up that whole equation, the asset side of the Fed’s balance sheet was always slightly larger than currency in circulation and has grown in parallel with currency in circulation.

The reason the Fed’s balance sheet was slightly larger than currency in circulation is that the Fed has other assets on its balance sheet, including gold, and it has other liabilities than currency in circulation. But before QE started, currency in circulation was by far its largest liability....